deBridge

DBR

Target Name

deBridge

Ticker

DBR

Strategy

long

Position Type

token

Current Price (USD)

0.03

Circulating Market Cap ($M)

50

Fully Diluted Market Cap ($M)

280

CoinGecko

$DBR - The bridge people are happy to pay for

12 Dec 2024, 04:33pm

TLDR

deBridge is a message passing protocol (layer zero, wormhole) priced as a bridge (stargate, mayan)

Their bridge layer, the DeBridge Liquidity Network, is Across Protocol on steroids

Substantially undervalued on a per volume and per revenue basis vs competitors

Leads bridges in margins due to great UX. People are willing to pay for a better experience

Its speed and flexibility position it to be the leader of crosschain dapp integrations

They’re hyperliquid bulls and could become the canonical bridge for Hyperliquid

$DBR is used for managing a profitable treasury and will be used for staking

Price Target of $0.24

Protocol Overview

deBridge, despite its name, isn’t just a bridge. It’s a generic interoperable messaging protocol like Wormhole and LayerZero. There are a handful of applications built on top of this layer, most notably deBridge’s own Liquidity Network (DLN).

deBridge’s structure is similar to Wormhole and Layer Zero with executable on-chain smart contracts and a set of off-chain validators that will eventually be subject to staking, slashing and governance via $DBR.

The DLN is an intents layer similar to Across but more lightweight and expansive. Like Across, when it receives a bridge request, it hands off its flow to a market of relayers who compete to execute on its behalf, enabling efficient bridging.

However, unlike Across, its message passing layer enables it to settle relays individually and instantly instead of batched. This eliminates the need for a liquidity pool and reduces relayer risk, enabling native swaps and limit orders between any token on any chain within 5 seconds.

Additional “deApps” include a bridge for wrapping assets, dePort, a cross-chain NFT standard, deNFT, a cross-chain OTC desk, P2P, and hooks to enable integrations with protocols and market makers.

