AAVE

AAVE

Target Name

AAVE

Ticker

AAVE

Strategy

long

Position Type

token

Current Price (USD)

127.4

Circulating Market Cap ($M)

1,900

Fully Diluted Market Cap ($M)

2,039

CoinGecko

Aave, the Core Pillar of Decentralized Finance and Onchain Economy

29 Aug 2024, 05:52pm

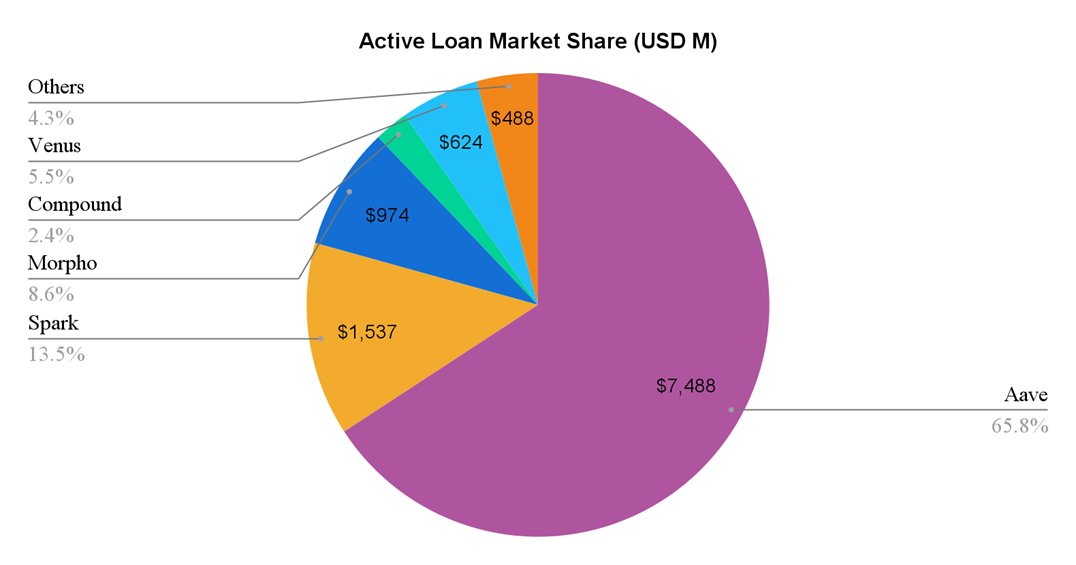

Aave is the largest, most battle-tested borrowing & lending protocol

As the indisputable leader in the onchain lending & borrowing category with an extremely defensible and sticky moat, we think Aave is extremely undervalued as a category leader in one of the most important sectors of crypto and has substantial growth ahead that the market hasn’t caught up to.

Aave launched on Ethereum mainnet in Jan 2020, making this year its 5th year in operations. It has since established itself as one of the most battle-tested protocols across DeFi and the lending/borrowing sector. As a testament to this, Aave is currently the largest borrow/lend protocol at $7.5b of active loans, 5x the quantum of the second largest protocol - Spark.

(Data as of 5th Aug 2024)

