Ethena

ENA

Target Name

Ethena

Ticker

ENA

Strategy

long

Position Type

token

Current Price (USD)

-

Circulating Market Cap ($M)

-

Fully Diluted Market Cap ($M)

-

CoinGecko

-

$ENA - Linear Maker; Exponential Ethena

11 Sep 2024, 10:02am

Overview of Ethena

building the synthetic dollar w/ internet native yield; the peg of USDe (its native stablecoin) is supported through delta hedging derivatives against protocol held collateral

yield of the stablecoin USDe is generated through a) native ETH emissions + b) funding rate from shorting ETH on centralized trading venues; and currently yield of staked USDe (sUSDe) is 4.4%

token value accrual of $ENA comes from a) locking up of $ENA to boost potential future rewards + b) restaking for economic security to secure cross chain transfers of USDe

Investment Thesis

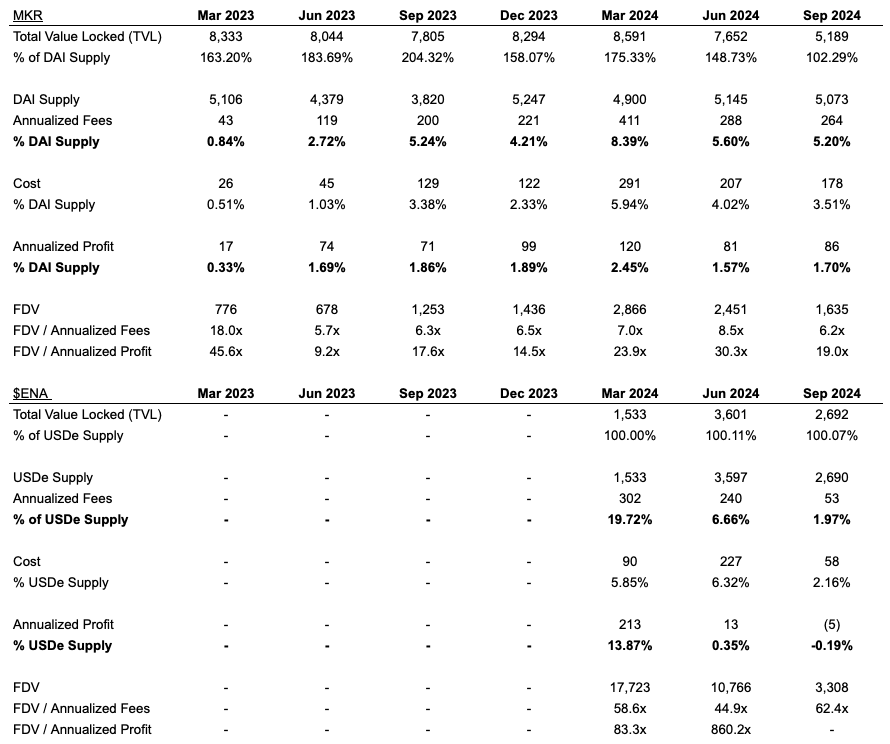

[potentially fastest horse in DeFi when the tides turn + do not want to write $ENA off in the anti low float high FDV meta + current valuation of >3bn FDV gives good odds w/ something of the potential to make >300mn annualized top line fees w/ <2bn TVL casually as shown in March]

secular stablecoin growth as one of the very few products in all crypto w/ proven product market fit; out of which market share of decentralized stablecoin is also expected to expand (i.e. <5%)

deep on / off chain integration including a) Bybit accepting USDe as collateral to trade perps while capturing yield w/ BTC and ETH spot trading pairs + b) USDe and USDe also integrated w/ Solana DeFi protocols such as Kamino and Drift

stellar founding and BD team + strong ventures backers making them the quickest stablecoin to reach >3bn in TVL in all DeFi history in the course of less than a year

on a protocol level + competitive angle; a) $ENA has the potential to print astronomical fees+ b) retain majority of its value to protocol’s earnings + c) better capital efficiency compared to other decentralized stablecoin protocols

staked USDe natively generates higher yield from a) ETH native yield + b) negative funding rate which could go as high as >30% in a directional market; as opposed to Maker which finds yield from stability fees (>5% on TVL which is expensive) + RWA vaults that comes with interest rates headwind that limits the protocol fee growth

given native higher yields; Ethena is able to retain most value from the fees generated to the protocol (i.e. >13% of USDe supply converted to protocol earnings) as opposed to Maker having to a) pass most to sDAI through DSR and retain only <2% of DAI supply on average + b) tough to adjust stability fees upwards which strips away protocols’ pricing power

w/ better use of capital in which each dollar TVL creates the equal dollar amount of USDe; as opposed to Maker having to be over collateralized (i.e. each $DAI requires >130% in TVL)

Valuation Analysis

effectively paying >60x FDV / annualized L30D fees now w/ <2.7bn in USDe supply now pricing in stronger growth w/ reasons mentioned above + function of low float

last cycle DAI supply peaked at <10bn and UST supply peaked at >18bn; assuming $USDe reaches a similar scale + $ENA retains most of the value and protocols earnings be at <5% of USDe supply; slapping a >20x P/E gives a >15bn outcome which is a close to 5x

theoretically this should be a conservative assumption; when market becomes directional the value retained to the protocol should be closer to the March’s numbers which means they could retain >10% from USDe’s total supply + multiple expanding

Catalyst

season 2 ended few days ago; giving out 5% of total token supply which could lead to more dumping in the short run but next season would not end in months + huge early investors unlocking comes next April giving a window of limited supply overhang

interest rates are coming down in September earliest as most expect; direct competitor $MKR (or $SKY) would be directly impacted although RWA is only a fraction of what Maker’s making now

Risks

investor unlocking happening next April effectively more than doubles circulating supply of $ENA + venture investors up by multiples so profit taking is a serious problem

systematic risks when USDe grows; we have never lived in a world where funding rate is overlayed by a structural short position in large cap collateral assets

Execution

liquid in most centralized venue including Binance and OKX; could get a bit creative OTCing w/ early venture investors to lock in DPI for them even with a huge discount to the current FDV

would assume funds’ positioning in this name is light given how price action has been since TGE

•

•

•

Affiliate Disclosures

- The author and/or others the author advises currently hold, or plan to initiate, an investment position in target.

- The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- The author is not being compensated in any form by the target in relation to this research.

- To the best of the author’s knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

Neither BIDCLUB nor PHATPITCH LLC represents or endorses the accuracy or reliability of any advice, opinion, statement or other information displayed, uploaded, or distributed through BIDCLUB by any user, information provider, or other party. PHATPITCH LLC is not a broker, a dealer, or investment adviser. Nothing in BIDCLUB constitutes an offer or a solicitation to buy or sell any securities. BIDCLUB prohibits the sharing of material non-public information (MNPI), but assumes no responsibility for member conduct or associated risks. Nothing in BIDCLUB is intended as specific investment advice and no individual should make any investment decision based on any recommendation or analysis provided on BIDCLUB. You acknowledge that any reliance upon any such opinion, advice, statement, memorandum, or information shall be at your sole risk, and you bear sole responsibility for your own research and investment decisions. See full

Terms and Conditions.

Correct me if I'm wrong but I see

- most of the fees accrued is paid out to sUSDe

- TVL actually declining since mid June

- funding rate today isn't that great

- no ENA token value capture really

- lack of effort in making USDE used (CEX parking doesn't count)

- continuous inflation of ENA aside from investor vesting to incentivize TVL

I'd love some color on how much ENA is emitted on an average daily basis currently (as per season) and what the future of driving adoption + value-capture looks like -- but otherwise this still seems like a pretty good short?