Drift

DRIFT

Target Name

Drift

Ticker

DRIFT

Strategy

long

Position Type

token

Current Price (USD)

0.69

Circulating Market Cap ($M)

157

Fully Diluted Market Cap ($M)

693

CoinGecko

Drift ($DRIFT) Analysis and Valuation - the Binance moment for derivatives DEXs.

13 Sep 2024, 06:04pm

[Link to original full post]

Executive Overview

Multicoin has accumulated a large position across our funds—both liquid and venture—in DRIFT, the native token of Drift, a derivatives decentralized exchange (derivatives DEX) on Solana. We built the position over the last few years via private and more recently, via public markets as well. We have long believed in the opportunity for Open Finance, which we define as making all units of value—including, but not limited to, stocks, bonds, real estate, and currencies—interoperable, programmable, and composable on distributed ledgers, thus making capital markets more efficient and accessible to everyone on the planet. Open Finance, and by extension decentralized finance (DeFi), is one of our three Crypto Mega Theses. The biggest opportunity in Open Finance is a protocol which is built to allow anyone anywhere in the world the ability to trade any asset. The executive summary of our DRIFT thesis is as follows:

1. We believe that the most successful derivatives DEX needs to be built on an L1 that has other assets issued on the chain. We do not think that appchain derivatives DEXs will win because they will never be as performant as centralized exchanges (CEXs), nor will they be able to compose with other programs and assets on a general-purpose chain. They do not benefit from ecosystem flywheels that exist on generalizable L1s.

2. Drift has a unique exchange construction that enables three types of liquidity provisioning: dynamic AMM (DAMM), decentralized central limit order book (DLOB), and just-in-time (JIT). We previously wrote about the trade-offs in the design space of derivatives DEXs here and believe Drift has chosen the optimal set of trade-offs.

3. Drift’s core metric—total volume across derivatives, spot, and swaps—is up ~50x year over year, and the protocol’s market share in the derivatives DEX sector is up ~10x in that time.

4. The Drift team is relentless and constantly ships new products and features. Beyond a derivatives DEX, they are building a capital efficient DeFi platform that expands beyond synthetic trading. We believe Drift could be a DeFi “superapp” due to its ability to cross sell trading products to users.

5. Solana adoption is growing extremely quickly, and we are witnessing a secular growth trend across all Solana DeFi applications. Drift will disproportionately benefit from significant ecosystem growth tailwinds because we believe it’s the best constructed derivatives DEX on Solana.

6.The Drift team has the privilege of focusing 100% of their efforts on product rather than infrastructure. This is only possible because Solana is scaling without any input or thought from the Drift team. Being on Solana allows the Drift team to focus on product in an integrated, composable stack, vs the complexity and bridging of a modular environment. As the Solana network continues to improve (e.g., the introduction of Firedancer and Agave clients and other network upgrades), the developer experience and infra layer Drift lives on gets better without any engineering effort from the Drift team or other contributors.

a. Note - this is the ideal expression of modularity in software systems. Systems should naturally improve over time without developers having to think or act at all.

7. Based on our valuation framework and assumptions, which we outline at the bottom of this report, we value DRIFT in our base case at $3.58, more than 7x above its current price.

Market Analysis

THE OPPORTUNITY FOR DERIVATIVES DEXS

The vast majority of crypto’s big implosions in 2022 (i.e., FTX, BlockFi, Voyager, Celsius, Genesis) were centralized institutions. These centralized products generally go against the ethos of crypto; crypto is about empowering users all over the world to have more control over their assets by leveraging open and transparent systems. DeFi protocols, such as AAVE, Compound, Maker, Hubble, Uniswap, Orca, etc., all performed flawlessly during 2022 despite the massive volatility. This, to us, reinforces the efficacy and importance of DeFi.

Source: The Block

Over the past 12-24 months we’ve witnessed an explosion of DeFi activity on Ethereum/L2s and Solana. This wave of activity has been primarily driven by lending platforms (e.g., Aave, MakerDAO, Kamino, marginfi) and trading platforms (e.g., Uniswap, 0x, Orca, Phoenix, and Raydium). This is because—while clearly an important idea—DeFi, in its current incarnation, is mostly just a mechanism for going margin-long SOL, ETH, ARB, OP, SEI, APT, etc., and other DeFi tokens and memecoins. Market consensus has quickly converged on the idea that DeFi—at least for now—is “just” open and non-custodial Binance/HTX/Deribit. However, if you look at the data in the chart above, even in its current form, DeFi has been growing faster than CeFi.

DeFi traders today primarily access leverage through lending protocols and spot DEXs. For example, a trader can post $150 of SOL as collateral on Kamino, borrow $75 of USDC, and then trade that USDC on any market or DEX for $75 worth of SOL (the asset deposited as collateral). This allows her to hold $225 worth of SOL, thus giving her a higher level of exposure to the price movements of SOL. She has $225 of SOL and owes $75 of USD denominated debt (represented by the USDC she borrowed).

The current model has a few notable limitations: (1) traders are capped on leverage because most DeFi lending protocols require >133% collateralization (on non correlated pairs), and (2) because traders must borrow and sell spot assets, they can only lever up—or short sell—Solana native assets if the borrow/lend is on Solana. This is also true if the borrow/lend protocol is on Ethereum; they can only lever up on Ethereum native assets. There are varying solutions to this problem, most notably bridged assets, but bridges continue to be the largest security risk in crypto. Even in Solana, which is one of the most capital efficient ecosystems, only ~$826M of the ~$3B that was being lent on margin protocols (as of September 2024) was being borrowed, leaving ~$2.2B idle (we understand the capital sits there so that lenders can redeem with no term).

It is clear there’s demand for this type of spot leverage; however, in order for other real-world assets to be traded on chain in any reasonable timeframe, crypto markets need derivatives. A derivatives venue can allow anyone in the world the ability to trade any asset, whether a traditional asset or digitally native asset.

THE ROLE OF PERPETUAL SWAPS

Today, the most liquid financial derivative in crypto is the perpetual swap contract, and for good reason: the “perp swap” is one of the most important and elegant contracts in modern-day finance. Popularized by BitMEX, perp swaps now trade >$100B per day across all the major CeFi derivatives exchanges. Perp swaps have become widely popular because they afford several advantages over other forms of financial contracts:

● The futures contract never expires, meaning traders can keep it open “perpetually.” They do not need to worry about rolling over their positions.

● Perp swaps are entirely synthetic, which allows any collateral type for any position.

● Via a clever mechanism known as the funding rate, perp swaps track their underlying prices more closely than dated futures contracts.

● They can be more easily traded with leverage than spot.

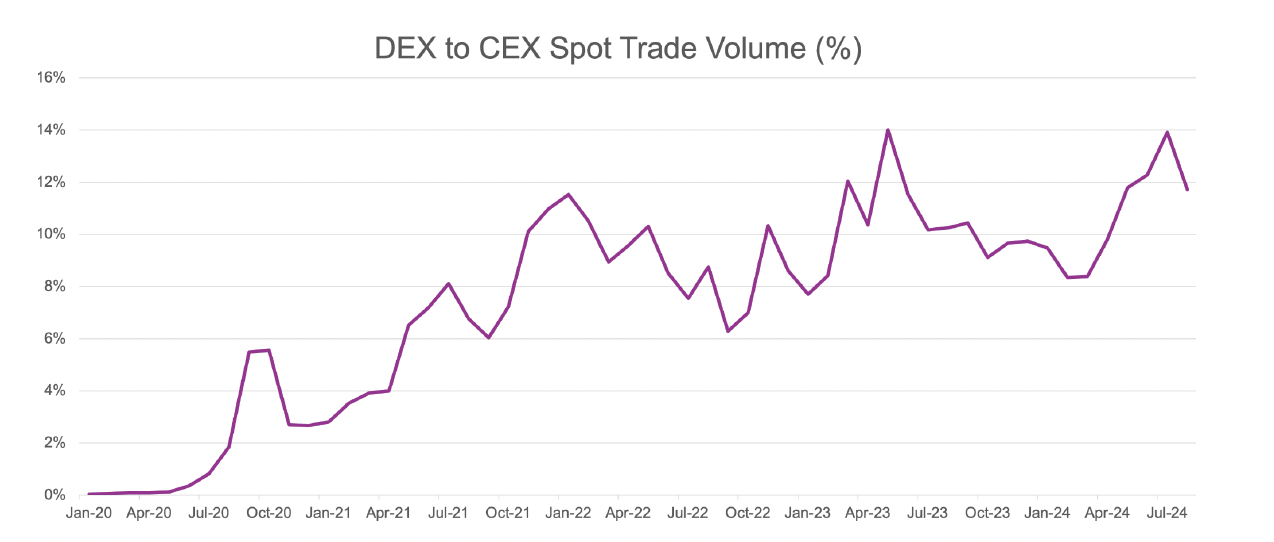

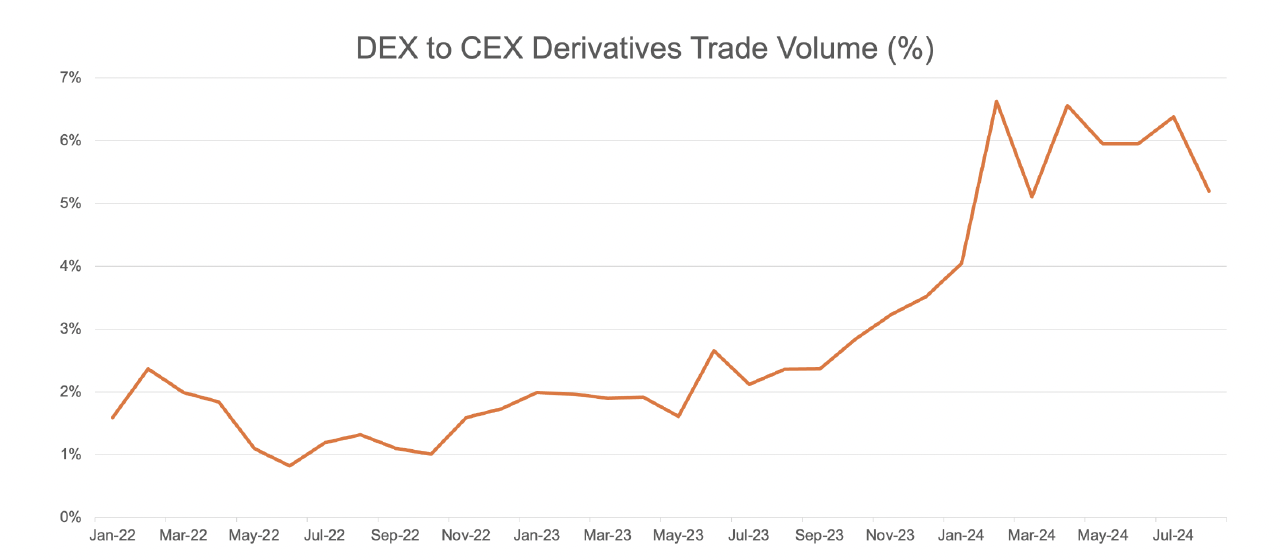

As shown in the chart above, DEX spot volume is currently ~12% of that of CEX spot volume. On the other hand, DEX derivatives volume is currently ~5% of that of CEX derivatives volume:

Source: The Block, DefiLlama

We think most crypto derivatives traders today are (1) more sophisticated than spot traders, or (2) overleveraged speculators. Highly sophisticated traders care a lot about fill price, execution, latency, etc, and are thus served better—right now—by CEXs. The levered speculators tend to go where it is most convenient, and for most traders that means CEXs. As a note, Binance reported in early 2020 that 79% (!) of perps speculators used >20x leverage, implying heavy retail participation.

