Liquity

LQTY

Target Name

Liquity

Ticker

LQTY

Strategy

long

Position Type

token

Current Price (USD)

0.93

Circulating Market Cap ($M)

91

Fully Diluted Market Cap ($M)

93

CoinGecko

Upcoming Liquity V2 Launch: What It Means for $LQTY

09 Nov 2024, 08:35am

TL:DR:

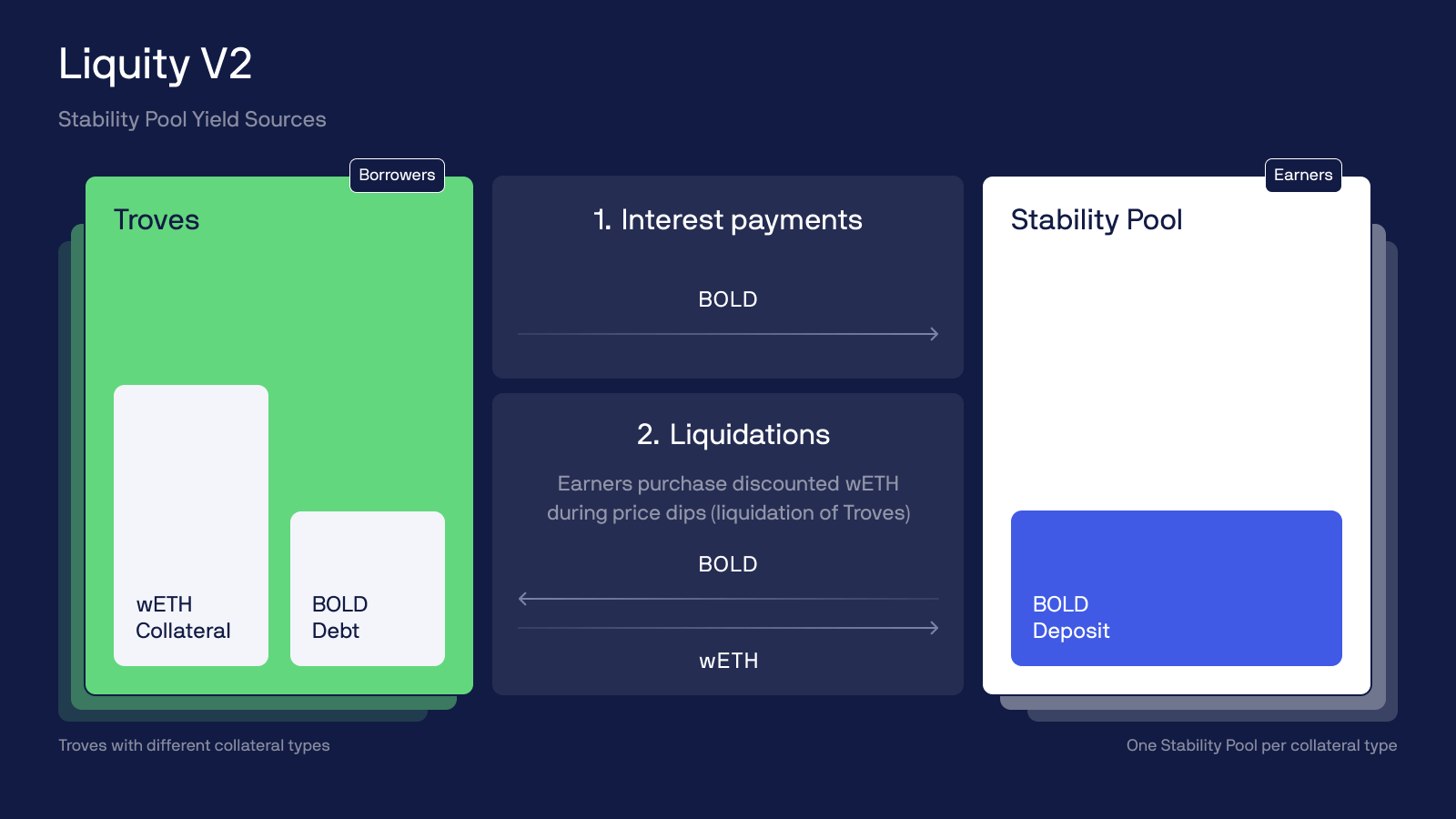

Liquity v2 is a CDP platform. Users can lock WETH and/or select liquid staking tokens (LSTs) and issue stablecoins (BOLD). Collateral choices: wETH, rETH, wstETH.

