Across

ACX

Target Name

Across

Ticker

ACX

Strategy

long

Position Type

token

Current Price (USD)

0.27

Circulating Market Cap ($M)

108

Fully Diluted Market Cap ($M)

268

CoinGecko

Long $ACX as a play on ERC-7683 adoption by UniswapX

15 Oct 2024, 06:05am

MARKET OVERVIEW

As DeFi and the broader crypto landscape continues to evolve, new challenges like MEV protection, liquidity fragmentation, and deteriorating UX are consistently arising. Intent-based solutions are now emerging as a promising approach to tackle these challenges. From the user’s perspective, suppose Alice wants to trade her USDC on Ethereum for WETH on an L2. Traditionally, Alice would have to go through multiple steps including transferring USDC to her wallet, connecting to a bridge and transferring the USDC to the L2, then connecting to a DEX and executing a swap transaction.The process is complex and time-consuming. With intents that outsource execution to a network of solvers that compete to fill orders, Alice doesn’t need to take multiple steps or worry about how it happens. Intents-based systems simply allow users to specify their “intent”, which determines the end state of the chain — and a network of solvers compete to fulfill the user’s outcome as fast and cheaply as possible. There are two main benefits of intent-based design:

User experience — Intent-based systems offer a seamless and fast process. Users simply express their intent, and solvers handle the execution. Features like gas abstraction and Just-In-Time (JIT) liquidity contribute to a smooth, "one-click" experience reminiscent of Web2 apps.

Execution efficiency — Professional market makers (MMs) acting as solvers manage transaction execution with greater expertise than basic AMM contracts or end users. Their specialized knowledge allows for building more optimized on-chain transactions that further enhance capital efficiency.

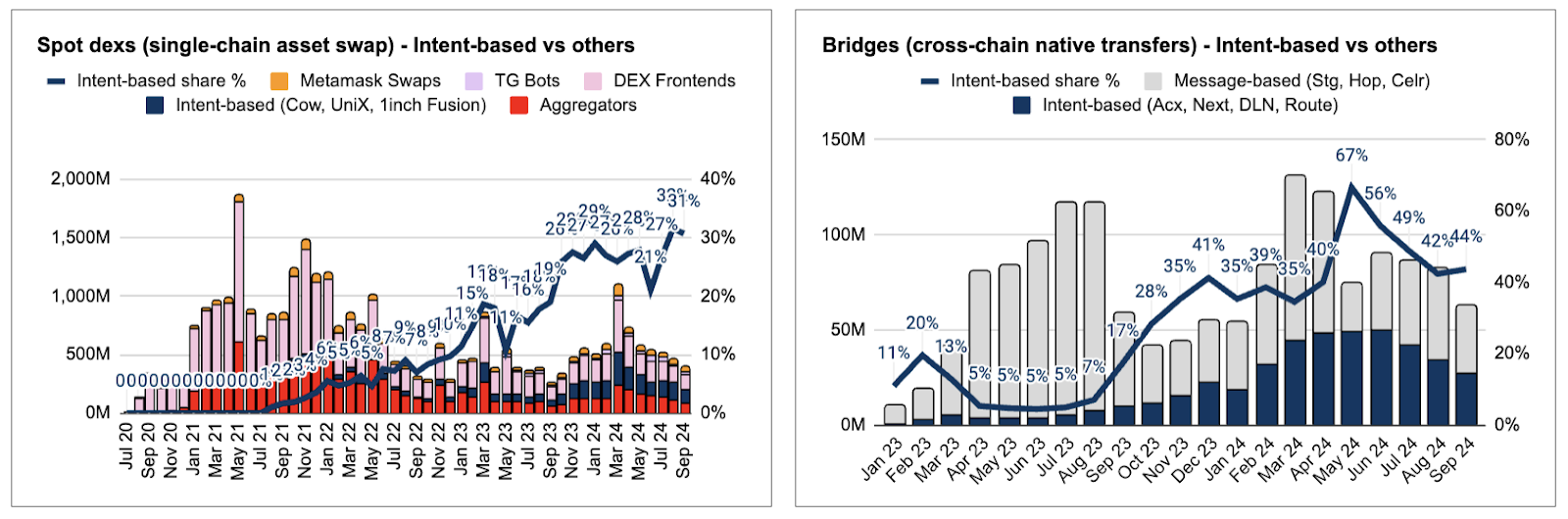

Given these advantages, intent-based solutions have been gaining significant traction in DeFi, particularly in spot DEXs and bridges. While not yet widespread in perp DEXs, we anticipate significant adoption in this sector in the coming months.

Intent-based spot DEXs or swaps (e.g., UniswapX, Cowswap, 1inch Fusion) function as aggregators with MEV protection, prioritizing the best execution for swappers. Expanding on the aggregator analogy, the protocol acts as an aggregator of solvers, with solvers aggregating on-chain and off-chain liquidity. Thus, combining intents with an order-flow auction (OFA) users get better pricing, as they source liquidity from different venues, and lower fees, due to benefiting from auction proceeds in the form of surplus rebates, compared to traditional on-chain swaps. For instance, on CoW Swap, users typically receive an average token surplus of 0.5% (also known as “execution welfare”) on volumes, indicating the price improvement facilitated by solvers.

Intent-based bridges (e.g., Across, deBridge, Router, Everclear), where users submit an intent to bridge tokens from Chain A to Chain B, and solvers are tasked with finding the optimal routing. This approach enables faster bridging times -3 seconds- (vs messaging-based bridge approaches like Stargate that take 40 seconds) by allowing solvers to take on finality risk and bridge optimistically. Once the transaction on Chain B is confirmed, the solver receives user funds on Chain A, along with execution fees.

Intent-based perp DEXs (e.g., SYMMIO) allow users to submit intents for opening positions, which are broadcast to market makers (MMs). This creates a decentralized OTC desk with bilateral trading agreements. When an MM fulfills an intent, an on-chain agreement is formed with both parties locking collateral. This offers advantages over AMMs and CLOBs-based perps. Unlike AMMs, which rely on passive LPs with limited asset variety, intent-based systems leverage MMs who can source liquidity from various venues, giving users access to global liquidity and asset exposure. Compared to CLOBs, intent-based systems reduce the need for high-throughput on-chain interactions as MMs only need to interact on-chain when they opt to fulfill a user’s intent.

