Euler Finance

EUL

Target Name

Euler Finance

Ticker

EUL

Strategy

long

Position Type

token

Current Price (USD)

7.35

Circulating Market Cap ($M)

135

Fully Diluted Market Cap ($M)

200

CoinGecko

Euler V2: 46% TVL Surge in 1 Month, $1.2B and Counting – The Modular Lending Powerhouse Poised for DeFi Dominance

20 Apr 2025, 02:25pm

Euler

TL,DR;

These guys have chewed glass and come out the other side stronger than ever. Most still remember Euler as the protocol that got hacked for $200M and folded, with TVL to zero. Only, that wasn’t a fold – that was the team returning capital so that they could do a ground-up redesign of the protocol from scratch to build out what is the most flexible and dev-friendly lending infrastructure in the market.

Type: Investment

Hold: 1 year+

Background

First live in 2022, Euler v1 was the team’s initial attempt at building out a more forward-looking lending protocol, enabling markets for the long tail of assets. All that was required was that there existed a WETH-pair on Uni v3 to enable a TWAP oracle price feed. Just prior to FTX collapsing, v1 had attracted almost $700M in TVL. Post-FTX, after dropping to $290M, the protocol recovered to $560M. In March 2023, the protocol suffered a massive flash loan exploit and was drained for $197M. Ultimately the hacker returned $195M of that, but the damage was done and TVL went to 0.

Story: https://www.euler.finance/blog/war-peace-behind-the-scenes-of-eulers-240m-exploit-recovery