That perp swaps have completely dominated CEX trading tells us something: traders prefer speculating on highly leveraged synthetic contracts over spot margin trading. And that is on centralized exchanges where those companies can allow deposits for every blockchain-based asset as collateral. These assets are liquid and can be borrowed and posted for spot margin on CEXs, but users prefer stablecoin margined perps over posting any of these as collateral or borrowing them. Traders on Solana do not even have the luxury of “depositing” BTC, XRP, BCH, LTC, DOGE, etc. as collateral (in a trust-minimized way), and thus perps—which allow anyone to lever up on any asset, with any form of collateral—are best positioned to win leveraged trading on Solana.

As it relates to derivatives DEXs, unlike spot margin, perp markets only require three core functions:(1) a matching and risk engine, (2) an oracle, and (3) an asset (stable or volatile) for margin. Because they are entirely synthetic, not only can perp exchanges accept any form of collateral, they can also enable trading on any asset (forex, commodities, equities, crypto, prediction market events, etc.).This makes them the ideal instrument for financial inclusion.

There is significantly less counterparty risk in spot trading than there is in derivatives trading. If Alice owns USDC, and wants to sell it for SOL, she can deposit it into a CEX, sell it for USDC, and withdraw it all in a matter of minutes (dependent on confirmations, withdrawal times, etc.). However, if she wants to open a derivatives position for some extended period of time, she must hold her collateral on the CEX in order to maintain her margin and keep her position open. As such, there is substantially more counterparty risk when trading derivatives as opposed to trading spot.

In the future, we believe that more and more retail users will get web3 wallets for reasons that are explicitly not speculation. This could include stablecoin payments, DePIN earnings, etc., as discussed further in this report. They will want to be able to trade any asset (forex, commodities, stocks, crypto, prediction markets, etc.), and find structures that help them hedge earnings (e.g., a Helium miner using HNT perps to hedge their future earnings). And the most convenient place to trade everything in a composable way will be on derivatives DEXs—specifically through perps.

CEXs (rightfully or wrongfully) are becoming slower and more rigid about their listing standards. If you want to trade a long tail asset then DEXs are the only place to go. CEXs also generally block users from jurisdictions (see, e.g., Binance prohibited jurisdictions) if their platforms include perpetual swaps. While many DeFi front ends, including Drift, geoblock regions including the U.S., there is a massive opportunity for derivatives DEX protocols to fill the gap by offering permissionless access and faster token listings for users that are currently boxed out of the system.

To get a sense of the potential scope of the TAM for a derivatives DEX, just think about how many trades are economically worthwhile but do not happen because of trust or access issues.

Permissionless access across borders expands access to global financial markets to billions of people around the world who do not currently have access. In the ideal future case for DeFi, anyone anywhere in the world will be able to trade any asset they want. This is extremely market expansionary (the market does not fully appreciate just how big this market could get). As billions of people come online in the developing world and need access to financial markets, they will seek out derivative DEXs. DEXs ensure that no exchange operator or politically motivated regulator can unilaterally change the rules of the exchange – meaning that traders all around the world can be comfortable trading on the same venue.

We believe the derivatives DEX market will be a winner-take-most market due to the strong network effects of liquidity. We also expect them to cannibalize market share from centralized incumbents due to their ability to cut costs and pass those savings on to traders; DEXs don’t require large customer support teams, localization, universal deposits/withdrawals and custody systems, etc. In order to grow into the world’s default trading venue, it’s very important that teams make the right set of trade-offs early, and to get the flywheel started by attracting liquidity providers and takers. We think Drift has gotten it right, and the results will compound.

MARKET COMPETITION: COUNTER THE STATUS QUO

The idea of derivatives DEXs is not new. UMA wrote the BitDEX paper in October 2019. Initially, derivatives DEXs were on Ethereum L1. Then they gradually moved over to Ethereum L2s (e.g., GMX on Arbitrum was the dominant derivatives DEX of the last cycle).

More recently, there has been a large structural move in the derivatives DEX market towards dedicated chains for DeFi derivatives, otherwise known as “appchains.” We do not view appchains as the correct approach for derivatives DEXs long term because they suffer from a lack of composability—both on-chain and off-chain forms of composability. They also are overly reliant on central points of failure and bridging infrastructure (they either lack native stablecoin support and/or don’t have third-party issuers that launch net new tokens on their chains). Additionally, they are limited in their ability to support native tokens as collateral, either because they don’t have independent third-party tokens and/or because the tokens on their chains are extremely illiquid.

The most well-known derivatives DEX protocol on an appchain is Hyperliquid. We contend that it is not practically a derivatives DEX because of the opaque nature of the validator set; it’s fast today but can be censored tomorrow. To our knowledge, Hyperliquid is an on-chain CLOB in which the validator set is made up of a limited set of validators run by the core contributors.

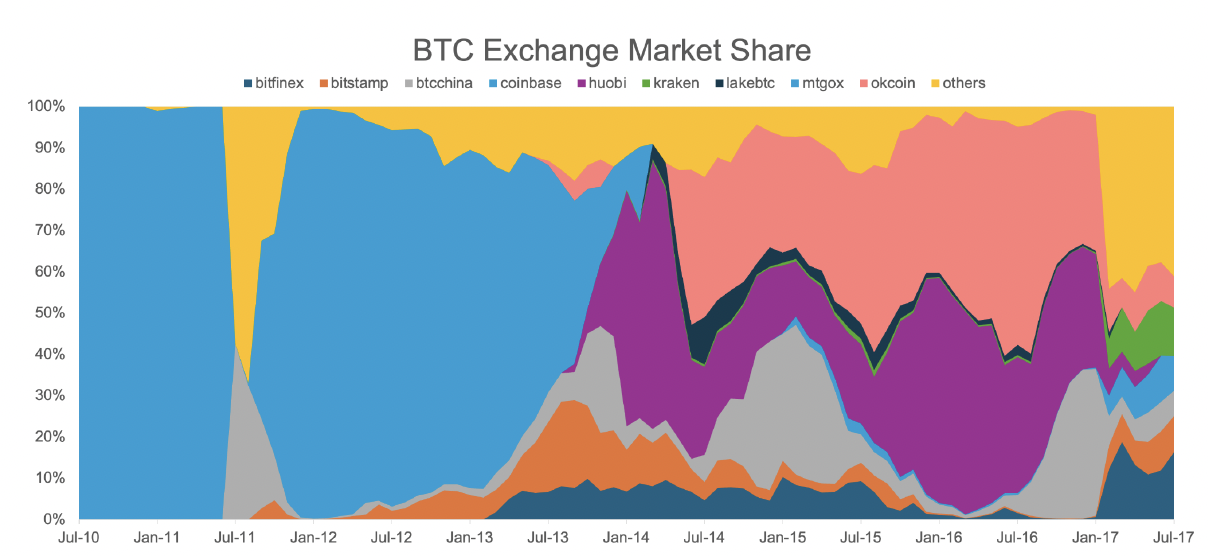

If a team builds a dedicated appchain for derivatives DEXs, they introduce a tremendous amount of friction. They need to convince users to get new wallets, they need to persuade stablecoin issuers to issue natively on their chain, they do not benefit from ecosystem flywheels that exist on general-purpose smart contract chains (e.g., a slew of tokens that can be used as collateral in the derivatives DEX, apps to compose with, users with funded wallets), and so on. Some people will claim that dYdX, Hyperliquid, and other large derivatives DEX competitors can’t possibly lose market share to a more compelling alternative—“they are too entrenched!” Unfortunately for them, history is not on their side; dominant CEXs have not stayed on top forever, and it is not uncommon for liquidity to migrate to better products. Before Binance, market share was fickle for CEXs.

Source: Bitcoinity

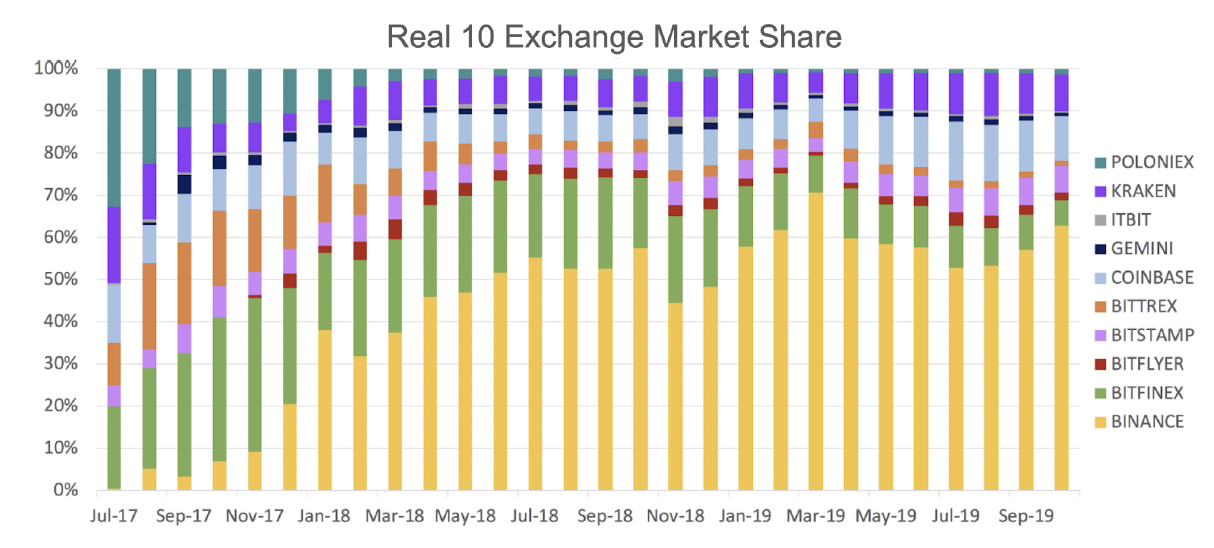

Binance created a one-time shift in the CEX market because they offered an extremely compelling product that integrated trading products and united them under a token. They launched the exchange in July 2017, and by 2018 they were the largest crypto exchange globally, with 5x more market share than any other “real 10” spot competitor. Market share can restructure faster than most realize.