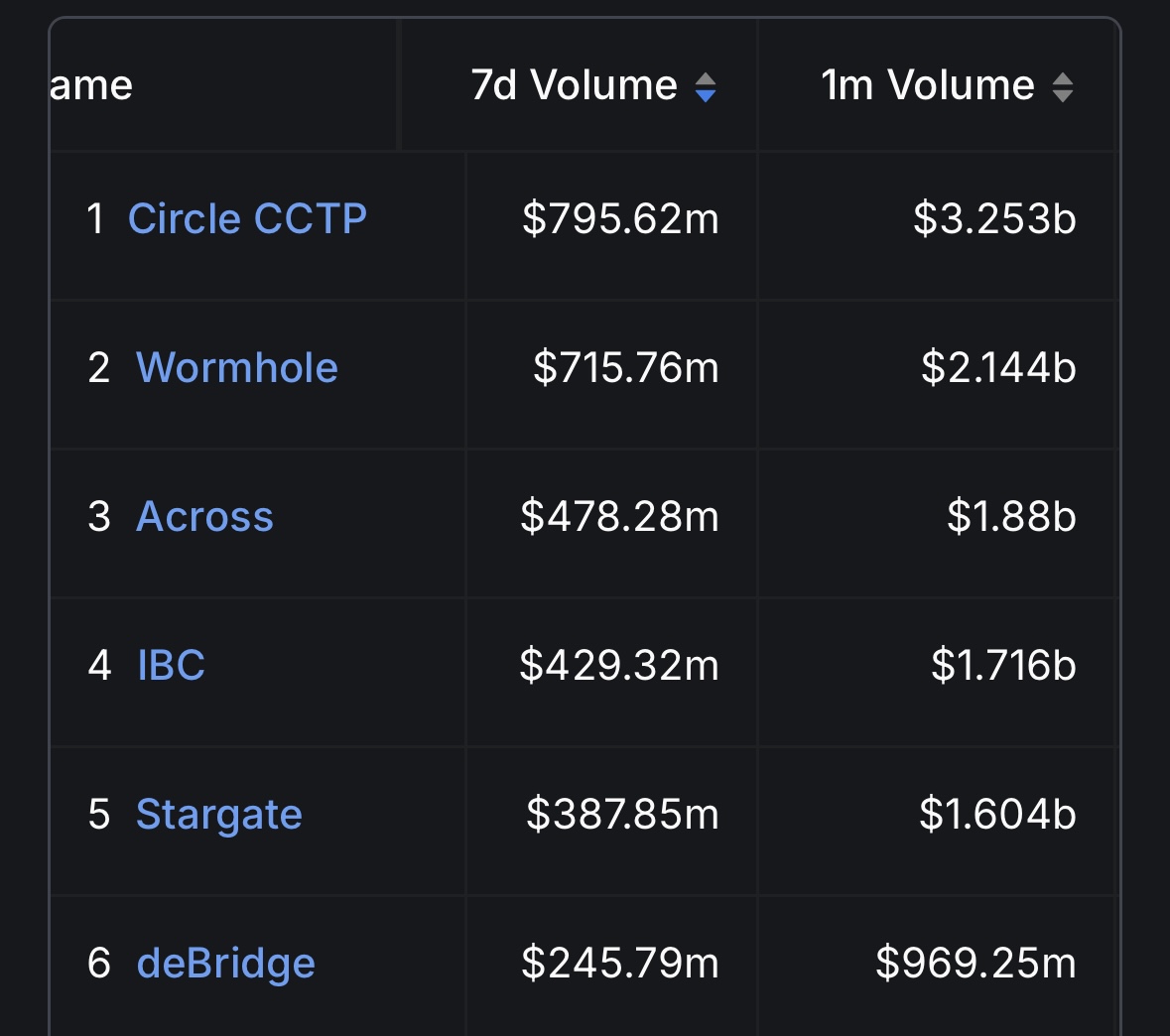

Traction

deBridge has roughly half the monthly volume as Across and LayerZero (Stargate), and a third the volume as Wormhole.

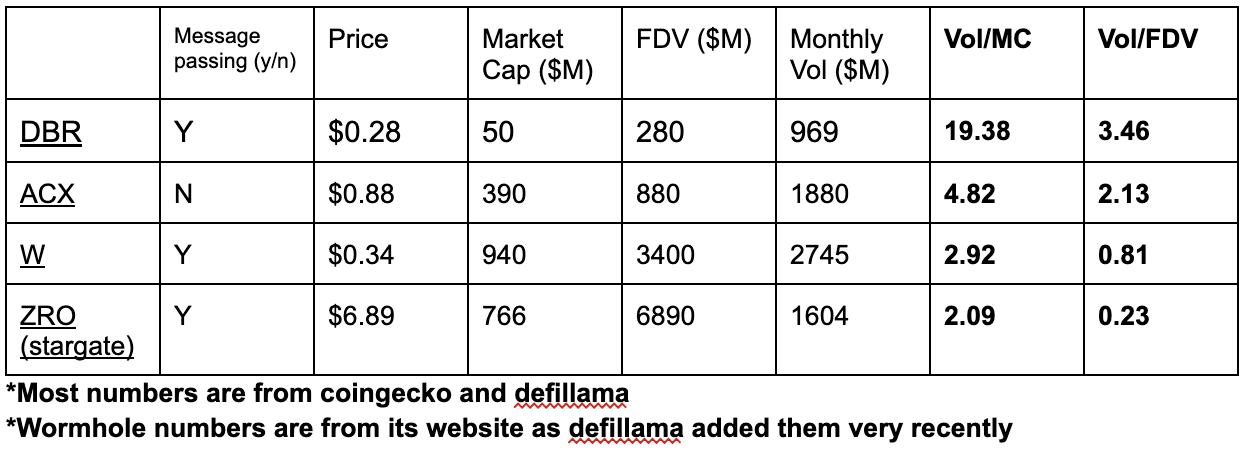

Compared to price, this far outperforms its counterparts. For the same valuation, deBridge sees significantly more volume versus Wormhole and Layer Zero. It’s even undervalued versus Across, which is a bridge without general message passing.

Furthermore, deBridge actually sees more volume in growing ecosystems. In the past month, it has had more volume to and from Arbitrum (Hyperliquid) and Base than Wormhole.

Best User Experience → Highest Margins

When I ask people what they think of deBridge, the answer is something like, “It’s expensive as hell, but I can’t stop using it.”