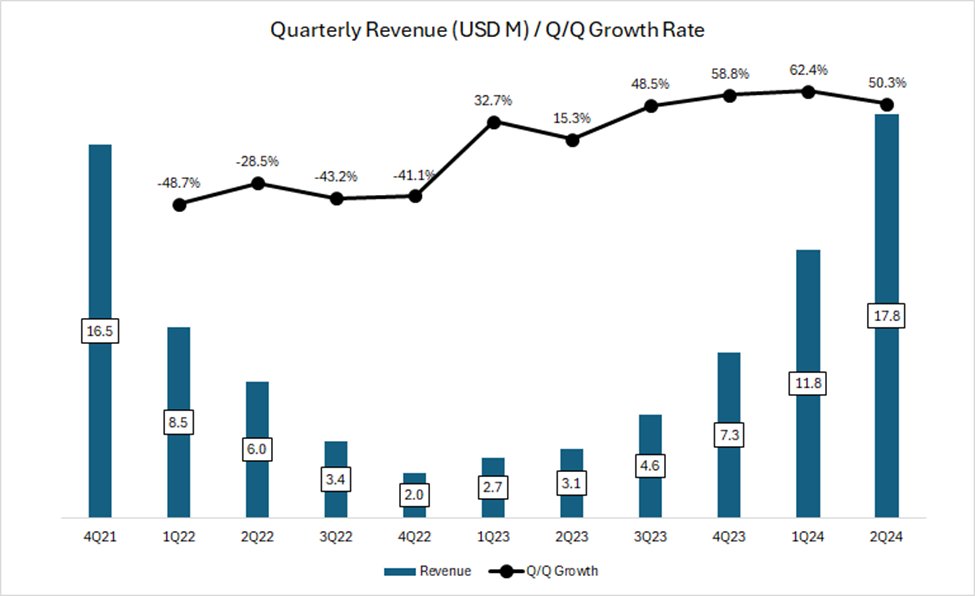

Protocol metrics are growing and have eclipsed the highs of the previous cycle

Aave also stands out as one of the few DeFi protocols that have exceeded their 2021 bull market metrics. For instance, its quarterly revenue has surpassed that of 4Q21 which was the peak of the bull market. Notably, revenue growth continued to accelerate sequentially even as the market went sideways from Nov ‘22 to Oct ‘23. Growth continued to remain strong, growing by 50-60% Q/Q as the market picked back up in 1Q24 and 2Q24.

(Source: Token Terminal)

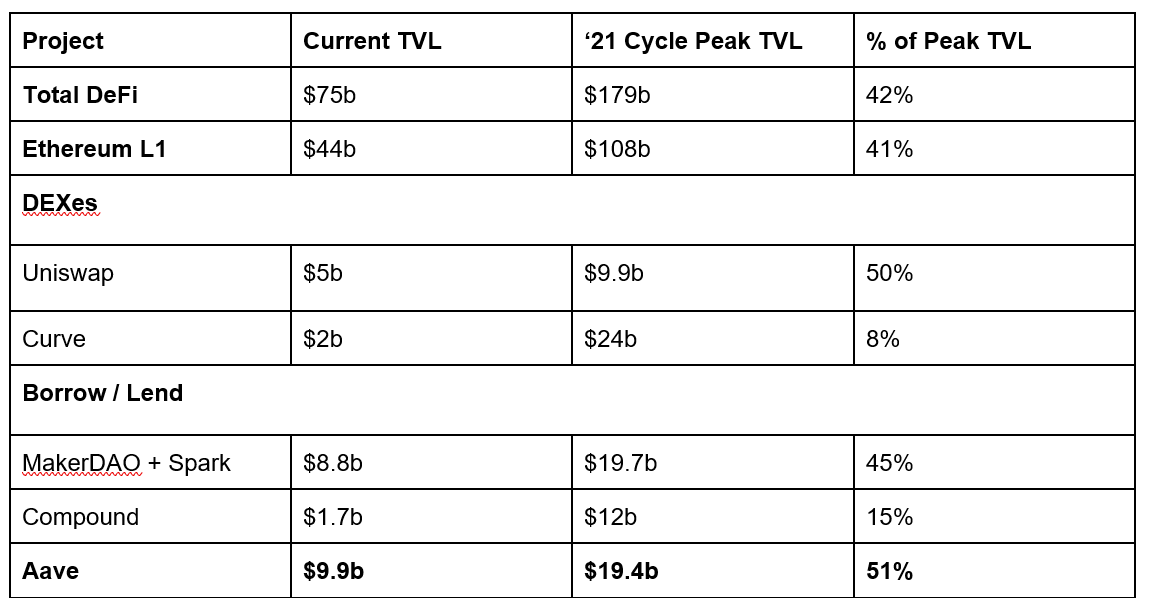

Aave TVL almost doubled YTD, driven by both an increase in deposits and a rise in token prices of underlying collateral assets like WBTC and ETH. As a result, TVL recovered to 51% of ‘21 cycle peak levels, illustrating its resiliency compared to other top DeFi protocols.