Source: CoinAPI

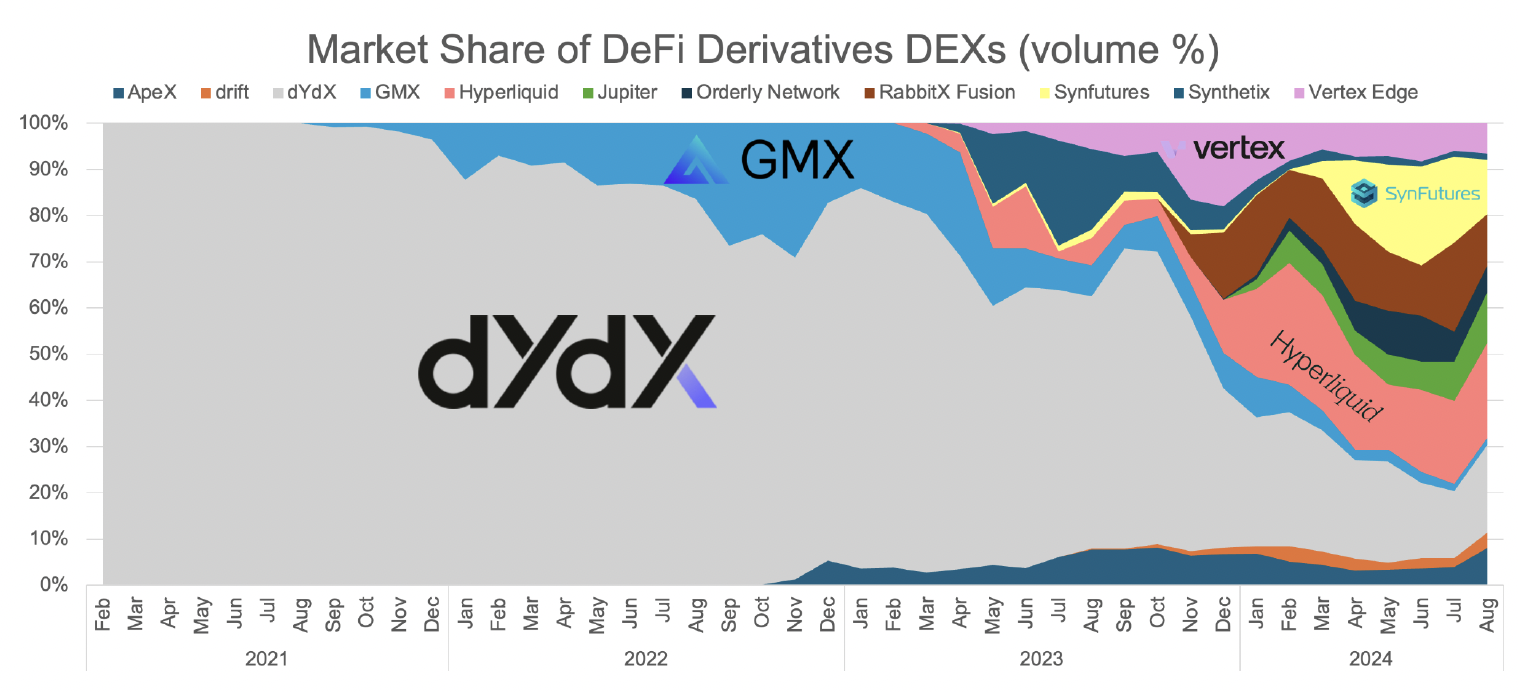

We believe Drift will be the Binance moment of derivatives DEXs. We called that shift in our original BNB report in 2019, and we are calling it again today with DRIFT. In recent times, market share has been fleeting and various derivatives DEXs have been dominant at different times:

Source: The Block

As the market begins to appreciate the elegance of Drift, we think their market share chart will look similar to Binance after they launched.

Drift Exchange

A BRIEF HISTORY OF DRIFT

We initially invested in the seed round of Drift in July 2021. The founders, David and Cindy, presented a compelling idea to build a global derivatives DEX on top of Solana utilizing a “dynamic AMM” model (DAMM). This sidestepped the need for professional Market Makers (MMs), who at the time were hesitant to provide on-chain liquidity on any chain, much less a newly launched chain like Solana was at the time.

The team launched Drift V1 to Solana mainnet beta in November 2021—effectively the top of the 2021 cycle. Incredibly, they reached $1B of trading volume in just 39 days, faster than FTX, Bitfinex, Coinbase, Uniswap, and other powerhouse exchange brands.

From there, they swiftly launched limit orders and maker orders in early 2022, and continued iterating on the product. Then, disaster struck.

During the collapse of Terra LUNA, a bug was found in the Drift protocol that created a shortfall. Fortunately, the Drift team reacted quickly, patched the bug, and rolled out a reconciliation plan to compensate impacted users. With the stumble behind them, they quickly began work on Drift V2, a complete reimagination of the product that expanded liquidity provisioning from just a DAMM to a DLOB, DAMM, and JIT. They also completely redesigned the risk engine and P&L settlement layer from scratch.

They deployed Drift V2 in November 2022, shortly after FTX collapsed and when Solana was most vulnerable. The Drift community, known as Driftors, stuck with them and continued to trade. And in May 2023, they announced a $23.5M funding round led by Polychain to help fuel growth and continue the momentum. Since V2 went live with the new liquidity provisioning and redesigned settlement layer, the protocol's performance has exceeded expectations, even through severe market volatility.

As investors, we look for intangibles. It is important to recognize how much of a slog 2H of 2022 and 1H of 2023 were for Drift. Solana was reeling from FTX, there was broad apathy from the bear market in crypto, the Solana network had recently halted several times, and maker-side liquidity was crushed across all of Solana DeFi. However, the team persisted. They did not shift strategy or abandon the Solana ship due to outages. Additionally, they did not give up on their derivatives DEX vision because of a V1 bug. They kept going where others would have easily quit.

We think persistence is a critical attribute for successful entrepreneurs. The Drift team has gone through a ton of adversity to get to where they are today, and they deserve every inch of it.

DRIFT’S LIQUIDITY PROVISIONING

Blockchains are always going to be slower than CEXs because of the inherent laws of physics. As a result, all derivatives DEXs that only support central limit order books (CLOBs) have historically suffered from worse execution than what you might see on Binance, OKX, Bybit, etc. MMs are worried about latency, because it can lead to stale maker orders being picked off before they can be canceled; therefore, they have to quote wider spreads to account for this uncertainty.

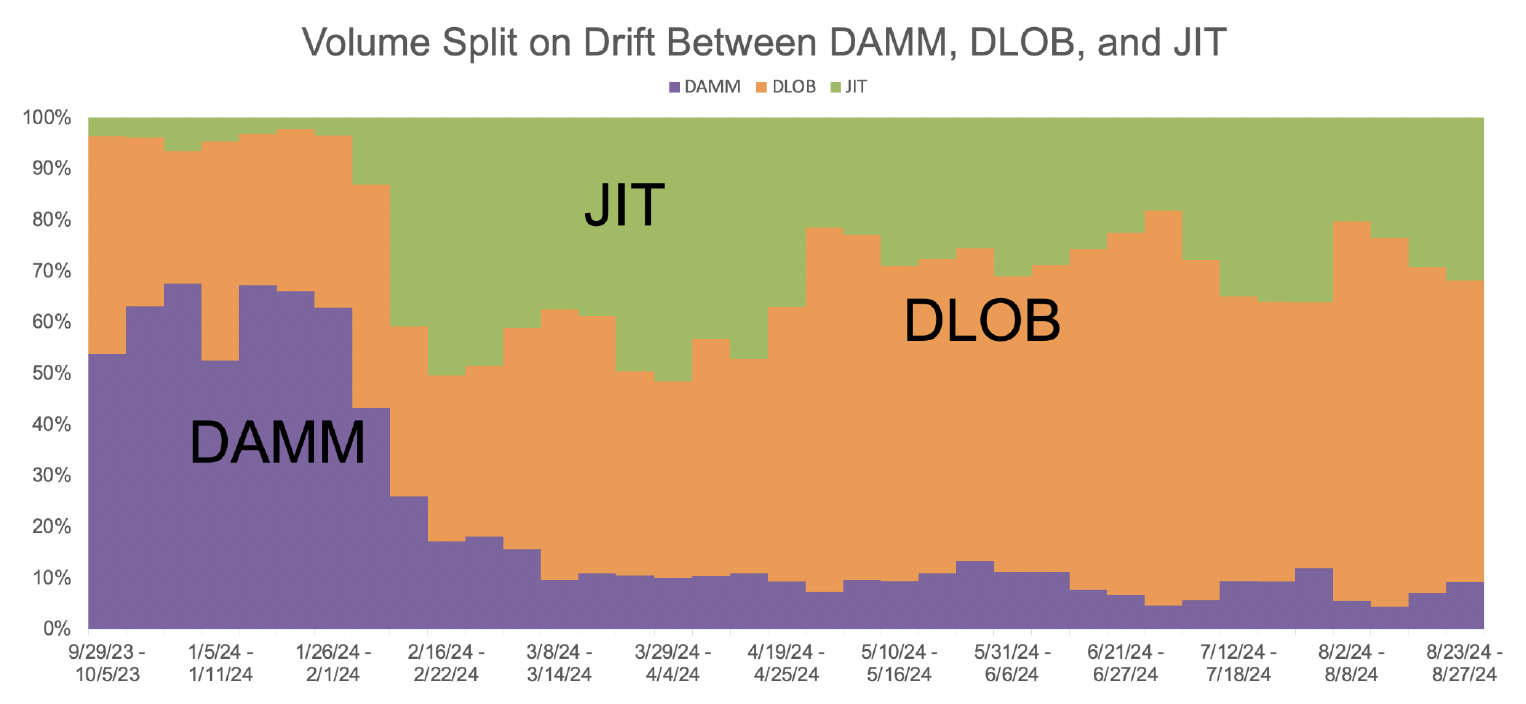

Drift is a derivatives DEX that lives on top of Solana. Drift’s primary novel feature is that it is supported by three types of liquidity provisioning, which help create tighter spreads, more reliable liquidity, and faster fills:

1. Just-in-Time (JIT) auctions — MMs can fill user market orders in a Dutch auction style format over some short time frame.

2. Decentralized CLOB (DLOB) — traders can place limit orders, and a network of keepers monitors these orders and execute them against the AMM or other limit orders (these keepers earn a % of the trading fee).

3. DAMM liquidity — if market orders are not filled by MMs, a DAMM pool provides the last layer of liquidity.

In late 2023 and early 2024, DAMM fills were the primary source of liquidity. However, in February 2024, Drift launched the Drift Market Maker Program, which resulted in major crypto MMs integrating via Drift’s APIs. This resulted in a significant shift from passive to active liquidity.

Source: Top Ledger

For mature markets, like SOL and BTC, we expect to—and want to—see more active liquidity (JIT + CLOB) because MMs are willing to quote those assets in size. In fact, active liquidity now makes up ~70% of SOL trades on Drift perp markets. Newer markets, like POPCAT and CLOUD, are more likely to have higher DAMM reliance (similar to Uniswap being the primary venue for newer, more long tail tokens on Ethereum). The net result is that MMs are quoting for large caps, providing better spreads than the DAMM would. The DAMM is acting as a backstop liquidity source, enabling perpetual trading for smaller assets that MMs are reluctant to quote. This is the beauty of Drift’s hybrid model, and it is optimized for both large cap and small cap tokens.