Liquity v2 introduces a new DeFi primitive where users set their own custom interest rates, instead of being rate-takers like in traditional lending protocols.

Liquity v1 has low fee capture due to its interest-free model. LQTY stakers only earn a 0.5% issuance fee from LUSD minters and liquidation fees. In v2, rates will be market-driven and are expected to align with other lending protocols, leading to greater value capture.

Liquity v1’s focus on governance minimization and protocol immutability limits LQTY’s utility. In v2, Protocol-Incentivized Liquidity (PIL) is introduced, similar to gauge voting, allowing 25% of borrowing fees to be directed to pools, lending markets, and other strategies. The longer LQTY is staked, the more voting power it accrues, creating the conditions for bribe market to form.

Friendly Forks of v2 is expected to airdrop to LQTY holders and/or share revenue with Liquity (Note: reasonable speculation but not confirmed. Link)

Recap of Liquity v1

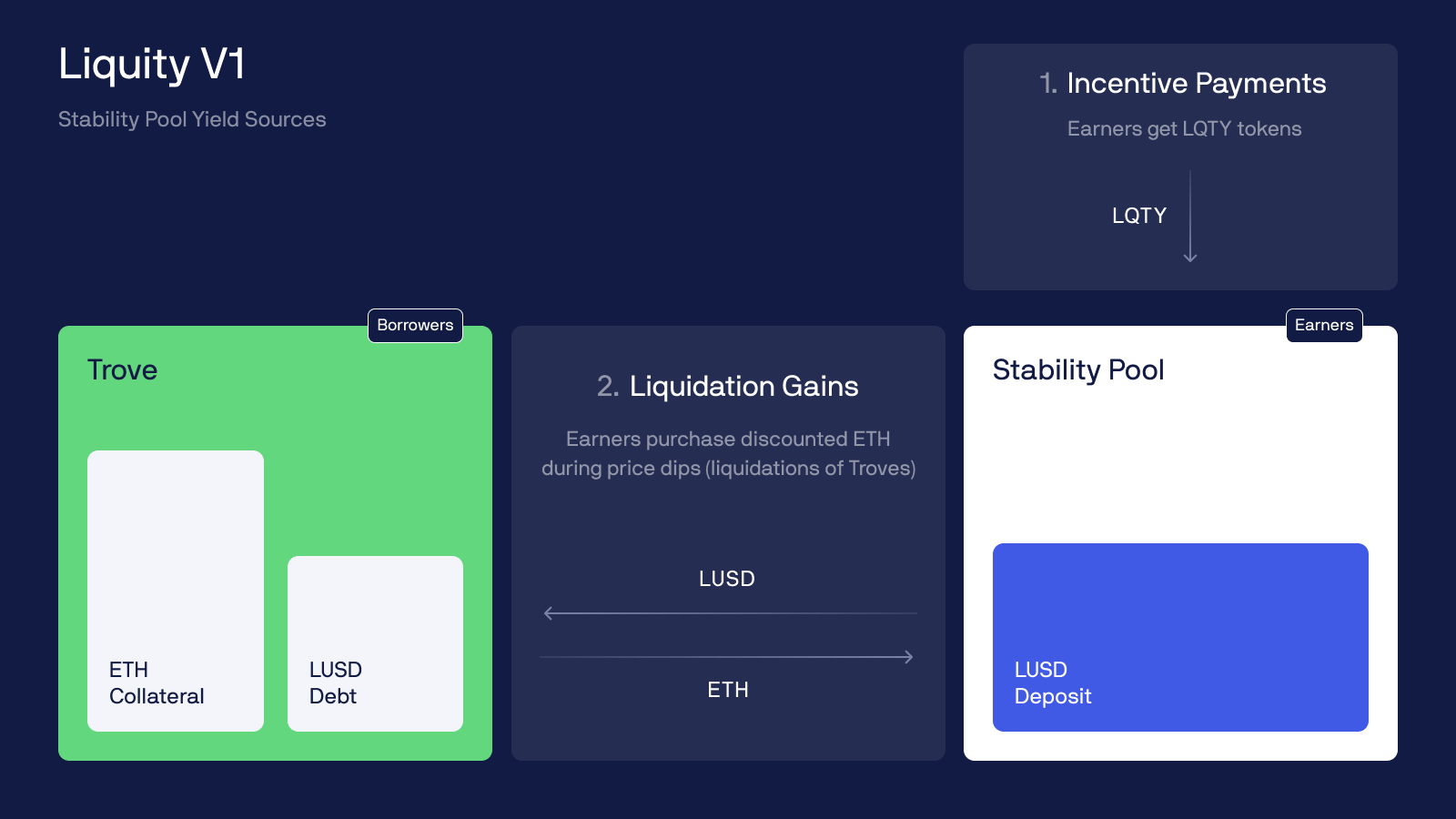

Liquity offers interest-free loans in LUSD, backed by ETH collateral. The protocol charges a 0.5% issuance fee to users, and loans can be liquidated if the collateral ratio falls below 110%.