Data as of 5 Aug 2024

Superior quality of earnings demonstrates product market fit

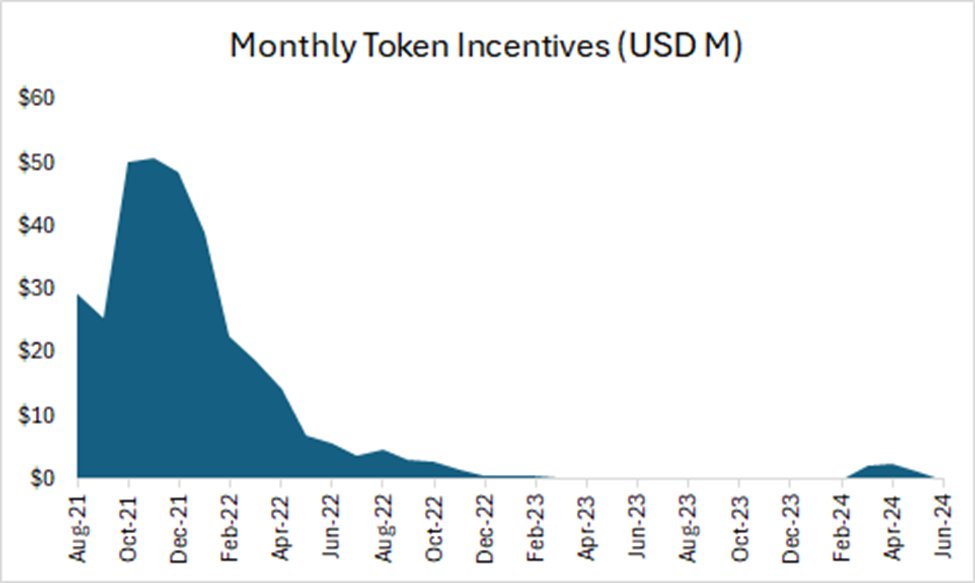

Aave’s revenues peaked in the last cycle during a time when multiple smart contract platforms like Polygon, Avalanche, and Fantom were spending copious amounts of token incentives to attract users and liquidity. This resulted in unsustainable levels of mercenary capital and leverage, which propped up revenue figures for most protocols during that period.

Fast forward to today, token incentives from host chains have dried up, and Aave’s own token incentives are down to negligible amounts.

(Source: Token Terminal)

This indicates that the growth in metrics over the past few months has been organic and sustainable, driven largely by the return of speculation in the market which drives up active loans and borrowing rates.

Moreover, Aave has displayed an ability to grow its fundamentals even during periods of waning speculation. During the market-wide crash across global risk assets in early Aug, Aave’s revenue remained resilient as it managed to capture liquidation fees as loans were repaid. This also serves as a testament to its ability to withstand market volatility across different collateral bases and chains.

(Data as of 5th Aug Source: TokenLogic)