DESIGNING A DERIVATIVES DEX FROM FIRST PRINCIPLES

We wrote an essay titled Trade-offs in the Derivatives DEX Space in September 2020. If you have not yet read it, we suggest browsing through it before reading the rest of this report. In that report, we wrote:

“The primary objectives for a [derivatives DEX] protocol are:

1. Having very liquid markets

2. Enabling moderately high leverage

3. Keeping the contract mark price close to the fair asset price at all times

4. A robust liquidation engine that protects against insolvency and socialized losses

5. Offering the lowest trading costs (at the application and protocol level)

6. Low latency trading

7. Supporting a variety of convenient and stable collateral types

8. Cross-margining positions

9. Ability to offer synthetic exposure to arbitrary assets and contracts

10. True on-chain decentralization, or at least full transparency

In our view, the best way for a synthetic DeFi platform to attract liquidity is to optimize for the ten features listed above. However this is complex and there are many tradeoffs that must be considered.”

Drift is the first instantiation of this thesis that we have seen that offers all of these features. Let us go through them in order:

1. Liquid Markets — Drift is supported by three liquidity-provisioning methods, as described above (JIT, DAMM, DLOB).

2. Available Leverage — Drift supports up to 20x leverage for large cap assets, and 5-10x leverage for longer tail assets.

3. Mark Price to Fair Price — With more MMs integrating Drift and Solana, they will arbitrage funding rates between Drift and large CEXs that currently dominate market share. This is a case where Drift benefits from the broader Solana ecosystem because if an MM integrates one Solana DeFi protocol, it becomes substantially easier to integrate another one.

4. Liquidation Engine — since Drift V2’s inception in November 2022, there has been ~1.5M liquidations across perps and spot (per this Dune dashboard). The insurance fund in that time has grown from 0 to $28M today.

5. Low Trading Costs — Solana’s fees are lower than those of other major chains which have derivatives DEXs. Fees at the application layer are easily tunable and will respond to market conditions.

6. Low-Latency Trading— for on-chain derivatives DEXs, Drift is very competitive, though it struggles against off-chain CLOB models (instead opting for more composability).

7. Multiple Collateral Types — Drift currently accepts 25 assets as collateral, spanning both stablecoins and volatile tokens (at varying collateral weightings). dYdX and Hyperliquid only support USDC as collateral. Jupiter allows virtually any asset with no haircut. When we tested the Jupiter platform, we were able to use Jason Derulo’s celebrity coin as margin.

8. Cross-Margin Platform — every product on Drift is cross margined. So if Alice lends on Drift’s borrow/lend market, that position can be considered towards her collateral on perp markets. She can also use the same collateral intra-product across markets.

9. Synthetic Assets— Drift recently launched Drift BET, a prediction market that works the same way as its perps market. We expect that, over time, Drift will enable trading on all kinds of assets (commodities, forex, equities, etc.).

10. Decentralization — the entire Drift stack is on Solana, and it is open source, ensuring complete transparency and permissionlessness. This stands in stark contrast to appchain DEXs, particularly those with off chain order books.

We believe Drift is closest to feature parity with the large derivatives CEXs that drive most of the perps volume in crypto today. We expect them to continue iterating on the core perps product, and they have the correct construction based on first principles (three types of liquidity, and built in an open and transparent way) to continue innovating and taking market share.

Operating a global cross-margined risk engine becomes exponentially more risky and complicated on an appchain. These protocols have to account for the viability and stability of various forms of pegged assets and apply haircuts to virtually every asset used as collateral. Integrated chains like Solana are more likely to have native liquid assets that can be used as collateral, which are generally much safer vis-à-vis the same liquidity and market cap, and thus require lower discounts. As a result, Drift can be much more capital efficient for traders who get more “money for their margin”.

Alongside the core perpetuals exchange, the Drift protocol features other unique products. There are many sources of yield within Drift: borrow/lend, insurance fund staking, Circuit vaults, DLP, SuperStake, etc. You can imagine that they will add additional automated yield products in time that dynamically rebalance user deposits towards the best risk-adjusted opportunities on Drift.

Drift has evolved into a collateral platform upon which any DeFi derivative can be built. This enables traders to seamlessly collateralize their crypto, forex, prediction markets, commodities, etc., positions using a single global margin account. And those traders will be able to match trades against anyone in the world that has an Internet connection.

THE CAPITAL-EFFICIENT DEFI PLATFORM

On-chain Composability

We published our initial BNB thesis in February 2019. The crux of the thesis (besides Binance growing spot market share) was they were starting to build out an entire suite of products that catered to their existing user base, including Binance chain, derivatives, spot margin, fiat exchanges around the world, options, etc. This enabled Binance to go from effectively nothing to the world’s largest crypto exchange in a matter of six months.

Drift is the Binance moment for DeFi. The application started with perps and spot trading, added borrow/lend (as an aside: they are #2 on Solana in terms of borrow/lend assets), and most recently added a prediction market product. There is a clear opportunity for them to add options, RWAs, liquidity provisioning vaults, yield optimizers, stableswap functionality, and more over time. We expect that all of these will magically compose with one another, and the existence of each will improve capital efficiency and execution for makers and takers. As an example, Alice can use a long BTC spot position to go short TRUMP token in Drift’s prediction market (hedging her BTC position against that specific event outcome using BTC as collateral). Were she to use Polymarket, she would need to own BTC on a separate venue, and then also hold USDC as collateral to short TRUMP. Drift is much more capital efficient in this scenario, and traders will also flock to where capital is most efficient.

As they continue to build out new products, Drift will look more and more like a CEX. In fact, their north star is feature parity with Binance, in a non-custodial way. We expect Drift to become bigger than the major CEXs over a long enough time horizon.

The challenge with Binance, and other CEXs generally, is they are all zero-sum and compete viciously with each other for users with little to no room for collaboration. By way of illustration, some of the top CEXs globally—with the exception of Coinbase—are very opposed to supporting solutions like Copper’s ClearLoop because offshore CEXs want user lock-in by requiring traders to custody with them. A global cross-margining system for CEXs would eliminate a lot of market dislocations and improve capital efficiency for large traders and MMs across the crypto ecosystem, but CEXs have displayed no interest in enabling this. We highlighted this dynamic and its problems in our March 12, 2020 retrospective.

Unlike CEXs, there is a strong incentive for collaboration among DeFi protocols because better products (even if you do not benefit your own protocol directly) bring more users on chain, which leads to more ecosystem momentum, which leads to more potential users of your application. Ask yourself this: how often do you see Bybit, OKX, Binance, and HTX collaborate? And how often do you see DeFi teams on Solana collaborate? Amazingly, because Drift lives on chain, it’s not hard to imagine a world where they cooperate with all kinds of other DeFi applications (alongside their own in-app composability).

We see a world in which a new crop of prime brokers (PBs) pop up that are DeFi-native. Looking back at the collapse of Three Arrows Capital, and even Archegos Capital in TradFi, the problem was that none of the lenders knew the size of the borrowing hedge fund’s positions across all brokers, their correlations, and their overall risk. In DeFi, we could see specialist PBs extend credit on chain that are algorithmically bounded. For example, a PB could enable a market neutral fund to deploy a basis yield strategy on Drift in an undercollateralized way, but the capital would algorithmically be constrained to move to Drift (and other whitelisted protocols and contracts). The PB would have full visibility into the lent funds and liquidate them at a layer above Drift should they need to.

The opportunities for on-chain composability with other protocols is effectively boundless, and we are just now starting to see what can happen with global, permissionless finance APIs.

Off-Chain Composability

We briefly touched on on-chain composability before, but an underrated form of composability for Drift is off-chain composability. We define on-chain composability as DeFi legos. We define off-chain composability as the benefits an app gets by being part of a broader ecosystem.

Here is a simple example of off-chain composability: a new user to the Solana ecosystem can receive SOL via TipLink, a low-friction onboarding experience that allows anyone to send a money link to anyone else. The onboarded user can easily buy a Helium hotspot and start earning HNT rewards. She can swap her SOL on Jupiter for USDC, then deposit the USDC into Drift, and hedge her future HNT earnings. Upon receiving HNT rewards, she can swap them for USDC, make a wager on Drift BET (Drift’s prediction market), and then transfer her Drift BET winnings to purchase an NFT on Tensor. She can do this all with one wallet natively on the Solana blockchain.

If the DEX aggregator was on Optimism, but the derivatives exchange was on Arbitrum, and the DePIN network was on Base, she would have to bridge at every step, incurring a large amount of latency and slippage costs. The user flow would break entirely.

The biggest bottleneck to growth in crypto, and DeFi more specifically, is getting wallets into the hands of millions of users. We have long said DeFi is a second-horizon activity. Once users have funded non-custodial wallets—and do not need to buy SOL, ETH, etc. on Coinbase and then withdraw it to a wallet—they will use DeFi because it is the cheapest and most convenient financial rails for them. As an example, Helium miners were at one point 10% of Jupiter users.

We think Solana has the best shot of onboarding millions of users and getting them wallets (of which they only need one!), and thus Drift will disproportionately benefit from that because any user with a Solana wallet can tap into Drift’s liquidity with no bridging, new wallet, etc, required.

Drift’s Growth Story

Drift has grown tremendously since emerging out of the brutal 2022 bear market. The team has relentlessly shipped since then and perfectly encapsulated a phoenix rising from the ashes (we like those at Multicoin).