ERC-7683 UPCOMING LAUNCH - ACROSS AS THE BEST PROTOCOL TO CAPITALIZE ON INTENT-BASED CROSS-CHAIN SWAPS AND BRIDGING PENETRATION

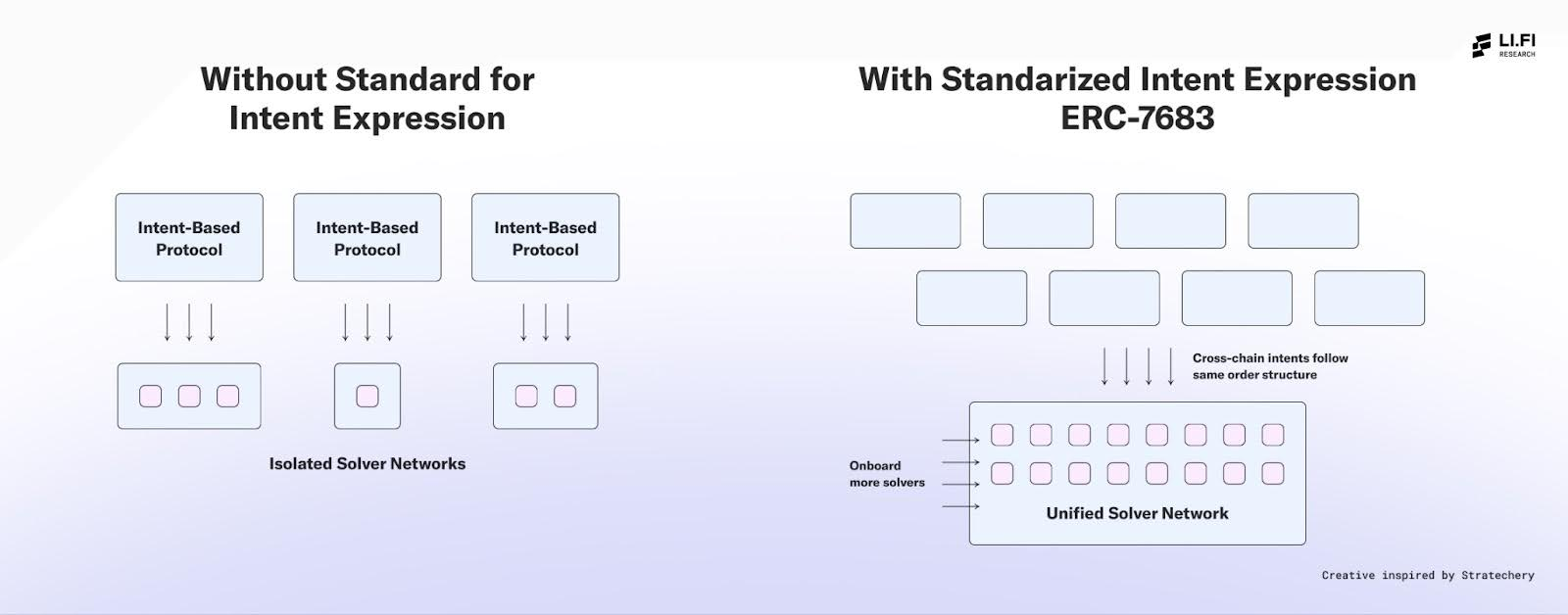

The current landscape of intent protocols consists of individual siloed protocols tailored for specific use-cases. We are not seeing many solvers being shared and solving on different OFAs (even single-chain intent-based spot platforms like UniswapX, CowSwap and 1inch Fusion aren’t sharing solvers and infrastructure). One of the main reasons for this is that running an intent solver is complicated and requires expertise in building highly performant software as well as managing cross-chain inventory risk (high barriers of entry). By standardizing the intent structure what ERC-7683 aims is that a solver written for one dApp, like UniswapX, could be easily reused to solve for other cross-chain intent-producing dApps like Across and CowSwap. In doing so it increases the aggregate capital efficiency of the solver network active liquidity.