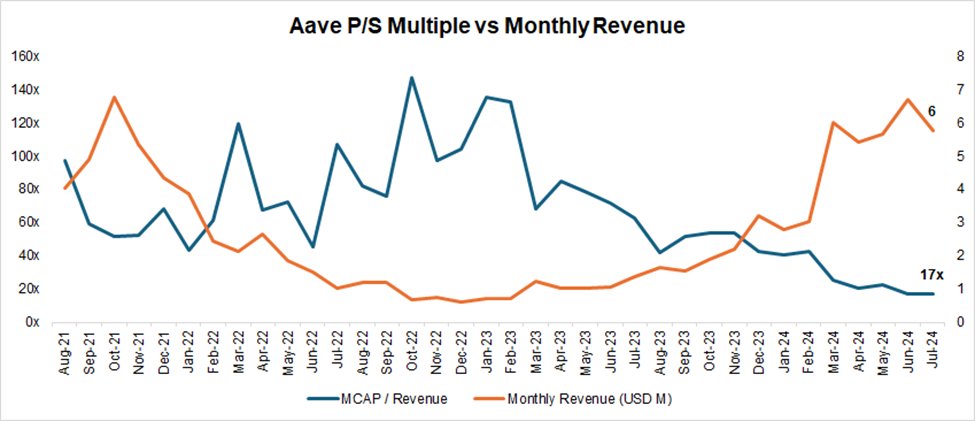

Despite a strong recovery in fundamentals, Aave is trading at the lowest multiples seen in three years

Despite a strong recovery of metrics over the past few months, Aave’s P/S ratio remains depressed at 17x after tumbling to its lowest levels in 3 years, far below the 3 year median of 62x.

(Source: Coingecko, Token Terminal)

Aave is well-poised to extend its dominance in Decentralized Lending & Borrowing

Aave's moat primarily consists of the following 4 points:

Track Record of Protocol Security Management: Most new lending protocols experience security incidents within their first year of operation. Aave has been operating without a single major smart contract-level security incident to date. The security track record from a platform's robust risk management is often the top priority for DeFi users when choosing a lending platform, especially for large whale users with substantial funds.

Two-sided network effects: DeFi lending/borrowing is a classic two-sided marketplace. Depositors and borrowers form the supply and demand sides. Growth on one side stimulates growth on the other, making it increasingly difficult for later competitors to catch up. Moreover, the more abundant the overall liquidity of the platform, the smoother the liquidity entry and exit for both depositors and borrowers, making it more attractive to large fund users, who in turn stimulate further growth of the platform's business.

Excellent DAO management: The Aave protocol has fully implemented DAO-based management. Compared to centralized team management models, DAO-based management offers more comprehensive information disclosure and more thorough community discussions on important decisions. Additionally, Aave's DAO community includes a group of professional institutions with high governance levels, including top risk management service providers, market makers, third-party development teams, and financial advisory teams. This diverse source of participants leads to active governance participation.

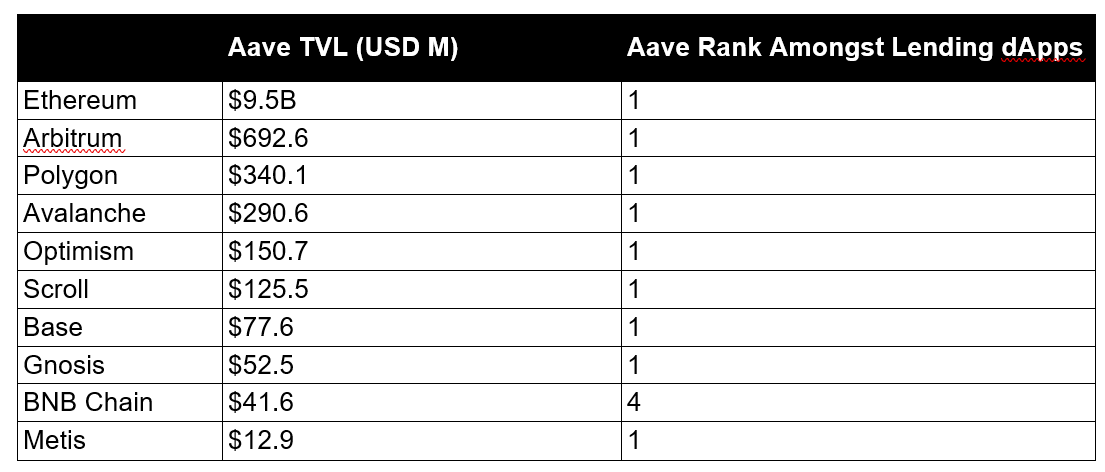

Multi-chain ecosystem positioning: Aave is deployed on almost all major EVM L1/L2 chains, and its TVL (Total Value Locked) is in a leading position on all chains it is deployed to except for BNB Chain. In the upcoming V4 version of Aave, cross-chain liquidity will be linked, making the advantages of cross-chain liquidity even more prominent. See the image below for details:

(Data as of 5th Aug Source: DeFiLlama)

Revamped tokenomics to drive value accrual and remove slashing overhang

The Aave Chan Initiative just launched a proposal to overhaul $AAVE’s tokenomics, which will enhance the utility of the token by introducing a revenue-sharing mechanism

The first major shift would be to remove the risk of $AAVE being slashed when mobilizing the Safety Module.

● Currently, stakers of $AAVE (stkAAVE - $228m TVL) and $AAVE / $ETH Balancer LP tokens (stkABPT - $99m TVL) in the Safety Module expose themselves to having their tokens slashed to cover for shortfall events.

● However, stkAAVE and stkABPT are not good coverage assets given the lack of correlation with collateral assets accruing bad debt. The selling pressure on $AAVE during such events would also circularly reduce coverage.

● Under the new Umbrella Safety Module, stkAAVE and stkABPT would be replaced by stk aTokens starting with aUSDC and awETH. aUSDC and awETH suppliers can opt for their assets to be staked to earn additional fees (in $AAVE, $GHO, protocol revenue) on top of interest earned from borrowers. These staked assets are liable to be slashed and burnt during a shortfall event.

● This arrangement is beneficial for both users of the platform as well as $AAVE token holders.

Additionally, more demand drivers for $AAVE will be introduced via revenue-sharing mechanisms.

● Introduction of Anti-GHO

○ Currently, stkAAVE users enjoy a 3% discount on minting and borrowing $GHO.

○ This will be replaced by a new “anti-GHO” token which is generated by stkAAVE holders who mint GHO. Anti-GHO generation is done linearly and is proportional to the interest accumulated by all GHO borrowers.

○ Anti-GHO can be claimed by users and used in 2 ways:

■ Burn Anti-GHO to mint GHO, which can be used to repay debt for free

■ Deposit into GHO Safety Module for stkGHO

○ This increases the alignment of AAVE stakers with GHO borrowers and would be an initial step to a broader revenue-sharing strategy.

● Burn and Distribute Program

○ Aave will enable net excess protocol revenues to be redirected to token stakers subject to the following conditions:

■ Aave Collector net holdings are at 2 yearly service providers’ recurring costs for the past 30 days.

■ Aave protocol 90-day annualized revenue is at 150% of all protocol expenses YTD, including the AAVE acquisition budget and aWETH & aUSDC Umbrella budgets.

○ We will start observing consistent 8 figures of buyback from Aave protocol from this and poised to grow even further as Aave protocol continues to grow from here.

Moreover, $AAVE is almost fully diluted with no major future supply unlocks, a stark contrast to recent launches which have been bleeding upon token generation event (TGE) due to the low float high fully-diluted valuation (FDV) dynamics.

Significant growth ahead for Aave

Aave is have multiple growth factors ahead and it is also well-positioned to benefit from the secular growth of crypto as an asset class. Fundamentally, Aave’s revenue can grow in a multitude of ways:

Aave v4

Aave V4 is set to further enhance its capabilities and put the protocol on track to onboard the next billion users into DeFi. First, Aave will focus on revolutionizing the user experience of interacting with DeFi through building a Unified Liquidity Layer. By enabling seamless liquidity access across multiple networks (both EVM and eventually non-EVM), Aave will eliminate the complexities of cross-chain transitions for borrowing and lending. The Unified Liquidity Layer will also lean heavily on Account Abstraction and Smart Accounts to allow users to manage multiple positions across isolated assets.