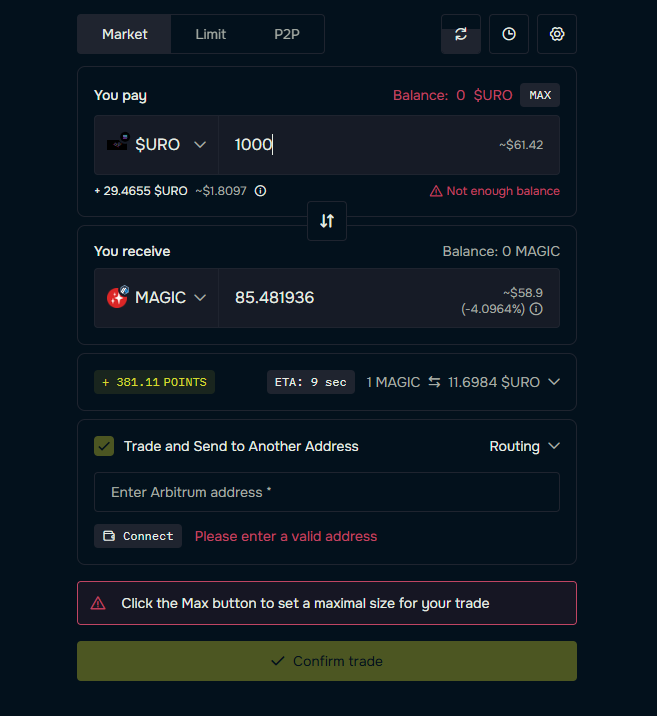

DeBridge is the definition of leaning into laziness. I have access to Circle, so I can literally bridge to dozens of chains for no fees. But I’m too lazy to swap to USDC, deposit to Circle, withdraw from Circle, then swap from USDC. I’d rather pay $2-5 on deBridge to go from $uro on Solana to $magic on Arbitrum with one click. In the blink of an eye, the $magic appears. It’s like Doordash on a Sunday hangover, but without the waiting.