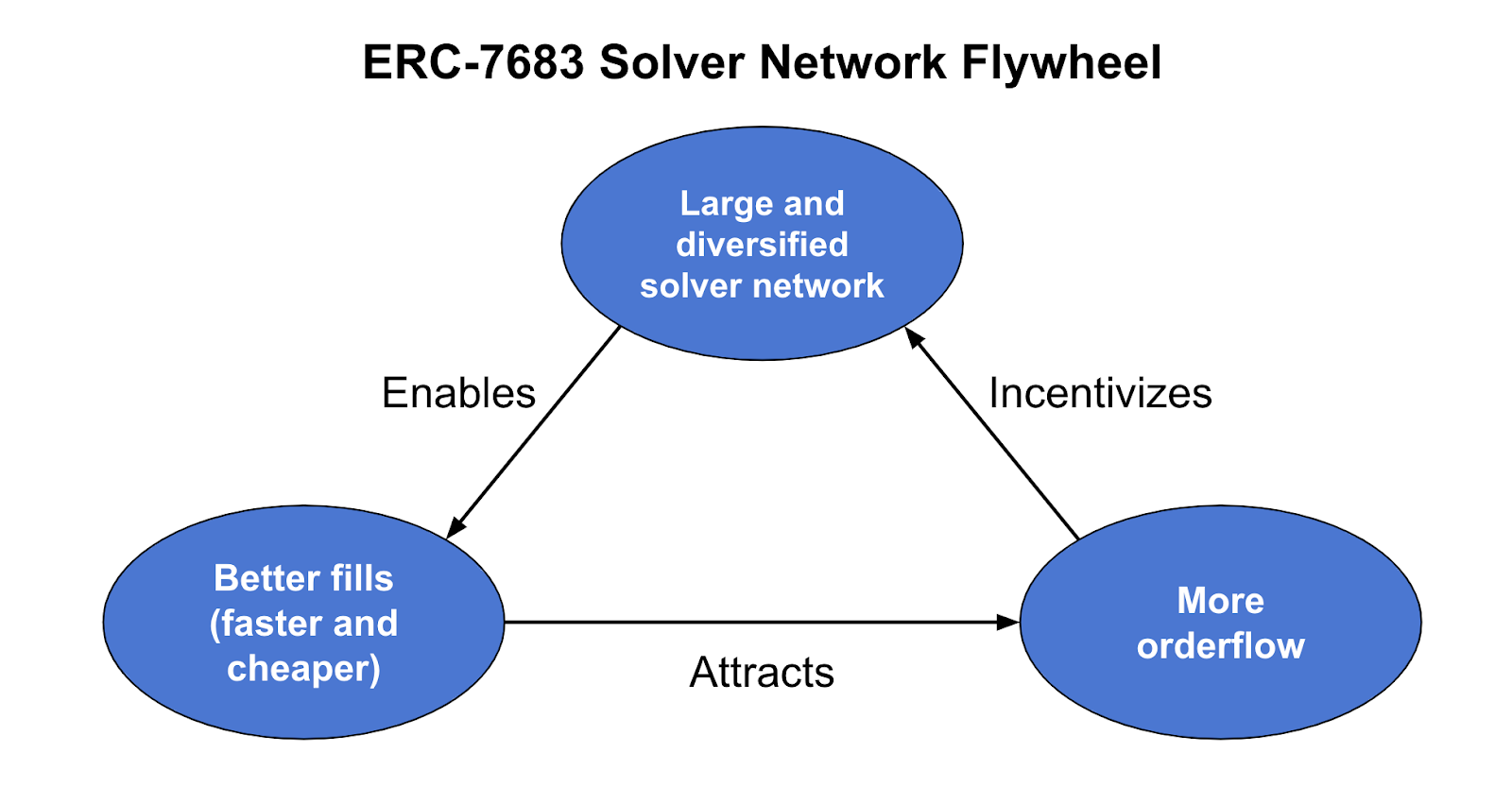

Furthermore, by reducing the solver’s complexities involved with intent solving, the ERC-7683 standard facilitates one of the biggest MOAT a solver network can have, which is having a large and diversified network of solvers and MMs with inventory that compete with each other to provide fast and cheap fills. This mirrors the “liquidity begets liquidity” phenomenon that we have seen on DEXs: A large-liquidity DEX pair offers better prices to swappers, a large solver network offers better execution, in terms of price and speed, to intent users. It is a network effects game, more solvers lead to better execution (price and speed), attracting more order flow, which in turn incentivizes more solvers to join. By standardizing intent-orders, ERC-7683 helps bootstrap this network, creating a powerful MOAT.

What’s the TAM → DeFi actions that will be covered by ERC-7683

Erc-7683 focuses on cross-chain intents DeFi use cases, which should cover >90% of all on-chain cross-domain interactions-. This mainly include bridging (cross-chain native asset to native asset transfer), cross-chain swaps (cross-chain limit order swaps), but that fundamentally is also extendible to pretty much every DeFi action that you can think of on a cross-chain context as every financial interaction can be expressed as a swap, or combinations of swaps:

AMMs

Adding/Removing Liquidity -> send one or multiple tokens to a pool, receive a LP token.

Swaps -> user sends one of the designated tokens, receives the other token at a determined exchange rate.

Lending

Opening a loan -> user sends collateral token, receives loan token.

Closing a loan -> user returns loan token + interest, receives collateral token.

Perps

Opening a position -> user sends collateral tokens, receives tokenized or LP position (receipt).

Closing a position -> user returns LP token and receives gain/losses.

Bridges

Bridge transfer -> user sends tokens to bridge contract. User is sent tokens by a solver on the destination chain. Then the solver receives the user’s token on the origin chain.

Looking into intent-based bridging and cross-chain swaps we can estimate the TAM with the below assumptions:

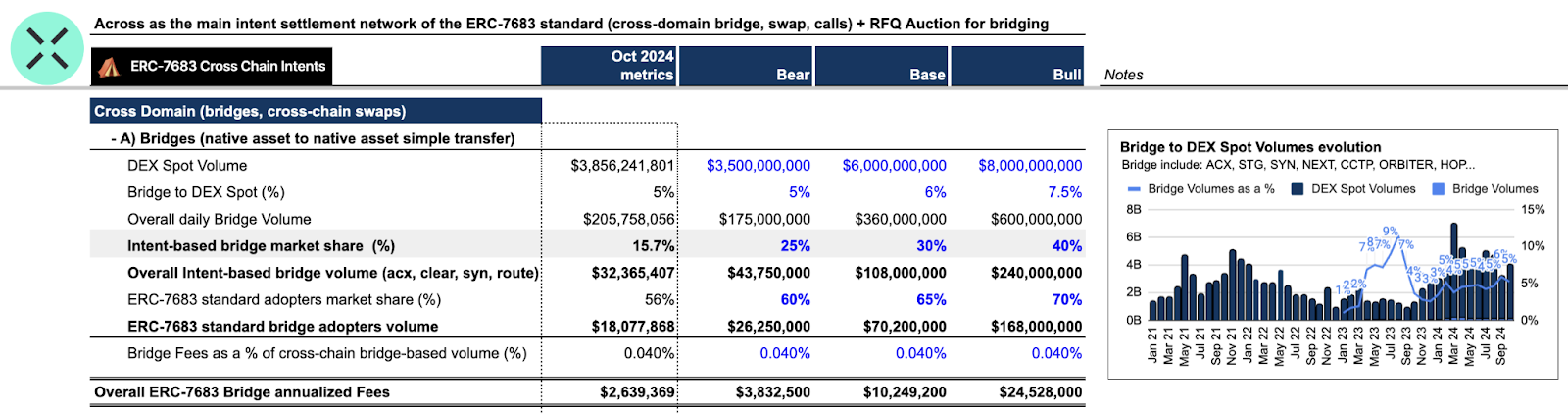

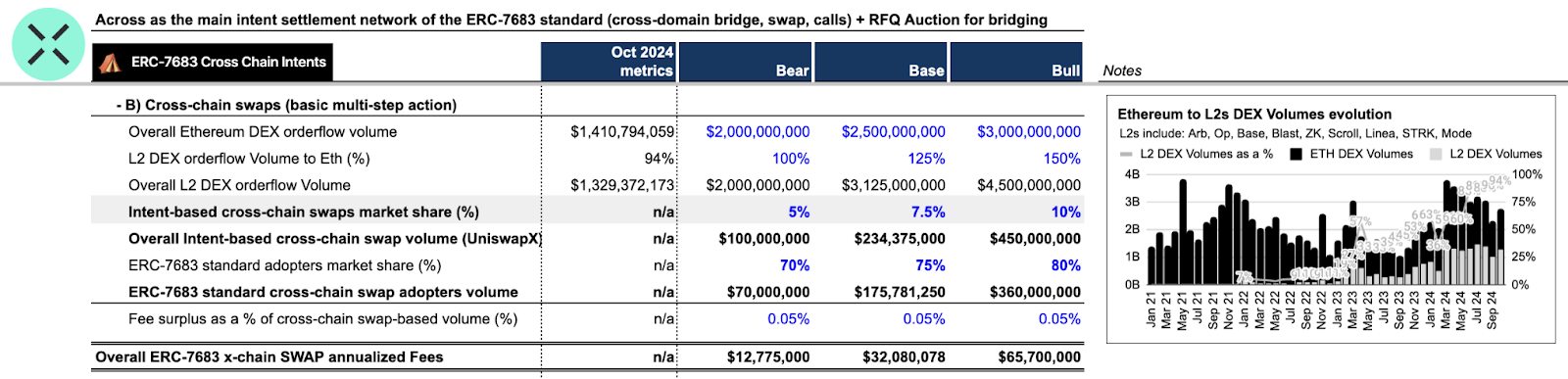

For bridges, the framework is that as more L2s keep launching, the demand for bridging activities between these different ecosystems should increase (at least in line with the historical DEX Spot Volume to Bridge Volume ratio). Furthermore, giving the UX benefits that intent-based bridges bring to users, we should expect more of these protocols to pivot to this model. As such we expect the market share to increase from the current 15% to 25-40% across bear, base and bull, and for ERC-7683 standard adopters to gain share vs non-adopters (reasoning is the previously mentioned MOAT effects of having an already bootstrapped large and diversified solver network). Lastly, fees as a % of volume have been contracting, but appear to have stabilized around 3.5bps (which we believe is the long-term rate that will be charged).