Macro Dynamics

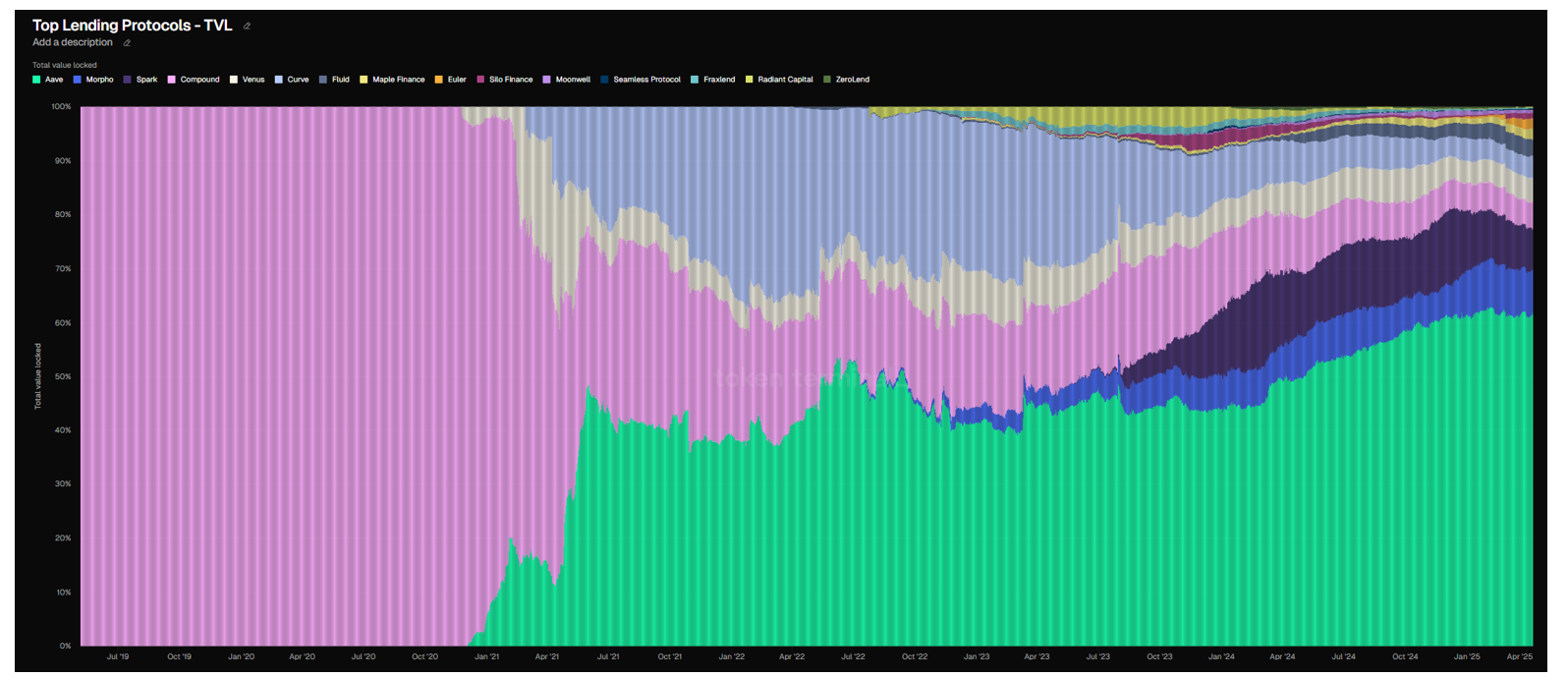

Monolothic peer-to-pool lending protocols have dominated DeFi lending. There is ~$40B deposited in the top 5 protocols, only $4B of which is in a modular-first lending protocol (Morpho). Monolothic platforms like Aave generally allow users to deposit governance-approved collateral into pools, against which they can withdraw a predefined amount (governance-given LTV) and predefined rate curves. This has proven incredibly effective given how straight forward the design is and the structure’s ability to scale, as evidenced by Aave’s dominance.

Where monolithic protocols are restricted is in fully permissionless deployment (e.g. are heavily governance-first), typically constricted to a smaller set of assets, and are fairly capital inefficient. Strictly isolated markets that constrain risk to a single pool are more flexible in asset selection and can cater to a longer tail of assets but are often highly capital inefficient as a deposit in e.g. a SHIB pool cannot be used as collateral in a WETH – e.g. no rehypothecation.

As the number of tokens continues to skyrocket, there is increasing demand for a “lending v3” (e.g. modular) that enables a far more flexible structure that can support both blue chips and long-tail assets, but at the same time allow for rehypothecation and capital efficiency, while maintaining a reduced risk profile as is the case with isolated markets.

Early attempts, namely oracle-less protocols such as Ajna, Astaria, Ethereum Guild have attempted to implement fully modular models, but have had limited success. NFT-first lending protocols such as Blend have implemented this model to a certain degree of success.

Morpho was really the first fully-modular protocol that caught on, having first launched as a more capital efficient overlay on top of Aave and Compound before launching its own lending primitive as a direct competitor. Solana’s top lending protocol Kamino is another example of a modular-first architecture with permissionless market deployment and a vault layer that aggregates liquidity across markets. The success of both of these underscores the market demand for modular lending.

Euler’s permissionless and modular architecture could dominate in a bullish, developer-driven environment with a surge of innovative financial products. With the expected regulatory clarity coming (esp. market structure bill) and resolution of the global trade conflict, DeFi generally is poised for explosive growth over the next few years. Euler is extraordinarily well positioned to be the fastest horse in that race. It is a blip on the TVL map right now, but the trajectory of that growth in one of the only true-PMF verticals in crypto cannot be underestimated.

Aave v4 is the elephant in the room for any lending protocols. Aave v4 is shifting away from its more monolithic, governance-heavy design towards a new unified liquidity layer, dynamic interest rate mechanisms, and modular risk controls. In essence, Aave is internalizing many of the functions that external platforms (such as the original Morpho overlay) addressed. This brings its implementation in much more direct competition to Morpho. Where it stops short though is addressing the long-tail of alt markets and rehypothecation ability that Euler offers. As such Euler’s value prop remains differentiated, while Morpho will likely begin to get squeezed from both sides (Aave from one, Euler from the other).