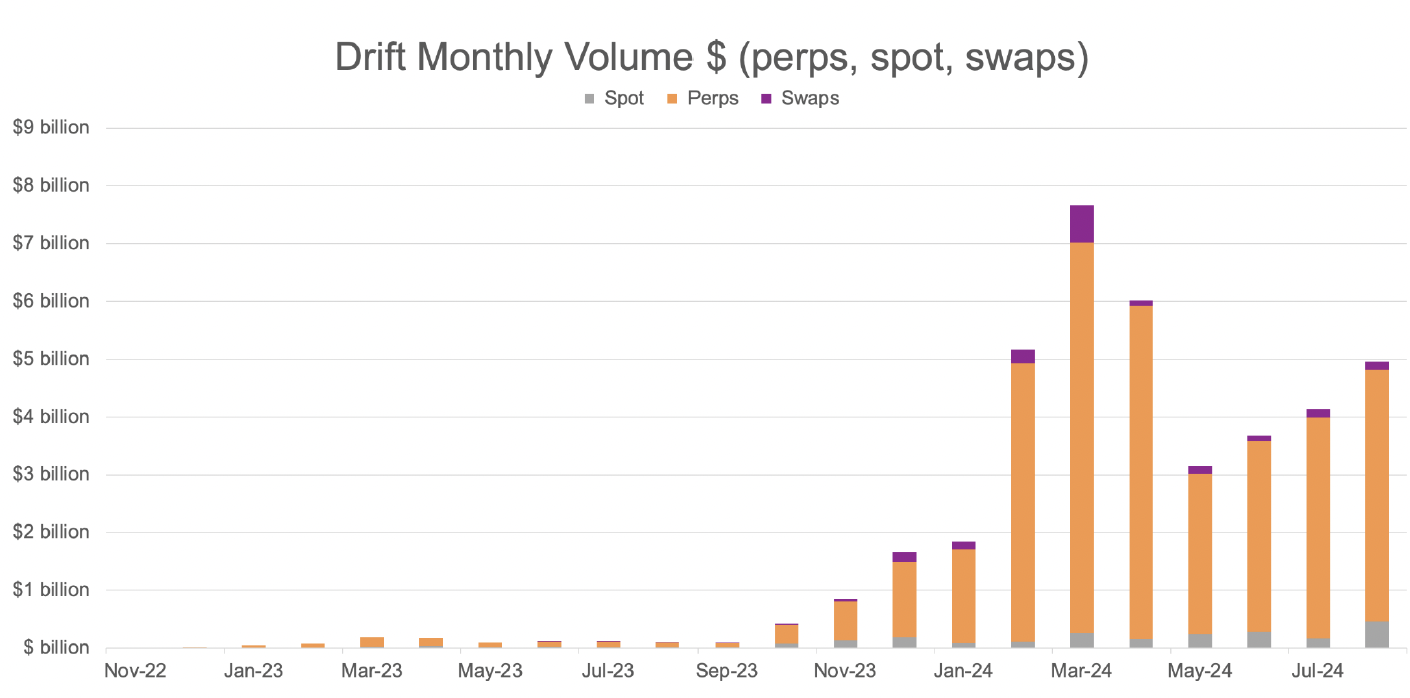

Approximately $5B was traded on Drift across perps, spot, and swaps in August 2024, representing an increase of 50x(!) in volume year over year—cumulative volume across perps, spot, and swaps in August 2023 was ~$97M. This is the most important metric for Drift because running an exchange and matching service is an extremely high margin business, and it is the core product offered by Drift today. Significantly, the majority of the increased activity has come from perps.

Source: Top Ledger

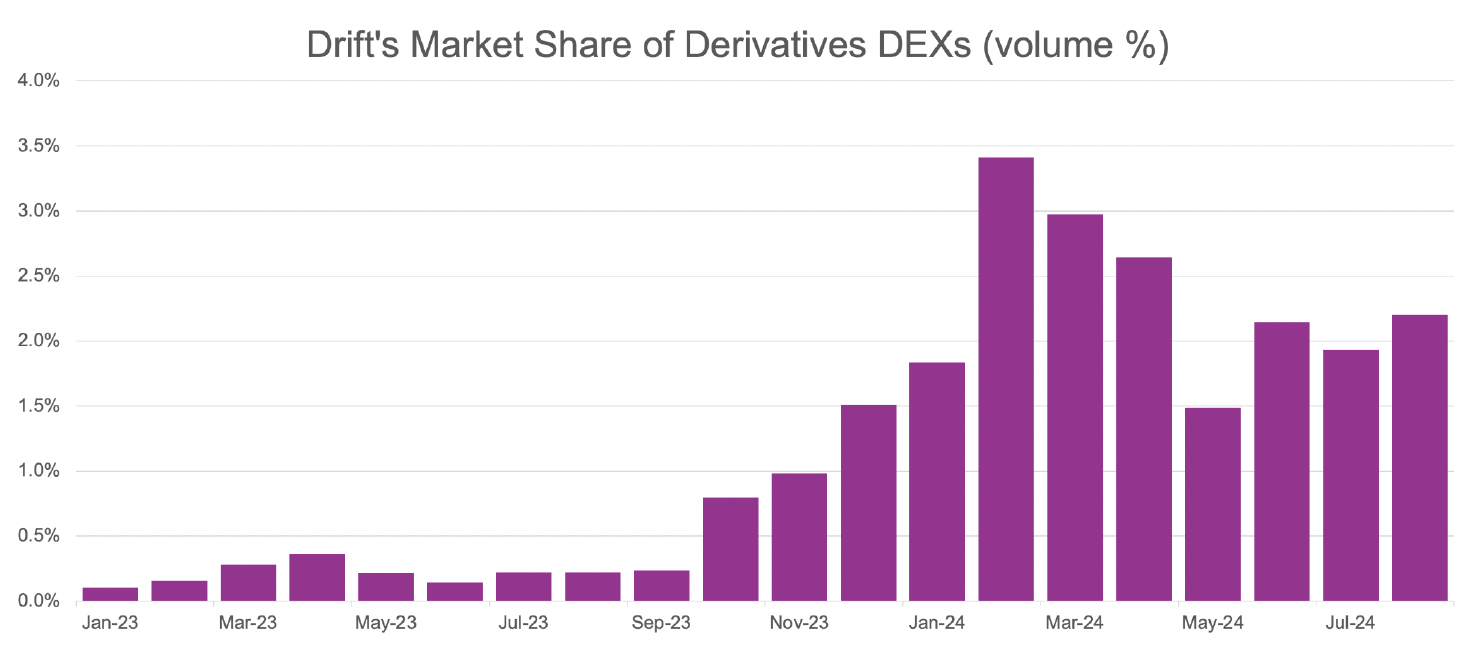

While volume growth is important on an absolute basis, it is also worth considering whether Drift’s market share is growing. In their most important market (perpetual contract trading), Drift has ~10x’d their market share against competitors over the last 12 months. On an absolute basis, their market share is still small (2.2%), which leaves ample room for growth.

Sources: The Block, Top Ledger

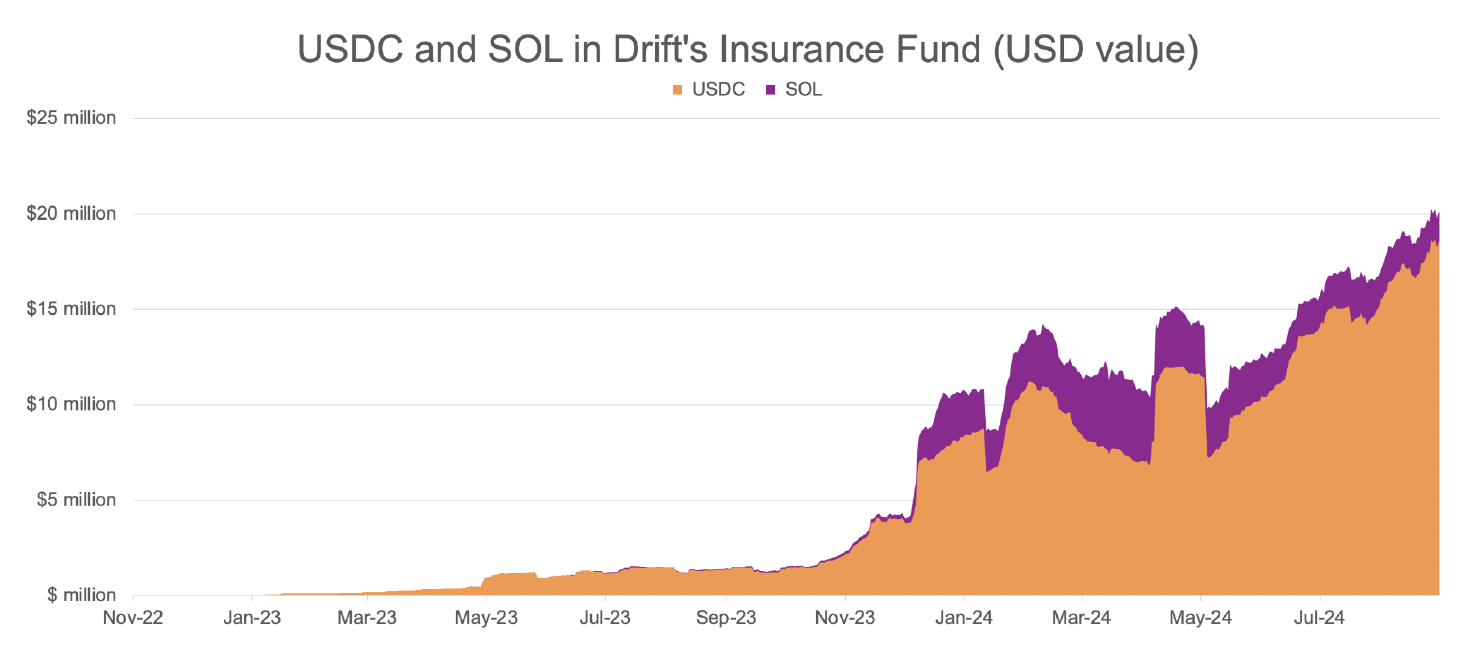

Relatedly, Drift’s insurance fund has grown from ~$1.5M at the end of July 2023 to over $20M of USDC and SOL at the time of writing (with another $5M of DRIFT staked that is not included in the chart because the token recently launched and it would bias the chart upwards, and $3M of other less liquid tokens also not included).