Intent-based 7683 Bridging TAM

For cross-chain swaps the framework is similar. As on-chain traction continues moving to L2s (also driven by the launch of more L2s), the L2 DEX Volume as a % of Ethereum should continue trending up, and we expect it to reach 100-125% across bear, based and bull in the next 12 months. Furthermore, cross-chain swaps will be needed as much as ever as this unifying layer of the complexity that all these different ecosystems will bring. As such, we model their penetration as a % of L2 DEX Volumes, with 5-10% across bear, base and bull, which are conservative numbers based on the penetration we have been seeing on single-chain swaps (currently at 30% of Ethereum non-toxic DEX Volume). In terms of ERC-7683 adoption market share between upcoming cross-chain swap protocols, we expect them to follow similar market share dynamics to what we saw when Uniswap launched, with a winner-takes-all distribution. Lastly, for Fees the methodology is different than with bridge based transactions, and here we look at the Fee surplus as a % of cross-chain swaps. We conservatively estimate this to be 5bps but we have been seeing cases on CowSwap of it being >50bps, and it will majoritarily depend on the slippage set by the user on their limit order (with the default being normally set at 50bps).

Intent-based 7683 x-chain SWAP TAM

Value Flow in ERC-7683→ Market structure and key players

To present how those bridge and cross-chain swap fees will be distributed we have to first present the market structure of ERC-7683 and who are the key players involved:

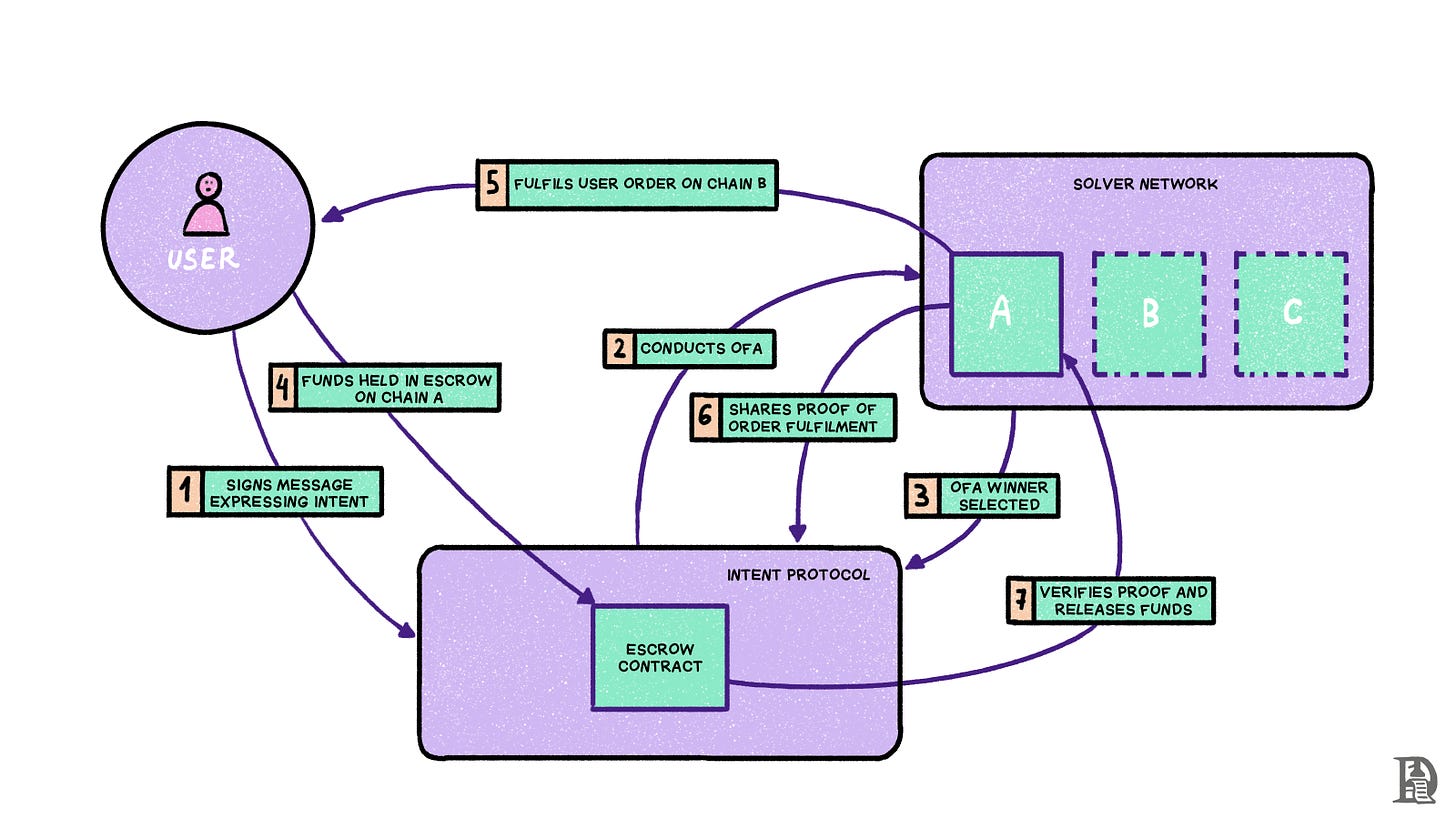

Small walkthrough of how cross-chain intent-based systems -bridge, swaps- work with solver networks:

Source: Decentralized.co

A user starts by expressing intent to reach an end state. The types of intents that ERC-7683 enables can be broken down to three: a) “bridging”, b) “swapping” or c) “calls” (cross-chain multi-step actions supported by Across+: bridge+ deposit, stake, buy or mint NFT…). For example, a user may want to spend 300 USDC on Base to get at least 0.1ETH on Optimism, which would be b) a cross-chain limit order swap.