Liquidations are supported by a stability pool funded with LUSD deposits. LUSD is pegged between $1 and $1.10 through arbitrage opportunities.

LQTY stakers earn ETH from issuance fees and LUSD from redemption fees when arbitrageurs swap LUSD to maintain the peg. The protocol is designed to be immutable and governance-free.

In v1, stability pool depositors put in LUSD to earn LQTY emissions (from inflation). LUSD in the stability pool is utilized in liquidations so depositors have the option to buy discounted ETH.

How does the user set interest rate work in v2?

On platforms like Aave, if you deposit $1,000 of ETH and borrow $500 of USDC (50% LTV), you pay the same borrowing rate as someone with a 80% LTV.

Liquity v2 introduces user-set interest rates: borrowers can choose their own rates, based on what they are willing to pay and their risk appetite regarding risk of liquidations.

Redemptions (anyone can get BOLD on the market and redeem for underlying ETH/LSTs) are aligned with dynamic interest rates. Instead of targeting loans with the lowest collateral ratio for redemption (like in v1), redemptions will occur in ascending order of individual interest rates.

Borrowers can set rates between 0.5% and 1,000%. Borrowers with lower rates are at higher risk of being redeemed. While they can freely adjust their rates, they must align them with the market to avoid redemption.

The redemption mechanism allows any holder to swap BOLD for $1 worth of collateral (e.g., ETH or LSTs), creating arbitrage opportunities when BOLD trades below peg (e.g., if BOLD is trading at $0.90, buy BOLD from the market and redeem it for $1 worth of collateral).

The collateral paid to the redeemer comes from the borrower with the lowest interest rate, in exchange for a proportional debt reduction. Borrowers affected by redemptions lose collateral exposure without necessarily incurring a financial loss at that moment. Therefore, they are incentivized to maintain competitive interest rates to minimize redemption risk.

Problem with Liquity v1 and why v2 solves it

In v1, the average collateral ratio is around 500% (LTV of 0.2), much higher than the minimum 110% (LTV of 0.909). This is primarily because of the redemption mechanism.

Redemptions aren’t the same as repaying debt. If you're a trove borrower, you have collateral at stake and debt taken out in the form of LUSD. Redemptions mean that ANY LUSD holder, even a random person without an active trove, can redeem it for the underlying collateral whenever they wish. This is important because it's core to maintaining the peg. The way redemptions work is by targeting the troves with the lowest collateral ratios.

Therefore, having a low collateral ratio means you're constantly at risk of being redeemed, and the demand for redemptions is an unknown factor outside of your control. While the borrower might not lose financially when redemptions happen, it makes it difficult to maintain a stable, controllable leveraged position on your ETH. This is why v1 has such high collateral ratio and what makes v1 not ideal as a lending vehicle compared to traditional lending protocols.

The v2 design directly addresses this issue. Users can set their own interest rates, and redemption will target those paying the lowest rates, instead of being based on collateral ratios as in v1.

This makes v2 a much better vehicle for leverage, bringing it closer to a lending market like AAVE. Users can be confident that as long as they pay a competitive market rate, they should be able to maintain their leveraged position.

$LQTY (the current picture)

Liquity is one of the most secure and well-designed protocols, having been forked by many and never experiencing smart contract issues since launch—testament to its high quality.

Liquity's ethos is governance minimization and immutability, which is commendable. However, this design means the LQTY token has few attractive features (not even governance) for buyers.

The only utility for holding LQTY (in v1) is staking it to earn the 0.5% fees and redemption.

Thesis for LQTY in light of upcoming v2 launch

Support for LSTs drastically expands the addressable TVL for Liquity v2.

LQTY remains the protocol token, with no new token launch.