Second, Aave will improve accessibility to its platform via expanding to other chains and onboarding new asset classes. In June, the Aave community endorsed the protocol's deployment on zkSync. This move marks Aave's entry onto its 13th blockchain network. Soon after in July, the Aptos Foundation authored a proposal for Aave to deploy on Aptos. If passed, the Aptos deployment would be Aave’s first foray into a non-EVM network and would further cement its position as a truly multi-chain DeFi powerhouse. Furthermore, Aave would also explore integrating RWA-based products which would be built around GHO. This move has the potential to bridge traditional finance with DeFi, attracting institutional investors and bringing a flood of new capital into the Aave ecosystem.

These developments culminated in the creation of the Aave Network, which would be the central hub where stakeholders would interact with the protocol. GHO is set to be used for fees, while AAVE would be the main staking asset for decentralized validators. Given that The Aave Network will either be developed as an L1 or L2 network, we expect the market to reprice its token accordingly, reflecting the additional infrastructure layers being built.

Growth is positively related to BTC & ETH’s growth as asset class

The introduction of both Bitcoin and Ethereum ETFs this year represents a watershed moment for crypto adoption, offering investors a regulated and familiar vehicle to gain exposure to digital assets without the complexities of direct ownership. By lowering barriers to entry, these ETFs are poised to attract significant capital from institutional investors and retail participants, catalyzing further integration of digital assets into mainstream portfolios.

The growth of the broader crypto markets are a boon for Aave given that more than 75% of its asset base is comprised of non-stable assets (mostly BTC and ETH derivative assets). As such, Aave’s TVL and revenue growth is directly tied to the growth of these assets.

Growth is indexed to stablecoin supply

We can also expect Aave to benefit from growth in the stablecoin market. As global central banks signal a shift towards a rate-cut cycle, it would lower the opportunity cost for investors seeking yield sources. This might catalyze the rotation of capital from TradFi yield instruments to stablecoin farming in DeFi to access more attractive yields. Furthermore, we can expect higher risk-seeking behavior in bull markets which serves to increase stablecoin borrow utilization on platforms like Aave.

Final thoughts

To reiterate, we are bullish about the prospects of Aave as the leading project in the large and growing decentralized lending& borrowing market. We have further outlined the key drivers that underpin the future growth and detailed how each of them could further expand.

We also think Aave will continue to dominate market share due the strong network effects that it has built, driven by the liquidity and composability of the token. The upcoming tokenomics upgrade serve to further improve the security of the protocol and further enhance the value capture aspect of it.

Over the past few years, the market have lumped all DeFi protocols in one basket and priced them as if they are protocols with little growth ahead. This is evident from Aave’s TVL and revenue run rate trending up while its valuation multiples compress. We believe such deviations in valuations and fundamentals will not last for long and $AAVE offer some of the best risk-adjusted investment opportunities in crypto now.

•

•

•

Affiliate Disclosures

- The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- The author is not being compensated in any form by the target in relation to this research.

- To the best of the author’s knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

Neither BIDCLUB nor PHATPITCH LLC represents or endorses the accuracy or reliability of any advice, opinion, statement or other information displayed, uploaded, or distributed through BIDCLUB by any user, information provider, or other party. PHATPITCH LLC is not a broker, a dealer, or investment adviser. Nothing in BIDCLUB constitutes an offer or a solicitation to buy or sell any securities. BIDCLUB prohibits the sharing of material non-public information (MNPI), but assumes no responsibility for member conduct or associated risks. Nothing in BIDCLUB is intended as specific investment advice and no individual should make any investment decision based on any recommendation or analysis provided on BIDCLUB. You acknowledge that any reliance upon any such opinion, advice, statement, memorandum, or information shall be at your sole risk, and you bear sole responsibility for your own research and investment decisions. See full

Terms and Conditions.

gm Arthur ty for the thesis.

Do you have any insight at all re: Trump x Aave?