Source: Top Ledger, Investing.com

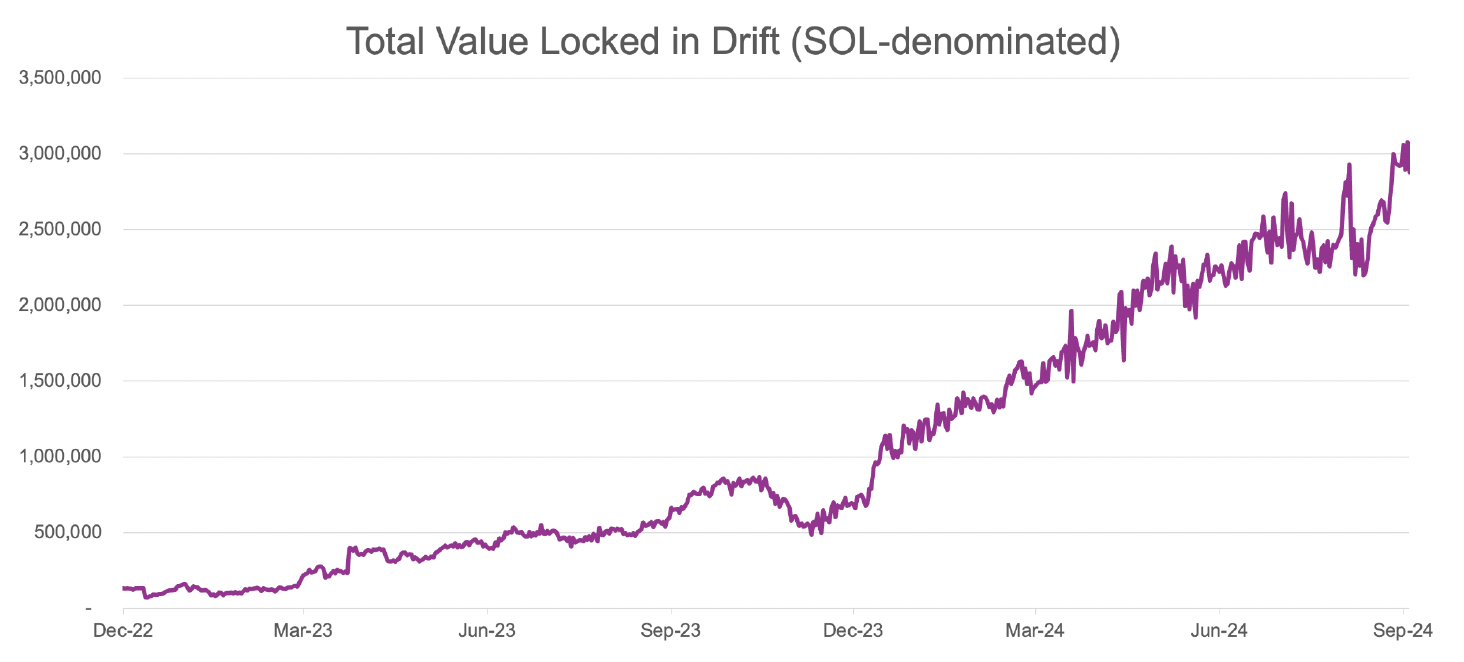

“Total Value Locked” (otherwise known as TVL) is not a perfect metric; in fact, in a lot of cases it can be counterproductive (e.g., too much TVL for a spot AMM relative to taker volume implies a capital inefficient protocol). However, the collateral sitting in Drift, both for lending and derivatives margin, is useful to track. We think it is relevant to look at SOL-denominated TVL (though the USD denominated TVL chart looks similar), because underlying price volatility does not skew the data.

Source: Artemis, Investing.com

We include all of these charts to make a specific point, which is that the existing Drift product suite is a growth story. Even after the DRIFT airdrop, which occurred on May 16, 2024, Drift’s core protocol metrics are still going up and to the right.

As we elaborate further below, we think there will be a liquidity migration from Ethereum and L2s, as well as appchains, over to Solana, and Drift is best positioned to capture that liquidity for derivatives. As such, we expect these metrics to continue increasing.

The Solana Tailwind

Multicoin has been investing in early-stage crypto projects and public tokens for seven years. We have looked at every “hot new” category that has emerged, and our primary conclusion after this time is that public blockchains are primarily useful for two things: 1) trading and 2) payments. And the most important considerations when building a trading or payment application are 1) latency and 2) cost.

Across the entire L1, L2, and L3 landscape, we have repeatedly held that Solana provides the most clear way to get low latency and low cost without sacrificing composability.

Going into Solana’s annual developer conference—Breakpoint—in November 2022 (just prior to the collapse of FTX), we were quite excited about Solana. We thought the ecosystem had matured to a point that it could present a credible challenge to Ethereum. Unfortunately, the FTX collapse set the ecosystem back by 12 months. Throughout most of 2023, most capital markets participants (mainly speculators) left Solana for dead. But the core ecosystem teams—including, without limitation, Dialect, DFlow, Drift, Drip, Helium, Hivemapper, Hubble/Kamino, Jito, Jupiter, Magic Eden, marginfi, Marinade, Metaplex, Orca, Phoenix, Pyth, Raydium, Solend, Squads, Tensor, and TipLink—continued to build, mostly under the radar.

By Breakpoint 2023, the ecosystem achieved enough momentum that some market participants started to re-examine their priors about Solana, and very importantly, started to play around with it. In our opinion, they were all generally impressed, and started buying SOL and using Solana regularly.

Today, most DePIN projects rely on Solana. These projects include Hivemapper, Helium, Render, io.net, Kuzco, Teleport, GEODNET, etc. Similarly, both private companies, such as Stripe (link), and major Fortune 500 fintech companies, such as Visa (link) and Paypal (link), have selected Solana as their venue (or one of a few venues). Additionally, with the rollout of token extensions earlier this year, Solana is now capturing meaningful RWA market share. In fact, Hamilton Lane recently launched a credit fund on the Solana blockchain. The Solana snowball is rolling downhill.

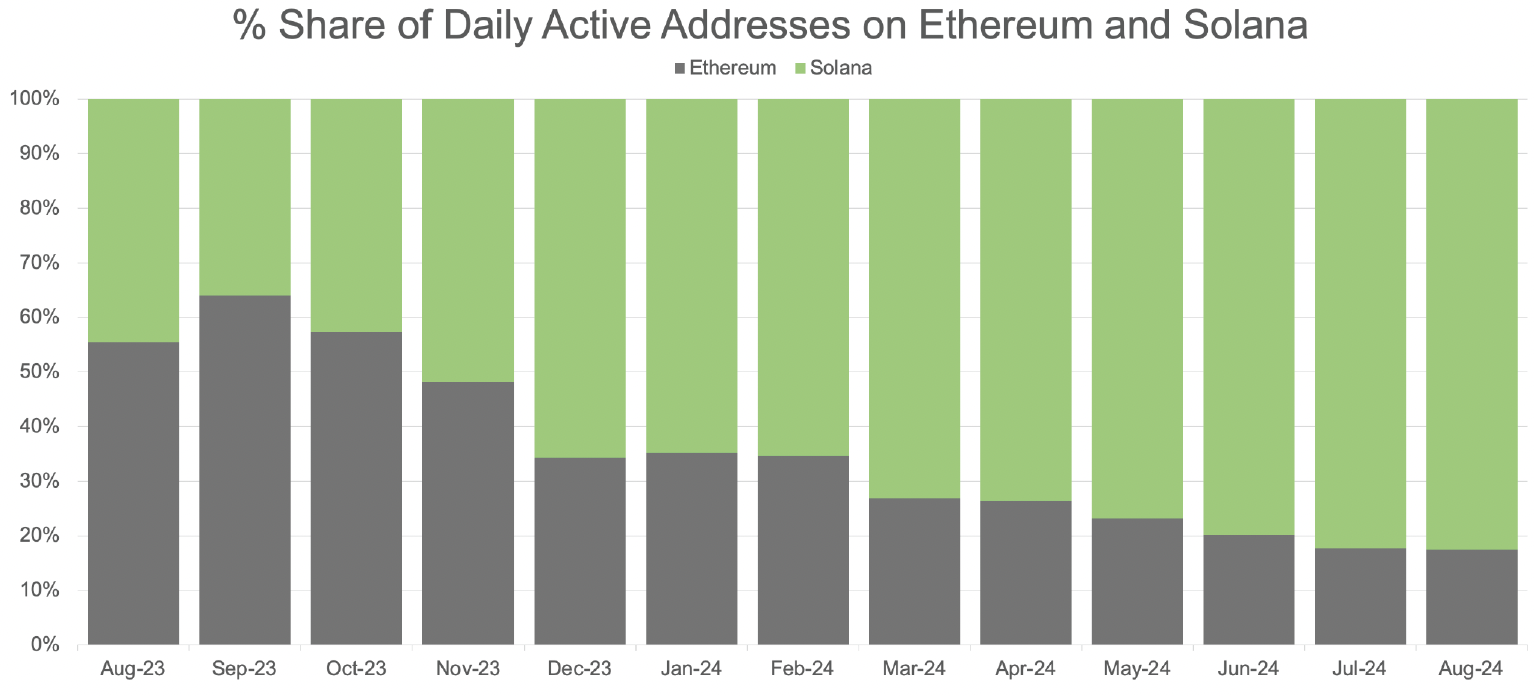

Solana’s success as of late can be seen in the uptick in usage relative to Ethereum and other modular networks. User activity on Ethereum has been decreasing relative to Solana, we believe both as a function of poor UX, high latency, and high fees, as well as increased reliance on L2s (which cannibalize ETH’s primary value capture mechanism, which is MEV).

Source: Artemis

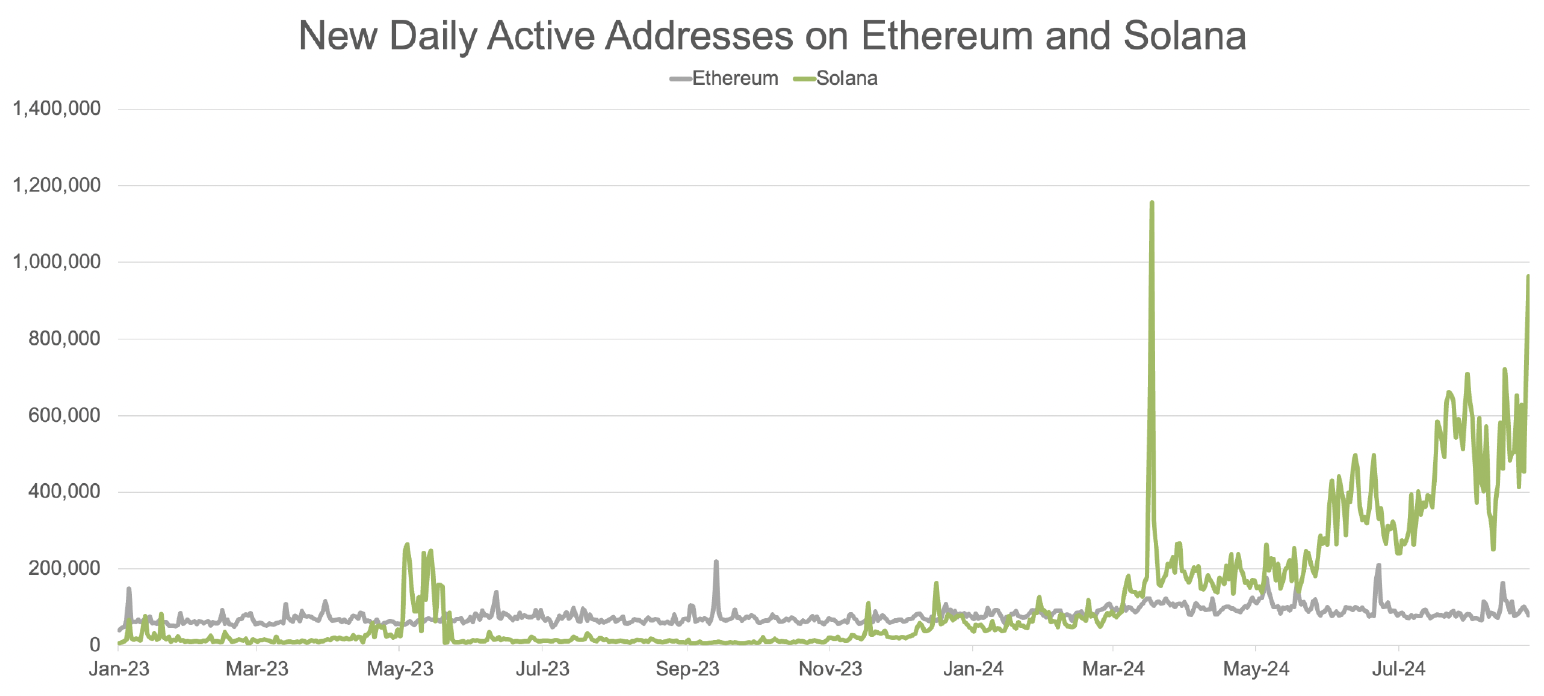

Daily Active New Addresses on Solana meaningfully flipped Ethereum L1 on a consistent basis over the last quarter, illustrating the user migration from expensive transaction environments to Solana’s low-cost environment.