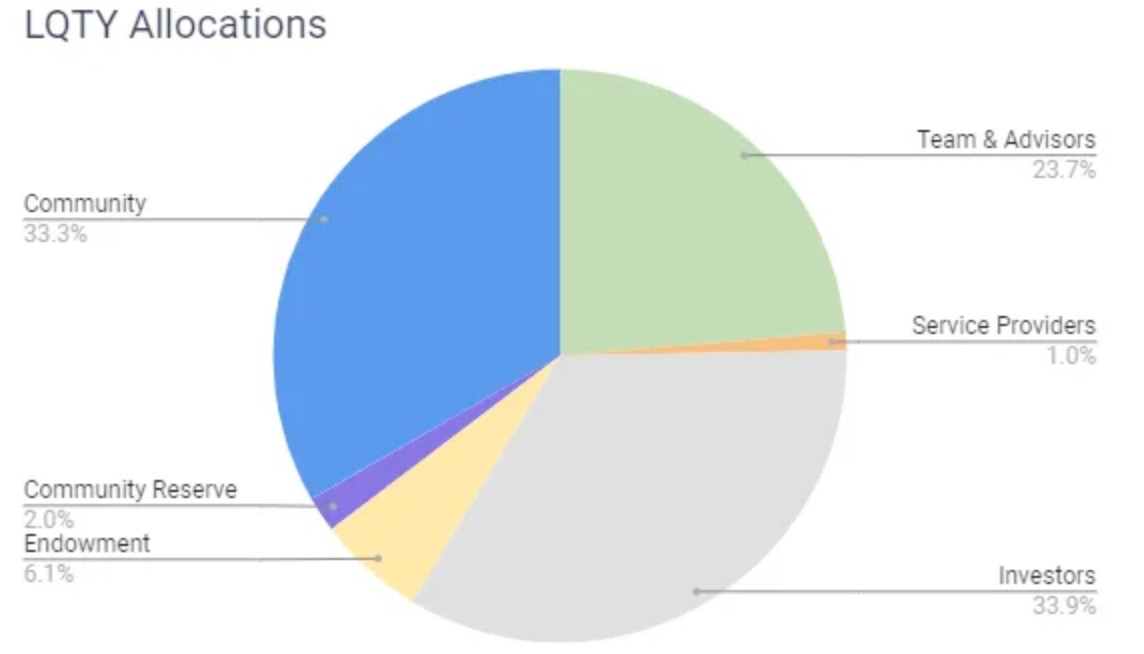

95% of LQTY is already circulating, no supply overhang.

v2 brings the protocol closer to the equivalent of a lending market and should be increasingly compared as so.

Liquity V2 is launching under a license but with “friendly forks” as partners across EVM chain in exchange for "incentives". 15 forks are lined up, examples include @beraborrow, @felixprotocol and @NeriteOrg.

Forks expected to airdrop to LQTY holders, revenue share with Liquity and use tokens to incentive BOLD pools across EVM chains. (link)

Risks

Still no direct value capture for $LQTY, as 75% of the fees collected reward the stability pool, and 25% go to PIL.

The stability pool remains a core component, limiting its broader distribution.

Bootstrapping liquidity for BOLD is tough, there’s no juice for protocol token farming given LQTY is 95% circ, organic yield may not enough to kick start the whole thing. (though mitigated by incentives from friendly forks)

Further Readings

https://liquity.gitbook.io/v2-whitepaper

https://x.com/lurkaroundfind/status/1796260757715169553

https://x.com/SamExotic3/status/1821345418237898831

https://x.com/filbef/status/1840875811077046734

https://x.com/zhao_eth/status/1839312864685007256

https://x.com/eldarcap/status/1838675605052649759

https://x.com/llamaonthebrink/status/1838947772537479213

https://www.liquity.org/blog/liquity-v2-bold-stability-pool-opportunities

•

•

•

Affiliate Disclosures

- The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- The author is not being compensated in any form by the target in relation to this research.

- To the best of the author’s knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

Neither BIDCLUB nor PHATPITCH LLC represents or endorses the accuracy or reliability of any advice, opinion, statement or other information displayed, uploaded, or distributed through BIDCLUB by any user, information provider, or other party. PHATPITCH LLC is not a broker, a dealer, or investment adviser. Nothing in BIDCLUB constitutes an offer or a solicitation to buy or sell any securities. BIDCLUB prohibits the sharing of material non-public information (MNPI), but assumes no responsibility for member conduct or associated risks. Nothing in BIDCLUB is intended as specific investment advice and no individual should make any investment decision based on any recommendation or analysis provided on BIDCLUB. You acknowledge that any reliance upon any such opinion, advice, statement, memorandum, or information shall be at your sole risk, and you bear sole responsibility for your own research and investment decisions. See full

Terms and Conditions.