The intent protocol then holds an auction (whether on-chain or off-chain), called the Order Flow Auction (OFA), where solvers compete to fill this intent. Based on the auction design, the protocol selects a solver and holds 300 USDC as escrow on Base.

The chosen solver then sources the liquidity required to fulfill the user's order of 0.1ETH on Optimism either using on-chain LPs or its own private liquidity.

Once fulfilled, the solver shares a proof of successful fill or completion with the protocol. There are different types of proofs that can be used for proving intent fulfillment. For example, Across currently uses an optimistic challenge mechanism (powered by UMA Optimistic Oracle), but is working on modularizing this part for enabling heterogenous trust and security models that may be faster without too many security tradeoffs.

The settlement protocol verifies the proof and releases the escrowed funds, settling and repaying back the solver. Fees from filling the user intent are implied from the spread between the dollar value of what the user escrowed on the origin chain and what the solver fulfilled him with in the destination chain.

As such, broadly speaking, the key players involved are:

Intent Generators: dApps or users initiating cross-chain actions that may have their own OrderFlow Auction’s (OFAs), such as Across and UniswapX.

Solvers: sophisticated actors competing in an auction to have the right to fulfill those intents.

Settlement Networks: Networks that verify intent fulfillment and handle solver repayments.

Source: Hackmd blog by Nick from Archetype/Across

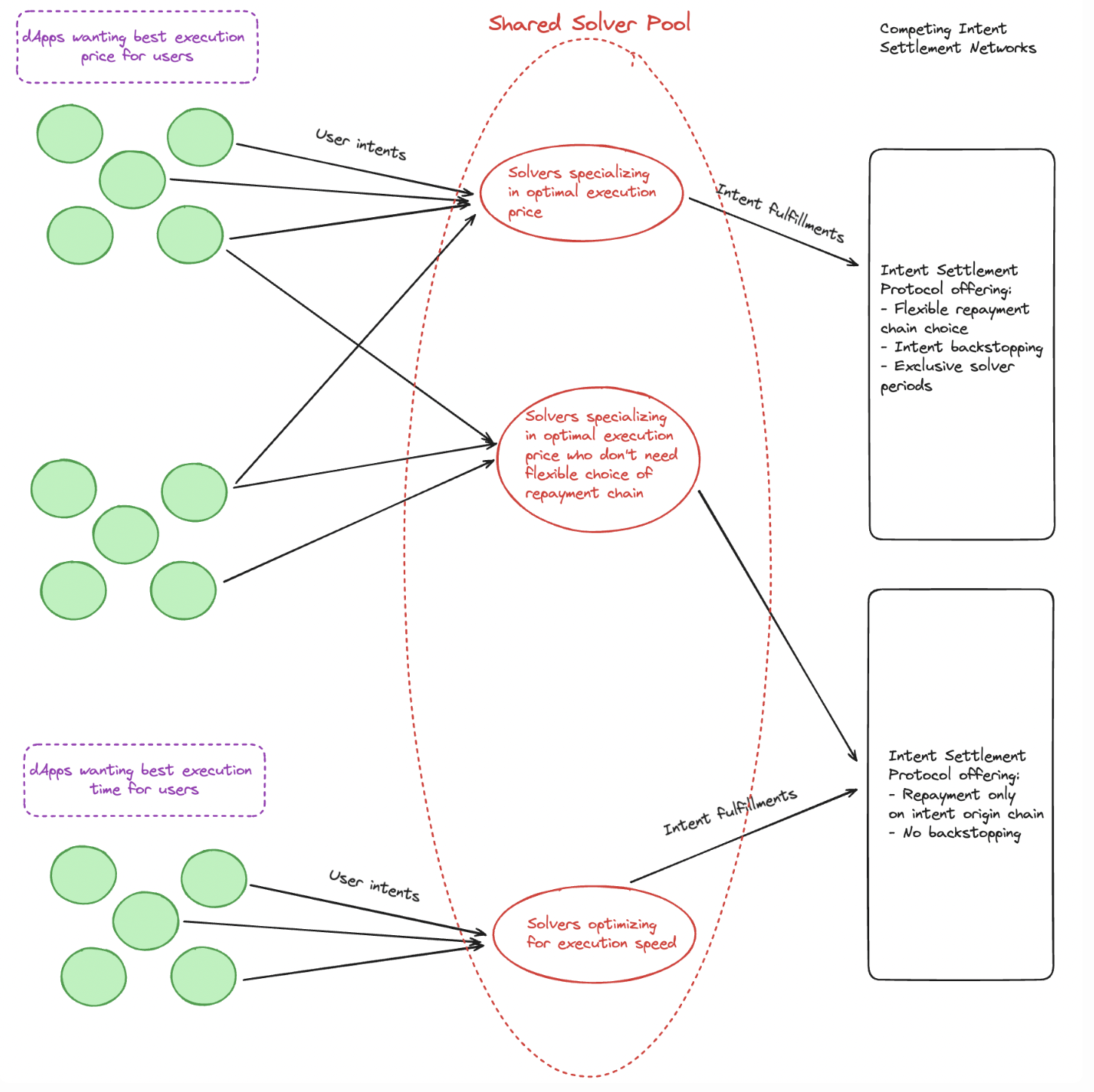

As the complexity of becoming a solver gets reduced (thanks to efforts like ERC-7683 or Inventory Access Layer protocols like @nomial_io), the middle solver layer or pool should get commoditized, with resulting value flowing to the edges (1. upstream to orderflow originators and OFAs auctioneers, and 2. downstream to Settlement Networks) where Across is strategically positioned:

1. Across’ Request-for-Quote (RFQ) auction for bridge transfers: Under Across’ current implementation model, there is MEV that gets leaked to L2 sequencers, as the solver competition to win orders is currently happening on-chain. Given L2 sequencers work with a mechanic ordered by priority fees, if two solvers have the same latency, then the way one wins the order is through paying extra priority fees to front-run its solver competitor. This leads to some value lost from a) outbidding more than necessary by the winning solver, b) value lost from the gas fee involved with on-chain TX reversion by the losing solver. This value is leaking to unintentional recipients (L2 sequencers that are receiving the priority fees) and an off-chain price RFQ auction would enable Across as the auctioneer the possibility to:

Lower the user fee to the fee resulting from the new off-chain RFQ auction, potentially reducing fees from 4 bps to 2.5 bps due to increased solver competition.

Maintain the fee take rate of 4bps for the user, and internalize that 1.5 bps spread as an “auction fee”, as long as competitive platforms charge similar take rates.

Hybrid-> only pass down 0.5 bps as price improvement to the user, and internalize the other 1 bps, so their resulting fee for the user goes from 4 bps to 3.5 bps (but you as the auctioneer take 1 bps).