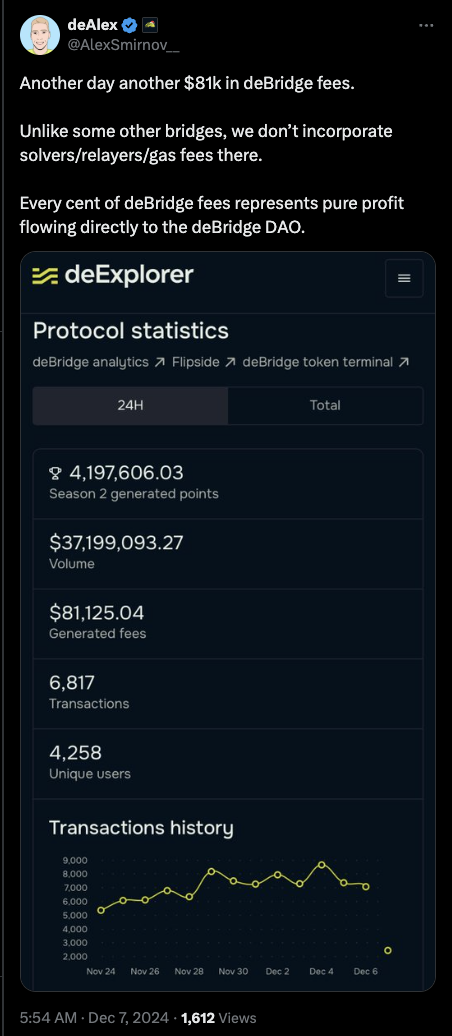

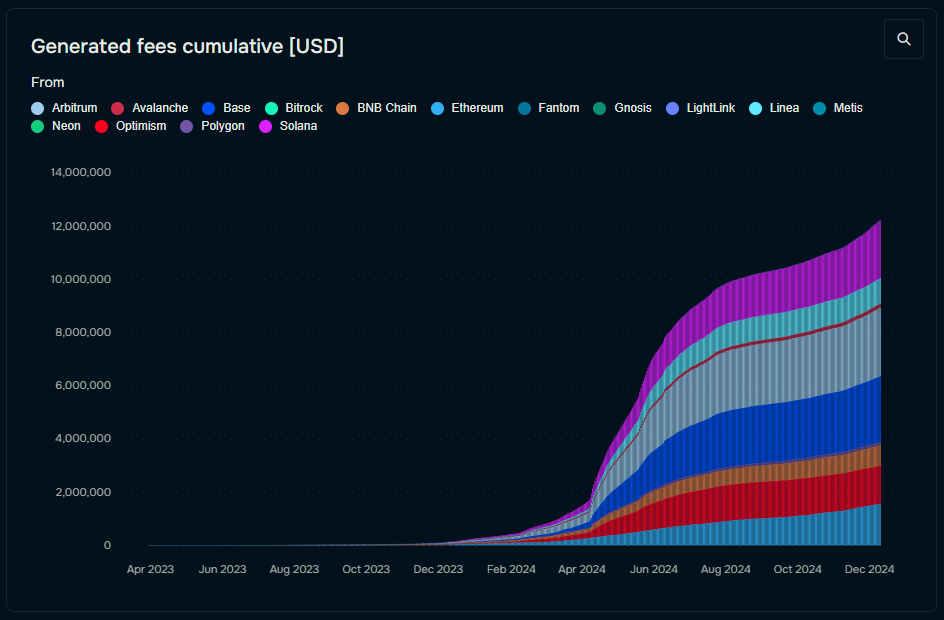

It turns out laziness is very profitable as it earns ~0.1% of its bridge volume as revenue, net of relayer/validator fees. Based on the past 30d, that’s $12m annualized, all of which goes to the DAO treasury.

In comparison, Across, Wormhole and Layer Zero appear to have no net revenue as all fees go to validators/relayers. I used to joke that bridges were like airlines—commoditized with terrible margins. deBridge, designed from the ground up with UX in mind, defies that.

Ecosystem Adoption

In the Solana ecosystem, deBridge has become a fan favorite for developers. Jupiter and Zeta Markets use it as their canonical bridge despite being partners with Wormhole.

Their team is also known to be hyperliquid bulls and they’ve hinted toward creating a bridge directly to HL.

Generally speaking, deBridge seems to be the best cross-VM solution for developers, especially between Solana and Ethereum L2s. Its instant crosschain swaps enable dapps to create seamless UX. As dapps like Phantom, Magic Eden and MakerDAO (Sky) add cross-VM compatibility, deBridge is likely to be integrated.

Token Utility

$DBR has two forms of utility: a network token with staking and slashing, and a governance token with treasury management.

As a network token, validators for the message passing protocol have to stake $DBR in order to get rewarded with fees (in ETH). Holders can delegate their tokens to share in the staking rewards. Malicious or faulty validators will be slashed. The network utilities have not been implemented yet.

As a governance token, holders elect the validators, choose to add new chains and determine the fees. They also manage the treasury, which currently holds over $13m, all from fees.