Source: Messari

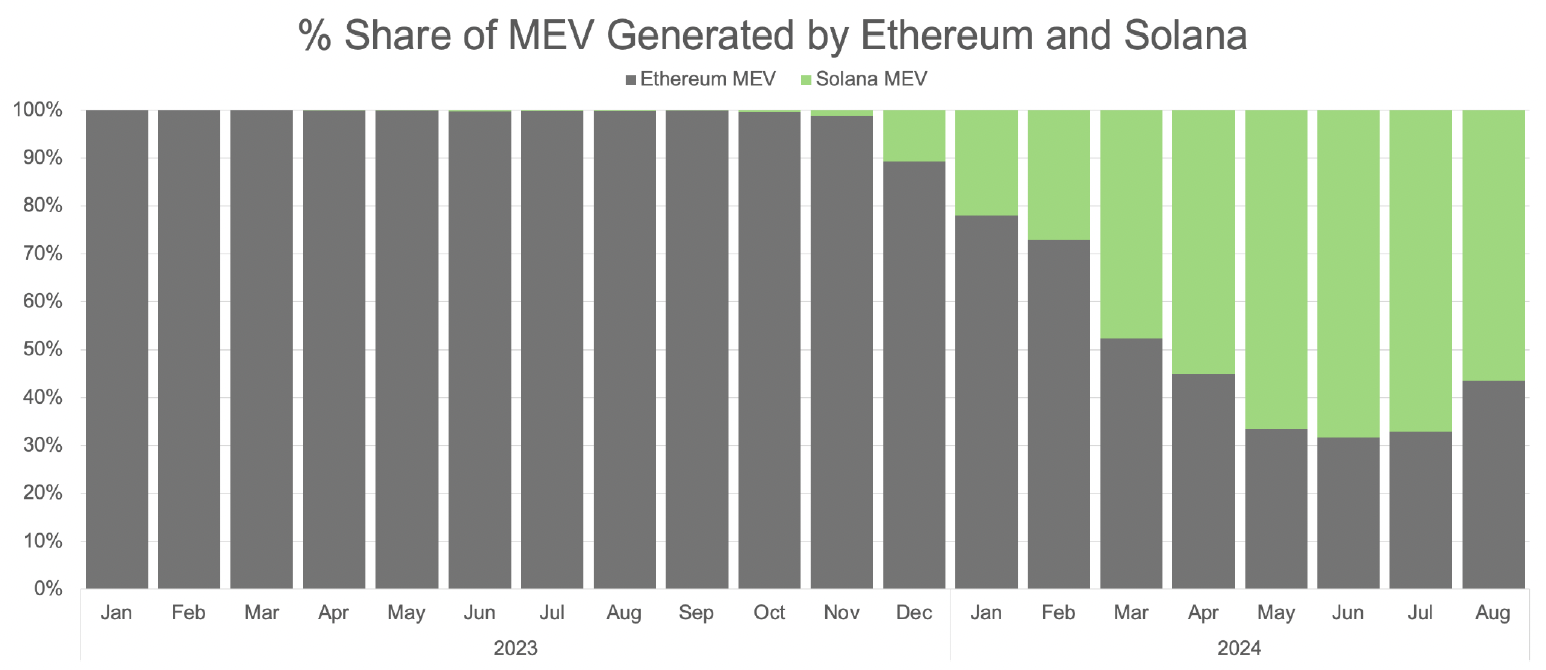

In Q1 2024 we also saw Solana generate more MEV than Ethereum for the first time, as evidenced in the chart below. This is significant because, until recently, it was a widely held belief that Solana would never eclipse Ethereum’s economic activity. However, over the last six months, Solana has routinely flipped Ethereum.

Source: Blockworks Research

We expect the momentum for Solana to continue through the end of the year and well into 2025, buoyed by the rollout of Firedancer and the annual Solana developer conference Breakpoint, which is in Singapore in a few weeks.

Firedancer is a new validator client that is being built by Jump Trading, one of the largest high frequency trading firms in the world. Jump Trading is building Firedancer with networking speed and performance as the main focus, and they are uniquely qualified to do so given their decades of experience building low latency trading systems. Firedancer is expected to be much more performant than the current Solana client and thus will materially help Solana DeFi protocols and their users. Since Firedancer is written in a different language than the existing Solana client, a single bug or glitch in either client should not theoretically impact the entire network. Multiple network clients thus dramatically increase Solana’s resiliency in addition to making it faster.

Drift Token

DRIFT is the native token of Drift. Crypto investors, including us, have (rightfully) been skeptical about certain DeFi tokens’ abilities to capture value for a long time. Questions arise such as:

● Which entity, token holder group or lab co, actually earns revenues from the protocol?

● Can a protocol’s token be forked out?

● Does the token suffer from the velocity problem?

● Does issuance from liquidity mining lead to wash trading, and is the protocol incentivizing fake usage?

● Is there utility value that can be gained by using or holding the token?

We believe that DRIFT is a compelling asset that possesses many of the attributes we’ve been talking about for years that encapsulate how a DeFi token can become valuable under the right design and circumstances.

We previously introduced the “equation of exchange tokens,” a term we coined while doing due diligence on Binance. It is as follows:

Exchange token network value = value created by exchange * efficiency of token value capture

“Value created by exchange” is how the exchange business is performing on a fundamental level. Examples include trading volume, daily/weekly/monthly users, website traffic, trust, liquidity, ability of management to execute, etc. We have highlighted Drift’s growth story in this essay above, and also their opportunities to expand their business beyond “just another DeFi perps exchange.”

The other part of the equation relates to the token itself. In examining derivatives DEX tokens, we think the opportunity for value capture is clear. The basic premise of our thesis is that some DeFi protocols have inherent risk associated with them. Owners of these protocols’ native tokens are primarily responsible for governing that risk and ensuring the protocol remains solvent. They also take on the risk of being diluted or slashed in the event there is a shortfall. For managing the system and taking on the risk of there being an insolvency, those token holders must be compensated via fees from the protocol. Drift enables a ton of leverage, and thus DRIFT token holders have a substantial amount of risk to manage.

There are additional benefits that can also come from holding the DRIFT token. These include fee discounts on trading, governance on choosing a risk council, tiered increases for referrals, etc. The DRIFT token recently launched, and we expect the community to quickly vote for these value capture mechanisms, following in the footsteps of BNB and other exchange tokens before it.

Drift Valuation Framework

We assume for the purposes of our valuation model that 100% of revenues that flow through the DRIFT protocol will accrue to token holders (the Drift team has not implied any value will be captured at the front-end layer). Importantly, 100% of protocol revenues today are accrued to a token governed treasury pool. Because Drift is governed by the community, we do not know precisely whether the revenue will flow through via passive/active treasury management, direct payouts, buy and burns, etc., but we expect within the next 1-2 years it will be obvious one way or another.

DEXs—both derivatives and spot—are some of the best businesses on the planet because they have margins that can almost approach ~95%. CEX margins are also fantastic, but they have to pay for customer support, global licensure, servers, big custody management systems, etc. Uniswap famously was doing 77% of Coinbase’s volume during 2021, with 33x fewer employees. For our valuation model, we ignore expenditures because the protocol is sustainable already, and in the long state economic equilibrium we believe it will be a 90%+ margin business.

For this valuation, we will use a cash flow multiple methodology. We assume that Drift protocol revenue (which currently is entirely directed to the token governed treasury) will be captured through some mechanism to the DRIFT token.

DEFI DERIVATIVES

DeFi derivatives market share is currently 4.9% of all crypto derivatives (per The Block Pro and DefiLlama data). We predict that DeFi derivatives will achieve 10% market share by 2027, which we think is very reasonable, if not too conservative.

We also project that the market for crypto derivatives broadly 2x’s in three years’ time (which we also view as conservative). Today, the total market for crypto derivatives is ~$48T annualized across CeFi and DeFi. In our model, that would mean total crypto derivatives volumes are ~$96T annualized in 2027, and DeFi derivatives volumes are $9.6T annualized (~4x August 2024’s annualized realized volume). Note that none of this requires any sort of synthetic trading of RWAs, as we project this growth can come only from native cryptoassets.

As U.S. markets are currently blocked by all major perps CEX and most derivatives DEX front ends, one material area of potential growth that we are not accounting for with precision is the U.S. user. DeFi regulation is uncertain and will materially vary the potential TAM for U.S. and, to a slightly lesser extent, E.U. markets. Current market size accounts for this lack of clarity, and thus we assume zero U.S. market access for the foreseeable future in our model. Absent material electoral changes in November, we do not expect to see broad, permissive regulatory change (whereas change could stimulate far greater TAM growth not accounted for in our model).

BORROW/LEND

DeFi borrow/lend borrow outstanding today is ~$11.77B (excluding $5B of DAI), per Token Terminal and Solana DeFi websites. This has grown at 64% CAGR since Aave's launch (higher if you extend farther back). We conservatively estimate this will 2x by 2027, implying $23.54B of loans outstanding in DeFi.

Lending protocols monitored by Token Terminal generated $1.7M in revenue over the past week, implying $88.4M of annualized revenue * 2x = $176.8M. At 5% market share, this would be a ~$9M revenue line for Drift. They are currently ~55 bps in market share.

We do not include spot exchange in our valuation because Drift is a small player currently, and we view the business line as call option value.

VALUATION MODEL

In order to derive our valuation model for DRIFT, we have established a framework of key assumptions that we believe to be the base case2. In summary, our base case assumptions are:

● Total crypto derivatives volume doubles in size by 2027.

○ CeFi derivatives volume grew at 63% CAGR between 2019 - 2024, per The Block Pro data.

● DeFi derivatives will be 10% of the market for crypto derivatives by 2027, up from 4.9% today.

○ DeFi’s market share in crypto derivatives has grown at 56% CAGR over the last 2 ½

years, per The Block Pro and DefiLlama data.

● Drift will capture 10% of the DeFi derivatives market by that time, up from 2.2% today.

○ Drift was at 0.22% market share in August 2023, per The Block, Top Ledger, and DefiLlama.

● Drift is able to capture a 4 bps net take rate.

○ Actual August 2024 realized net take rate was 5.6 bps (conservative because we include spot and swap volumes in the denominator, which are lower margin revenue lines for Drift today), per Top Ledger.