2. Across Settlement is designed to handle and support any auction mechanism producing transactions or signed orders following the ERC-7683 structure (apart from the mentioned off-chain price RFQ for bridge transfers, it will be able to settle UniswapX cross-chain swaps).

Unichain will support ERC-7683 in order to enable cross-chain swapping seamlessly between chains

Across Settlement as the solver’s settlement network of choice for securing UniswapX cross-chain swaps

At its core, Across Settlement manages user capital escrow, intent fulfillment verification, and solver repayments. The value prop of an intent settlement network is offering different features to solvers that makes their life easier (such as lowering their costs) when filling user orders and competing in RFQ-based auctions as they have a) security guarantees they will get their funds back, b) and in a fast and capital efficient manner (fast rebalancing).

For example, if you are a solver that has a $40,000 inventory your goal should be $400,000 in volume per day (a turnover of 10x of your inventory), for which you will need a lot of rebalancing, and a guarantee that the settlement protocol will be secure and efficient enough to repay and rebalance you fast enough to keep filling user orders and not get into capital constraints. If you apply an avg fee slippage of 3.5bps to that $400,000 in volume per day with that $40,000 inventory that gets translated into an implied top line APR of 114%. Nevertheless, for that APR to be realized the main factor is an efficient settlement and rebalancing network that enables you to meet the 10x daily inventory turnover.

Across is an efficient settlement network for solvers as it offers many differentiated features that are crucial for them such as: a) flexible repayment chain: allowing the solver to get repaid on their chain of choice and not being limited to have the funds stuck on the user’s origin chain, b) proven security model that provides lower execution risks for solvers in the sense that they are comfortable with the fact that they will be repaid and rewarded for fulfilling user intents, c) intent backstopping, for the case that a solver doesn’t end up fulfilling the user’s intent, the settlement network can use its own balance sheet (Across working capital solution) to fulfill it. ERC-7683 solvers will send their orderflow to the Settlement Networks that allow them to offer the cheapest fees and fastest fills to users so that they can win the respective OFAs (Across RFQ Auction for bridge transfers and Uniswap Batch Auction for cross-chain swaps).

There are some netting opportunities that arise during Across repayment process (which it does through 1 hour batches):

For instance, when a solver chooses to be repaid on a chain where there are concurrent users deposits being escrowed. It’s essentially a “Coincidence of Wants” (CoWs) scenario, where the transaction can be cleared or netted eliminating the costs involved with the additional bridging that would be required to rebalance solver’s liquidity. Across currently doesn’t charge any fees for this but it could implement a reduced “settlement fee” for the right of clearing through the use of concurrent user deposits.

When CoWs opportunities are unavailable (no concurrent user deposits on the chosen repayment chain by the solver) within the settlement window, Across offers solvers immediate payment through its working capital pool. This option incurs a marginal "convenience" settlement LP fee, which is designed to be lower than the bridge fees ensuring that solvers maintain profitability (could be thought of as a fee share on their top line fee as a solver would only use Across LP for rebalancing as long as the fees charged do not entirely cut into their spread from solving the user order).

Alternatively, solvers can use Everclear, a post-execution collaborative solver market, to find potential netting opportunities with other solvers (Solver’s Coincidence of Wants) before resorting to the Across LP pool. Both approaches aim to provide solvers with flexibility in managing cross-chain positions while maintaining profitability.

To summarize, in terms of where we expect value to flow it will be dependent on different factors mostly along the idea of what costs are being saved (or features or services offered) to solvers upstream by a. the OFA and b. downstream by Settlement Networks and that can be partially kept as an auction fee or settlement fee, as long as competitors' fill cost is similar or slightly higher.

Expected Fee share evolution for visual purposes

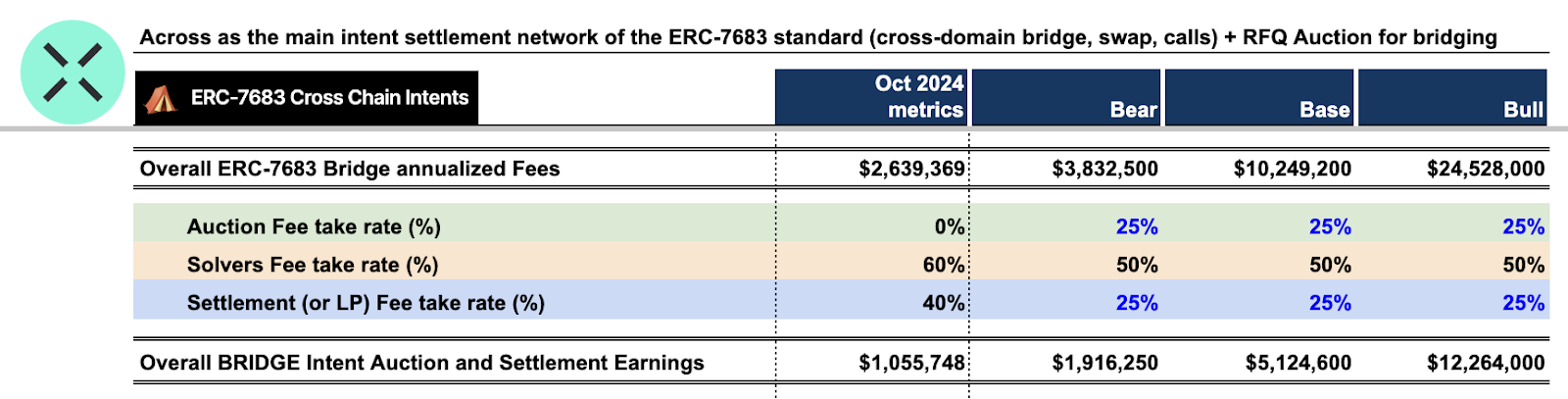

Going back to intent-based bridging Fees that we previously estimated across Bear, Base and Bull, we anticipate the Fee share among the different players to initially look like this (with the potential for further solver margin compression as it becomes more competitive).