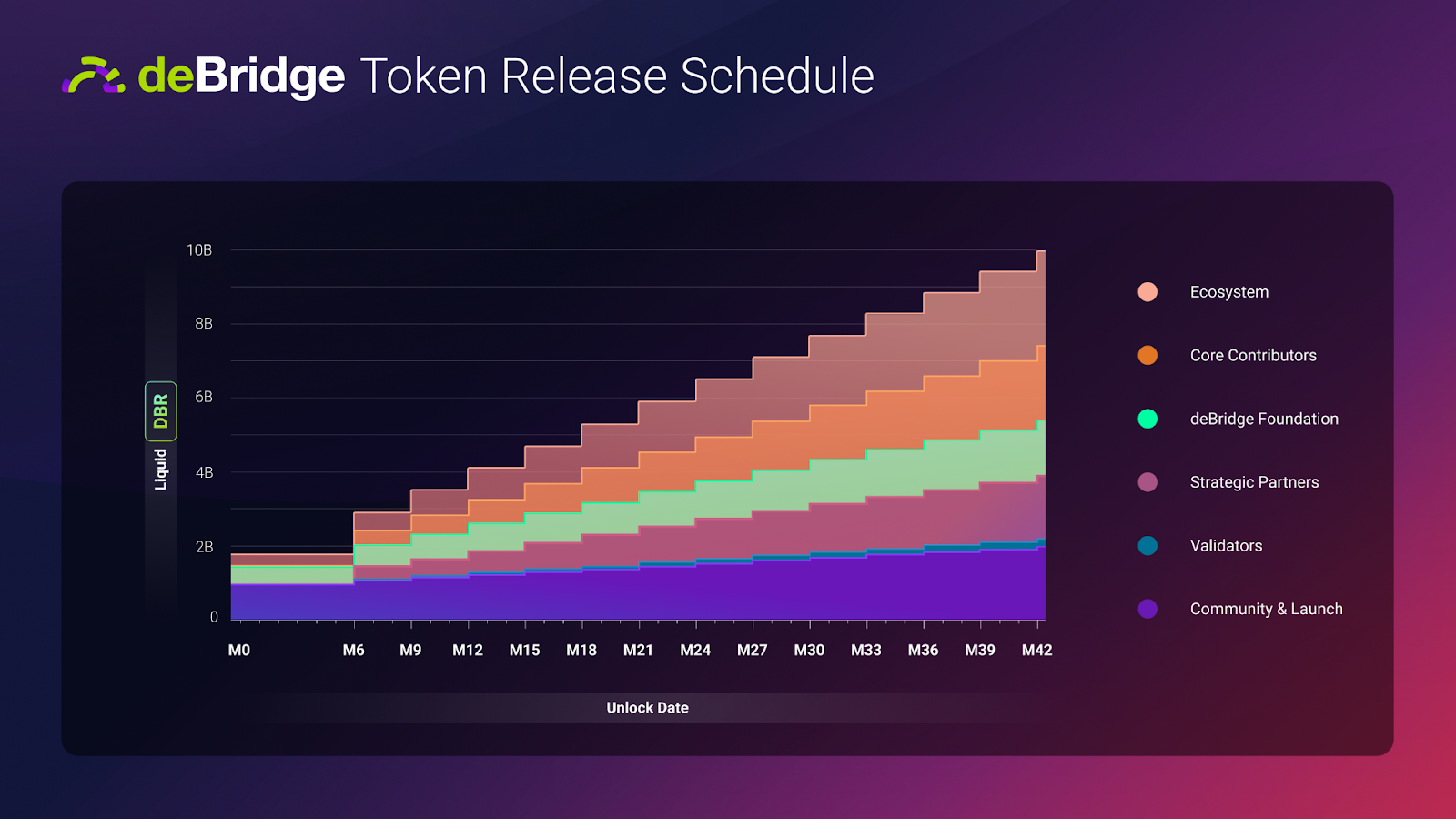

Tokenomics

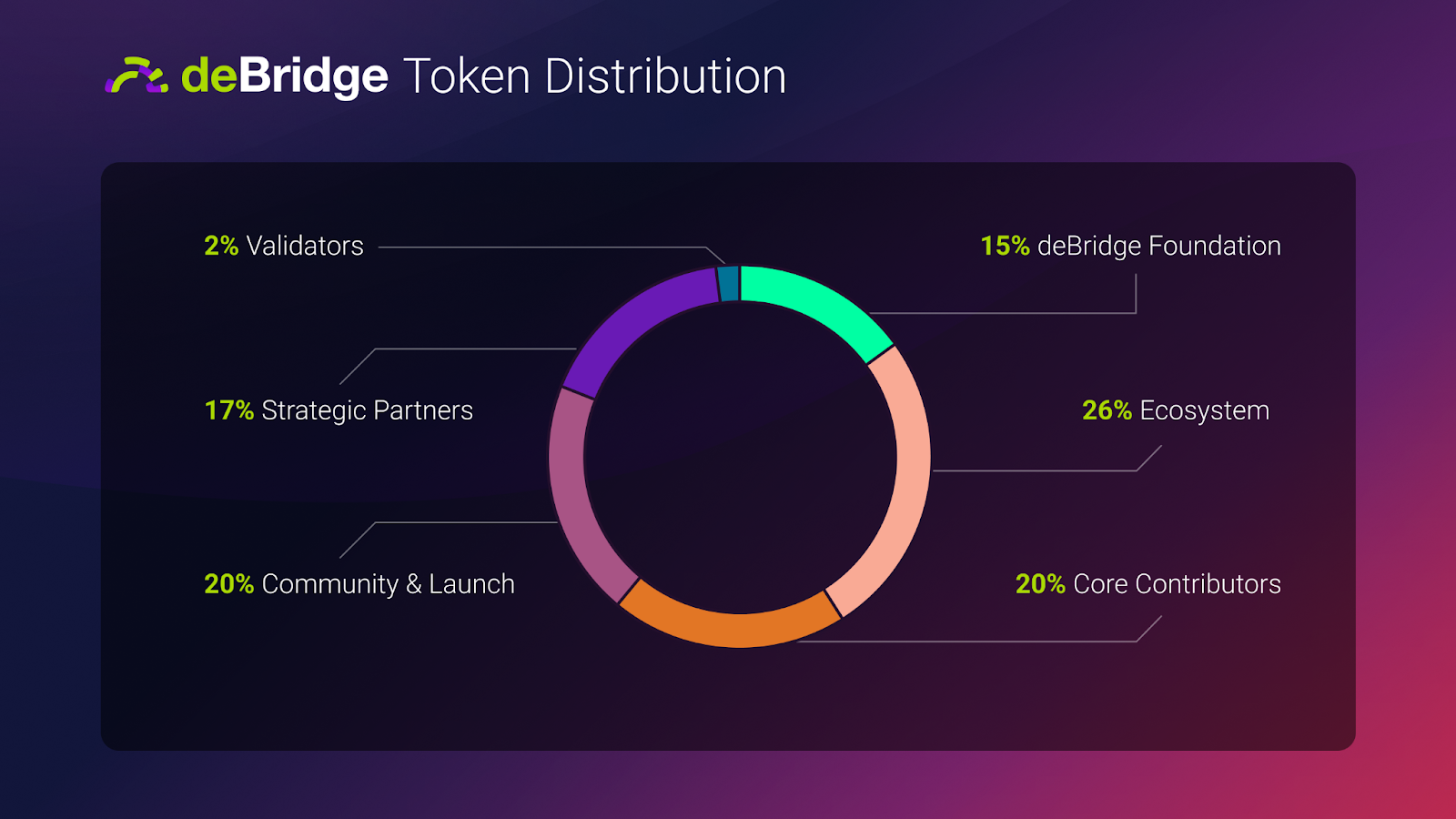

The token distribution is reasonable with 46% going to the community. Team gets 20%, VCs get 17%, grants via the foundation are allotted 15%, and validators get 2%. Of the 46% to the community, 26% sits in the treasury to be governed by the DAO.

The circulating supply is only 18% with unlocks beginning on April 17th. The looming unlocks may explain why the valuation seems suppressed. If so, that could lead to bullish unlocks in Q2.

Valuation

If we discount the 26% of supply in the treasury and 15% of supply for grants as unallotted assets, the total market cap of deBridge is $165M, with $13M in its treasury. With annualized earnings of $12M and staking utility, it seems severely undervalued, especially when compared to Wormhole and Layer Zero.

Based on the earnings alone, at a 20x multiple, $DBR’s total market cap should be $240M.

With network utility, the estimated annualized revenue for validators is $4.3M (181982 monthly trades x $4/trade x 50% share x 12 months). If we give this a 50x multiple due to the high premium on network tokens, that’s an additional $218M.

In total, that’s $240M + $218M + $13M BV = $471M at current metrics.

Considering the tailwinds of Hyperliquid, Base and cross-VM dapps, bridge volume, and deBridge’s dominance in it, will likely increase, growing its metrics by a potential 3x.

This gives me a target valuation of $1.4B in total market cap or $0.24 per token over the next year.

Catalysts

Across listed on Binance. $DBR is the only major interoperability token left to list

The manlets seem quite interested in using hyperliquid, but the onboarding process is tough for them. DeBridge becoming that onboarding tool has a lot of potential

Dapps going multi-vm between Solana and Eth L2s

Risks

It’s incentivized by points, so there is a risk of inflated metrics. That being said, it has the same volume per transaction as other non-incentivized bridges, and more than half of the season 1 airdrop remains unclaimed