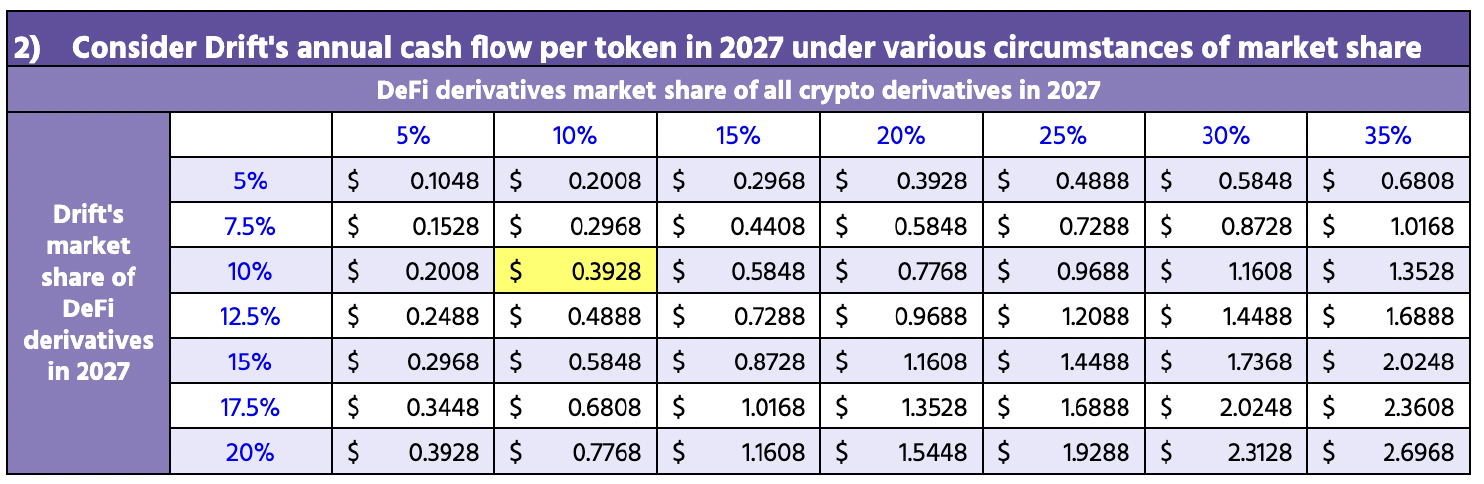

In our valuation model, which explicitly assumes (1) modest market growth, and (2) Drift capturing a higher percentage of DeFi activity based on a superior product, we arrive at a plausible scenario in which the Drift protocol is generating ~$392M of annualized revenue, or $0.3928 per token (as depicted in the table below). This does not include more speculative revenue opportunities such as Anatoly Yakovenko, Solana’s founder, recently claiming 75% of MEV will be captured at the application layer.

For context, in August 2024, Drift generated ~$2.8M of revenue, or ~$33.5M on an annualized basis. 12x revenue growth in three years, when the protocol 50x’d volumes and 10x’d market share over the past 12 months, with substantial looming Solana DeFi tailwinds, does not sound crazy to us.

We do not explicitly claim that DRIFT should be worth $X because of DeFi borrow/lend or derivatives DEX token comps because there are several outliers and crypto markets can remain irrational over short timeframes. However, as a point of reference, we looked at relatively mature DeFi protocols and their respective price to “sales”3 multiples (per Token Terminal data):

● AAVE trades at a 37x P/S multiple

● MKR trades at a 23x P/S multiple

● LDO trades at a 22x P/S multiple

We also examined the principal derivative DEX tokens (per DefiLlama and Token Terminal data):

● DYDX trades at a 135x P/S multiple

● GMX trades at 14x P/S multiple

As a contrast, DRIFT currently trades at approximately 14x P/S. Given the comparables, we think 25x as a base case revenue multiple is quite appropriate. In the “bear” and “bull” case, we simply decrease/increase the price to sales multiple, but do not adjust our underlying assumptions regarding the market and Drift’s capture of market share.

● Bear case multiple of 10x = 0.3928 X 10 = $3.928

● Base case multiple of 25x = 0.3928 X 25 = $9.82

● Bull case multiple of 50x = 0.3928 X 50 = $19.64

We must then discount from 2027 to 2024. We apply a 40% annual discount to capture the significant risks that Drift is able to take market share in the DeFi derivatives market, and that the market grows. 40% discount rates are considered appropriate for mid-stage business ventures (given DRIFT is a publicly tradable asset, we believe the discount rate is fair). This implies a discount factor of (1 + .4) ^ 3 = 2.744:

● Bear case: discounted value of $3.928 / 2.744 = $1.43

● Base case: discounted value of $9.82 / 2.744 = $3.58

● Bull case: discounted value of $19.64 / 2.744 = $7.16

The key assumption and driver is on the derivatives side. As a result, if Drift does not capture substantial market share in borrow/lend or spot, we will not expect a massive impact in the model.

We did our best to avoid “garbage in, garbage out” modeling as much as possible, but there is bias in every model. We encourage the reader to go through this exercise on their own time. If you would like to play with our assumptions, we have attached a download-able spreadsheet that you can modify based on your market assumptions and value drivers. Link here.

Summary

Drift is going to be the Binance moment for derivatives DEXs. Market share has come and gone in the DeFi derivatives space, much like it did for CEXs before Binance came along, but we think Drift is going to emerge as the key winner in this market.

We have conviction in this belief because Drift has designed the correct derivatives DEX construction from first principles. We do not view appchain derivatives DEXs to be the correct path long term and we expect market share to eventually work its way over to Drift as traders come to appreciate the capital efficiencies that Drift offers.

In the last 12 months, we believe the Solana ecosystem has provided incontrovertible evidence that it is the most viable public blockchain that can actually fulfill the primary vision of crypto: a permissionless, low-cost, low-latency asset ledger for everyone in the world. Most people still have not recognized this, even though the facts are there in plain sight. And further, Drift is the most compelling derivatives DEX on Solana because of composability, its three types of liquidity provisioning, its liquidity platform and path to be a superapp, and the team’s dogged persistence in the face of adversity.

Drift’s north star is a generalized DeFi derivatives platform underpinned by a liquidity layer that any derivative can be traded or cross margined on top of, in a completely open, noncustodial, and permissionless way. We expect hyper-localized, third-party front ends to emerge on top of Drift’s liquidity layer all over the world. These customer-face applications will compete on user acquisition, fiat on/offramp pricing, UX experiences catered towards specific geographies, etc. — all while not having to build out smart contracts or aggregate liquidity themselves.

Drift’s cumulative volume across perps, spot, and swaps is up ~50x year over year, with most of the growth attributable to their core product: perps. Their market share in DeFi derivatives increased ~10x over that same timeframe, but it is still small with plenty of room to run. It is an extremely high margin business, with clear future value capture look through for DRIFT token holders.

In summary, based on the assumptions laid out above and using our valuation model, we think DRIFT is sharply undervalued at its current price of $0.46. Our thesis is that Drift will continue to eat market share in a growing derivatives DEX space, and that the protocol and token will compound as a result. Our base case price target is $3.58.

Important Disclosures

Multicoin Capital Management LLC (“Multicoin”) provides investment advice to certain private fund clients (the “Fund(s)”) that own DRIFT tokens discussed herein and stands to gain in the event that the price of the token increases. Multicoin is adopting a “No Trade Policy” for the Funds and for Multicoin’s officers, directors, and employees, which restricts the purchase and sale of DRIFT tokens for three days following the public release of this report (“No Trade Period”). Following the No Trade Period, the Funds are free to buy or sell DRIFT tokens (and Multicoin’s officers, directors, and employees may trade subject to certain pre-clearance procedures). The DRIFT tokens held by the Funds are marked for the Funds’ valuation purposes using Fair Market Value pursuant to Multicoin’s Valuation Policy, which valuation methodology is accounting-based and differs from the valuation methodology used in this report. The valuation methodology used in this report is opinion based, provided solely for the purposes of discussion, and should not be relied upon as the basis for purchasing or selling DRIFT or any similar token and may differ materially from the accounting-based valuation methodology used by the Funds. This report’s estimated valuation only represents a best efforts estimate of the potential valuation of DRIFT, and is not expressed as, or implied as, assessments of the quality of a token, a summary of past performance, or an actionable investment strategy for an investor.

Multicoin believes that the information provided herein is reliable as of the date of publication, and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. The information is presented “as is,” without warranty of any kind – whether express or implied. This post may contain links to third-party websites (“External Websites”). The existence of any such link does not constitute an endorsement of such External Websites, their content, or their operators. These links are provided solely as a convenience to you and not as an endorsement by us of the content on such External Websites. The content of such External Websites is developed and provided by others and Multicoin takes no responsibility for any content therein. Charts and graphs provided herein are for informational purposes solely and should not be relied upon when making any investment decision. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in this report are subject to change without notice and may differ or be contrary to opinions expressed by others.

The content is provided for informational purposes only, and should not be relied upon as the basis for an investment decision or for valuing tokens. The contents herein are not to be construed as investment, legal, business, or tax advice.You should consult your own advisors for those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Multicoin, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Multicoin is available here:https://multicoin.capital/portfolio/. Excluded from this list are investments that have not yet been announced (1) for strategic reasons (e.g., undisclosed positions in publicly traded digital assets) or (2) due to coordination with the development team or issuer on the timing and nature of public disclosure. This report does not constitute investment advice or an offer to sell or a solicitation of an offer to purchase any limited partner interests in any investment vehicle managed by Multicoin. An offer or solicitation of an investment in any Multicoin investment vehicle will only be made pursuant to an offering memorandum, limited partnership agreement and subscription documents, and only the information in such documents should be relied upon when making a decision to invest. Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the potential complete loss of principal.

The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. These forward-looking statements may turn out to be wrong and can be affected by inaccurate assumptions or by known or unknown risks, uncertainties and other factors, most of which are beyond Multicoin’s control. When investing you should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all tokens discussed in this document and develop stand-alone judgment of the relevant markets prior to making any investment decision. Past performance does not guarantee future results.

•

•

•

Affiliate Disclosures

- The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- The author is not being compensated in any form by the target in relation to this research.

- To the best of the author’s knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

Neither BIDCLUB nor PHATPITCH LLC represents or endorses the accuracy or reliability of any advice, opinion, statement or other information displayed, uploaded, or distributed through BIDCLUB by any user, information provider, or other party. PHATPITCH LLC is not a broker, a dealer, or investment adviser. Nothing in BIDCLUB constitutes an offer or a solicitation to buy or sell any securities. BIDCLUB prohibits the sharing of material non-public information (MNPI), but assumes no responsibility for member conduct or associated risks. Nothing in BIDCLUB is intended as specific investment advice and no individual should make any investment decision based on any recommendation or analysis provided on BIDCLUB. You acknowledge that any reliance upon any such opinion, advice, statement, memorandum, or information shall be at your sole risk, and you bear sole responsibility for your own research and investment decisions. See full

Terms and Conditions.

Well researched with some spicy takes

I have a couple questions tho

1) perp exchanges tend to trade at low P/Es and P/Ss. Why do you think that is?

2) i agree with the problems regarding appchains, but what about rollapps/network extensions? such as what zeta is doing