Fee share for intent-based 7683 Bridging

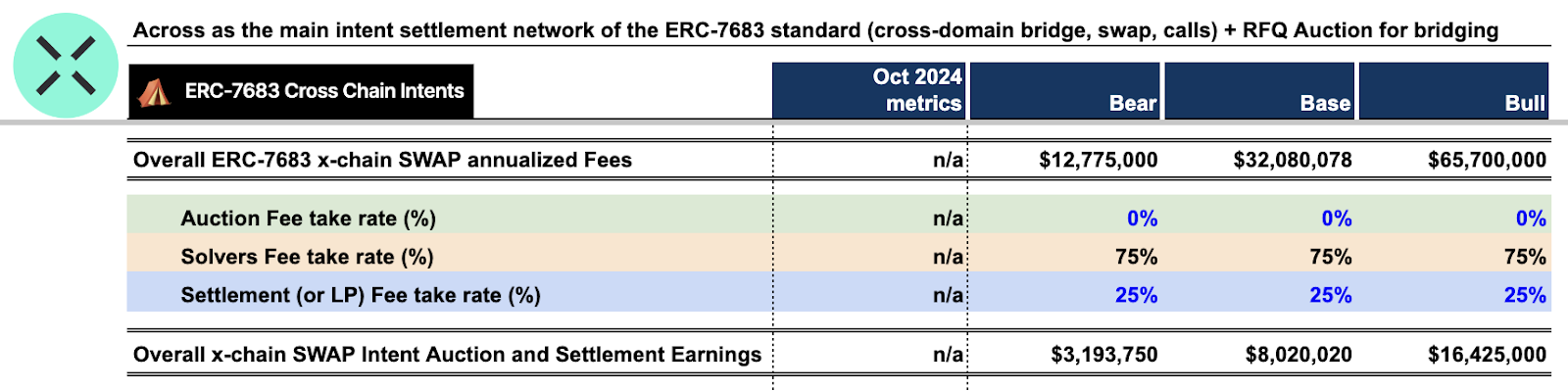

The main difference for intent-based cross-chain swaps Fees share is that even though we anticipate that in the long-run Uniswap will also probably charge an Auction Fee rate, that Fee won’t obviously be accruing to Across. So from Across POV valuation that should be considered to be 0%, while Settlement Fee share remains the same at 25%.

Fee share for intent-based 7683 x-chain Swap

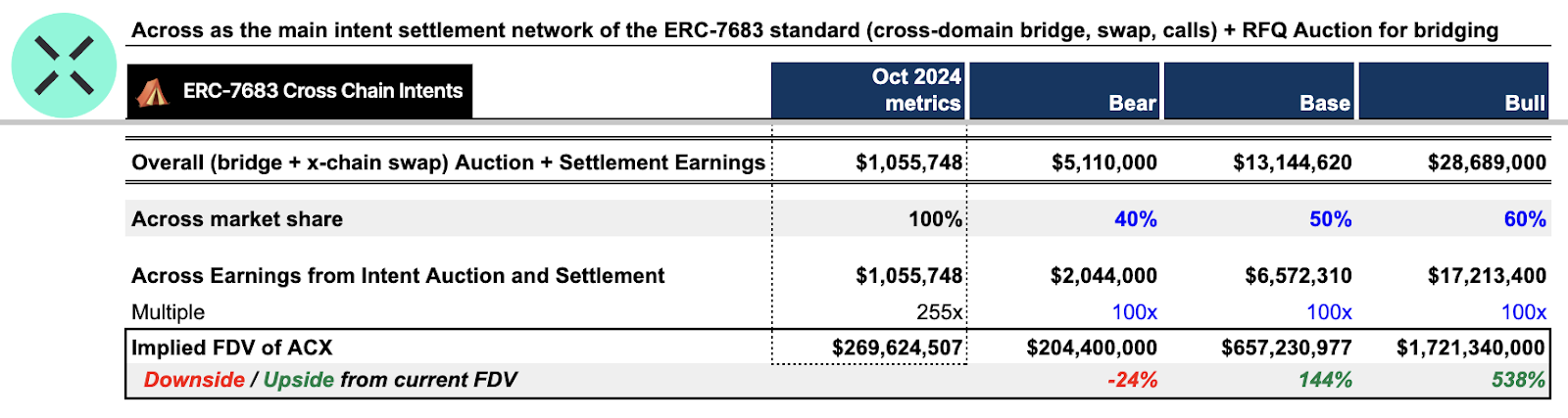

As a result, below are the implied Auction + Settlement Earnings scenarios across Bear, Base and Bull for protocols that are both OFAs, and Settlement Network in this ERC-7683 world. Lastly, we do estimate Across market share to be 40-60% and apply a 100x P/E multiple to the resulting earnings, getting and implied fully diluted valuation (FDV) ranging from $625M to $1.6B, in the base and bull case.

Resulting Across upstream Auction and downstream Settlement Earnings, Multiple and implied FDV

SUMMARY

As the DeFi landscape evolves, Across ($ACX) emerges as a pivotal player in the intent-based cross-chain ecosystem. Leveraging the upcoming ERC-7683 standard, Across is uniquely positioned to capture value at both ends of the intent fulfillment process: as an OFA provider for bridge transfers and as a Settlement Network for all ERC-7683 intents (including UniswapX cross-chain swaps). This dual positioning allows Across to benefit from the growing demand for seamless cross-chain interactions, which is expected to surge with increased L2 adoption and the proliferation of blockchain ecosystems.

Across's sophisticated settlement architecture, featuring efficient netting opportunities and a working capital solution, offers solvers unparalleled flexibility and capital efficiency. This, combined with its proven security model and intent backstopping capabilities, positions Across as the potential go-to settlement network for ERC-7683 solvers. With conservative projections indicating annual earnings potential between $6.2M and $16.3M, and an implied FDV ranging from $625M to $1.6B, in the base and bull case, Across represents a compelling investment opportunity in the rapidly evolving cross-chain DeFi landscape.

SIDENOTES

Cumulative and Historical MEV lost from on-chain gas foot races between solvers

Historical breakdown or fee share between rebalancing costs from Across LP working capital pool vs solvers fee margin

What’s ERC-7683 future when L2 native interop systems come to fruition? -> ERC-7683 intent standard aims to become this simple unifying layer, or “glue” across all the different native L2 interop systems.

We are seeing all of these different L2 ecosystems building their own ecosystem-specific interop: Op Superchain, Polygon CDK, Arbitrum Orbit, zkSync Elastic. But they are not compatible with one another. They are building this type of highway that allows for faster and more efficient messaging between Base and Op, for example for the Op Superchain interop. And while all of them strive for becoming very fast, as long as they take >1 minute for finality (which they will) there will still be a need and a market for intent-based interop powered by ERC-7683 (as it enables 3-5 seconds fills).

For example, if the origin and destination of a specific cross-chain intent are both within a native interop stack like the Op Superchain, the solvers would fill using ERC-7683 and instead of waiting for 1 hours of settlement (current Optimistic model that Across follows) they would just get paid back faster. This also improves UX as it would get cheaper for users (as loan times between a. solver fulfilling an intent, b. intent fulfillment being verified and solver getting repaid go from 1 hour to a couple of minutes). You would basically have Across’s solvers taking advantage of this better road connecting those L2 routes to get repaid faster vs the current 1 hour delay that they have to wait. You have OP Superchain-native interop under the hood being used as the method for proof verification and the UMA Optimistic way of sending messages that currently takes 1 hour can go away and exchange with this more cryptographically-secured and faster version.