Low float with upcoming unlocks

Wormhole announced at Breakpoint that they’ll be launching an intents based MPC network

•

•

•

Affiliate Disclosures

- The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- The author is not being compensated in any form by the target in relation to this research.

- To the best of the author’s knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

Neither BIDCLUB nor PHATPITCH LLC represents or endorses the accuracy or reliability of any advice, opinion, statement or other information displayed, uploaded, or distributed through BIDCLUB by any user, information provider, or other party. PHATPITCH LLC is not a broker, a dealer, or investment adviser. Nothing in BIDCLUB constitutes an offer or a solicitation to buy or sell any securities. BIDCLUB prohibits the sharing of material non-public information (MNPI), but assumes no responsibility for member conduct or associated risks. Nothing in BIDCLUB is intended as specific investment advice and no individual should make any investment decision based on any recommendation or analysis provided on BIDCLUB. You acknowledge that any reliance upon any such opinion, advice, statement, memorandum, or information shall be at your sole risk, and you bear sole responsibility for your own research and investment decisions. See full

Terms and Conditions.

Agree, Binance listing may be on the table in the following months. Looking back in history:

I think they applied for the listing program for high-quality teams and projects that Binance launched back in May 20, 2024, previous to $DBR TGE, when people were complaining a lot about the low float, high fdv meta. https://www.binance.com/en/support/announcement/calling-for-project-applicants-95b023902fef42e6a630425170460656

They also got highlighted by the Binance Research account 4 days later (May 24, 2024) on a twitter thread -where Across was also mentioned-. https://x.com/BinanceResearch/status/1794049995903254585