ERC-7683 x AI play -> competitive agents for any on-chain task that you express on natural language?: A TG-based prompt where you express in natural language what you want to do on-chain and a LLM parses the intent and sends it to a solver (important here to have verifiability and safeguards). AI agents have the potential to greatly simplify and improve the crypto UX, particularly in the context of cross-chain interactions. Instead of manually navigating different chains and token types, users could simply tell their AI agent, "Swap $100 worth of ETH to USDC and send it to Alice'' and the agent would handle the technical details, ensuring that the most liquid and cheapest route is taken. Apart from simple interactions, they can additionally fulfill more complex operations, such as yield farming or LP rebalancing cross-chain, without the need for the user to actually go through click flows. Instead, users could give the agent natural language commands.

Axal -> v2 goal of creating a scalable and secure intent processor and OFA auction driver. Building off of work by Across and UniswapX with solvers for specific tasks, Axal aims to support more general tasks to be auctioned off to agents (beginning with arbitrary on-chain state detection, transfers, and smart contract calls, expanding to web2 actions). Axal’s primary differentiator is support for multi-step systems, not discrete actions.

https://x.com/ashlan_ahmed/status/1844403418343014566

What if there are other standards that are going to be pushed and launched by competitors (Socket, OneBalance may be working on their own standards)? I guess there is a possibility that new standards like 7683 emerge that decide to be more granular and “specific” to certain use cases, but the probability that ERC-7683 wins is higher than other possible alternatives as it's being pushed by main category leaders on each of their verticals (bridging for Across and swapping for Uniswap).

Won’t cross-chain swaps eliminate a great part of the need for bridges or same-asset transfers?, and thus by projecting them separately we may be overestimating the TAM by double-counting? Intuitively, one could say that the main reason why people bridge (I myself) is to buy a token that may be on a different chain than where I had funds originally. So I bridge + swap. There are other reasons (which would be calls or multistep TXs which are supported by Across+) like bridge + deposit into a protocol like Pendle to earn yield, + LP into a DEX, + deposit collateral to lending protocol to earn yield, buy a chain-specific NFT, airdrop farm a new L2 that is doing quests…, but I would say those are not the prominent use cases? I think this is one of the best push backs and for which I don’t have a very good response tbh. I lack data as to what users do after bridging to a L2.

Why will solvers on the Across off-chain RFQ Auction be okay with only charging 2.5 bps?

a) Because they are fine with lower rate of returns due to potentially having lower capital or opportunity costs than competitors. The main edge of solvers in Across off-chain price-based RFQ auction will be having access to cheap inventory on-chain (lower capital costs). This is what @intheanera, @nomial_iol, and others are working on.

b) Because, despite the fact that under the current model where their expected rate of return is generally 4 bps, they may be losing or surrender on average 2bps from overpaying in priority fees and tx reversion gas cost (thus net 2 bps, which is lower than what they could earn in the RFQ Auction by only charging 2.5 bps).

What about competitors on the settlement (or rebalancing) layer for Across like Everclear? -> If we walk through a case where two solvers could collaboratively settle on Everclear (because they are connected to more intent-auctions like DeBridge and have a larger surface area for CoWs possibilities), in a world where every bridge or cross-chain protocol follows ERC-7683 standard for its intent orders, those internal netting or clearing opportunities would already be covered by Across Settlement and thus entirely neglect the majority part of Everclear’s value prop. We expect the market structure to follow a power-law distribution, with a single Settlement Network taking a big share, which would leave competitors edgeless.

Couldn’t the solvers or MMs themselves do the inventory management and not need Across’ “working capital solution?. In other words, be sophisticated enough for them to have their own netting where they are doing fills from Arbitrum, then Base and getting paid back on Arbitrum while making fills on Base. But then the solver has other fills going the other direction and he just does his own netting. The TLDR is YES, but a follow up of this question is what’s the best breakdown of solvers that Across would want to see -> a) an oligopoly with few sophisticated actors solving 80%+ of the orderflow (kinda power-law distribution with the introduction of Wintermute), b) a more equally distributed and democratized market structure with a lot of solvers.

From a value accrual perspective it seems like Across Settlement Network would benefit more from a more distributed market structure where anyone can be a solver and can use Across working capital solution for rebalancing, and thus be charged the “settlement fee”.

From a UX perspective, there may be efficiency benefits from having few sophisticated solvers solving most of the orderflow. The larger and more diversified solver network and competition that you have, the better but up to a certain optimization point -> (check Tarun’s paper on solver’s oligopoly as the desired state: https://x.com/tarunchitra/status/1765394067439947995) + the fact that they have their own rebalancing mechanism enables them to not have to pay ACX settlement fees.

Having said that, it may not be in Across hands:

As the orderflow pie and network gets big enough it starts becoming interesting for sophisticated solvers (Wintermute) to enter as a solver, which should dilute opportunities for the rest of the solvers + with hundreds of chains on the horizon, it'll become complex to manage token inventories and infra while remaining profitable, again leading to sophistication and centralization.

•

•

•

Affiliate Disclosures

- The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- The author is not being compensated in any form by the target in relation to this research.

- To the best of the author’s knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

Neither BIDCLUB nor PHATPITCH LLC represents or endorses the accuracy or reliability of any advice, opinion, statement or other information displayed, uploaded, or distributed through BIDCLUB by any user, information provider, or other party. PHATPITCH LLC is not a broker, a dealer, or investment adviser. Nothing in BIDCLUB constitutes an offer or a solicitation to buy or sell any securities. BIDCLUB prohibits the sharing of material non-public information (MNPI), but assumes no responsibility for member conduct or associated risks. Nothing in BIDCLUB is intended as specific investment advice and no individual should make any investment decision based on any recommendation or analysis provided on BIDCLUB. You acknowledge that any reliance upon any such opinion, advice, statement, memorandum, or information shall be at your sole risk, and you bear sole responsibility for your own research and investment decisions. See full

Terms and Conditions.

Gm - thank you for the writeup. A couple Q's

- Why 100x PE? How else should one think about the benchmarking and relative val on when to take profit?

- Can you walk us thru the vesting schedule and its impact on float in the next 6 month?

- Do u have a sense of timing on when we should really start seeing the impact of the ERC7683 implementation?

- The above seems to be the crux of the thesis -- any other catalysts we should be aware of on the horizon?