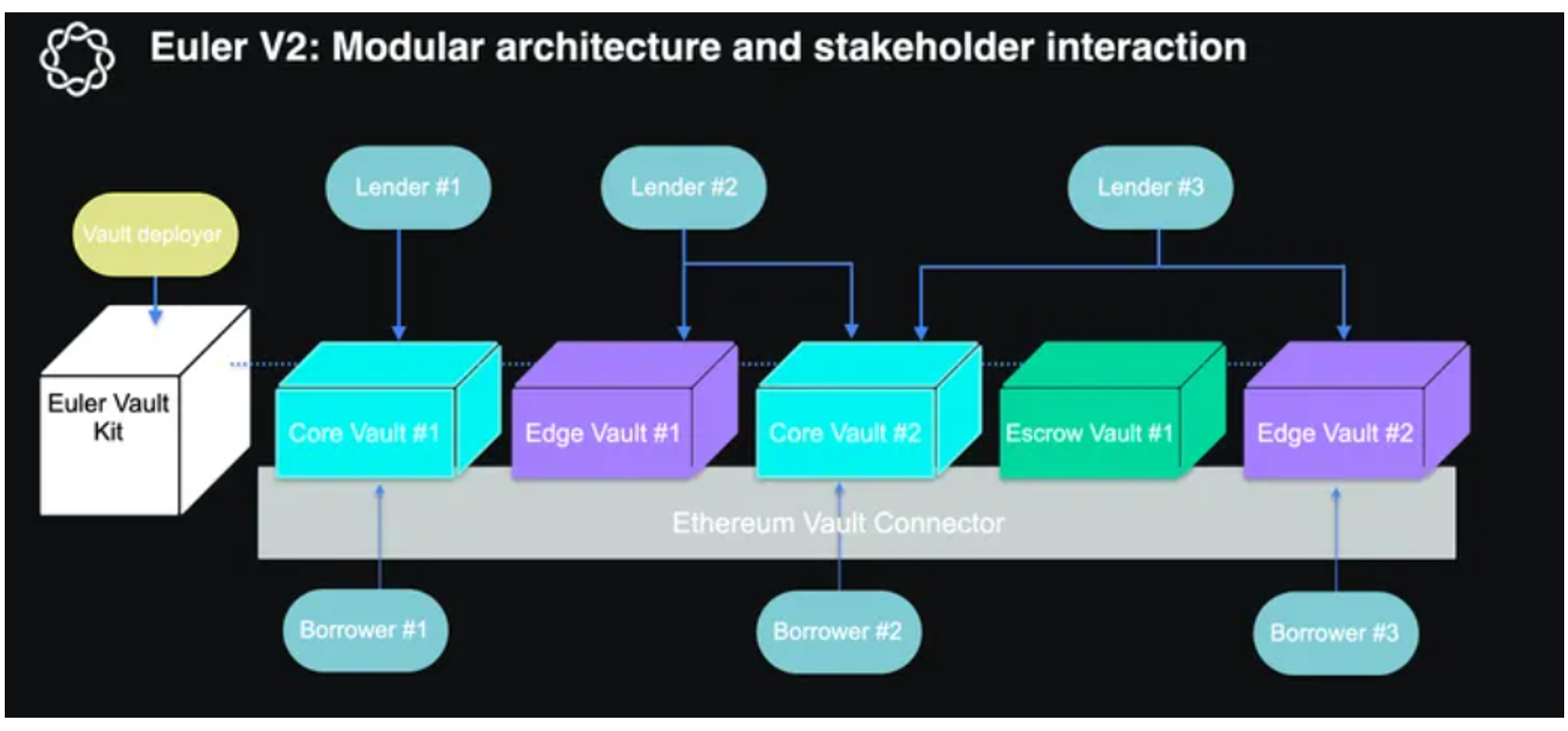

Euler V2

Live since late 2024, Euler v2 is a modular and highly customizable design geared towards onchain lending. V2 is based on two core components that together enable a wide array of lending products to be built: Euler Vault Kit (EVK) and the Ethereum Vault Connector (EVC). The goal of Euler is to improve upon the experience offered by current leaders such as Aave and Morpho by enabling a totally permissionless and ‘less paternalistic’ suite of products to developers. Euler’s main focuses are on flexibility and capital efficiency via simple rehypothecation. Beyond standard lending, Euler also enables simple yield/looping strategies through its vaults. Liquidations are done via Dutch Auction and Euler provides soft liquidations to minimize impact of rapid price movements, providing a far smoother and gas-friendly mechanism than most traditional lending protocols (e.g. fixed discount rates).

The majority of TVL is on Ethereum (~75%), but rapid reaction to the market and deployments on Base, Sonic, BOB, Bera, Swell and Avalanche (already $100M+) put them in contention to be the top lending protocol for any active EVM chain. Euler will also be live on Converge (ENA/Securitize joint chain) as one of the first to launch. Euler announced an expansion to Optimism on April 14 and BNB Chain on April 15. Documentation indicates we should expect more deployments to come:

Roadmap items include continued UX development (simpler deployment, portfolio tracking, etc.) and a native EulerSwap platform. The end state for Euler is a one-stop lending Super app built on top of its modular architecture.

- Ethereum Vault Kit (EVK):

o Responsible for authorization (e.g. user has requisite amount)

o System for building credit vaults, ERC-4626 based vaults that also enable borrow functionality. Different from traditional ERC-4626 vaults in that Euler’s credit vaults act as passive lending pools, rather than the standard yield-generating implementations that invest depositing funds

o Users can borrow from any credit vault as long as they have adequate collateral in any other vaults

o The vault that is borrowed from (the liability vault) decides which other credit vaults are acceptable as collateral

o Vaults hold a single ERC 20 asset

- Ethereum Vault Connector (EVC):

o Responsible for authentication (e.g. request came from a user)

o Integrating infrastructure that monitors which vaults are used as collateral by each account and enables liability vaults to withdraw collateral on users’ behalf in the case of liquidations

o Enhances the EVK by providing batching, simulations, gasless transactions and flash liquidity

o Enables the use of external contracts w/o requiring adaptors

o Provides a single address with 256 subaccounts, each of which can be used against a single asset

Revenue Capture to EUL

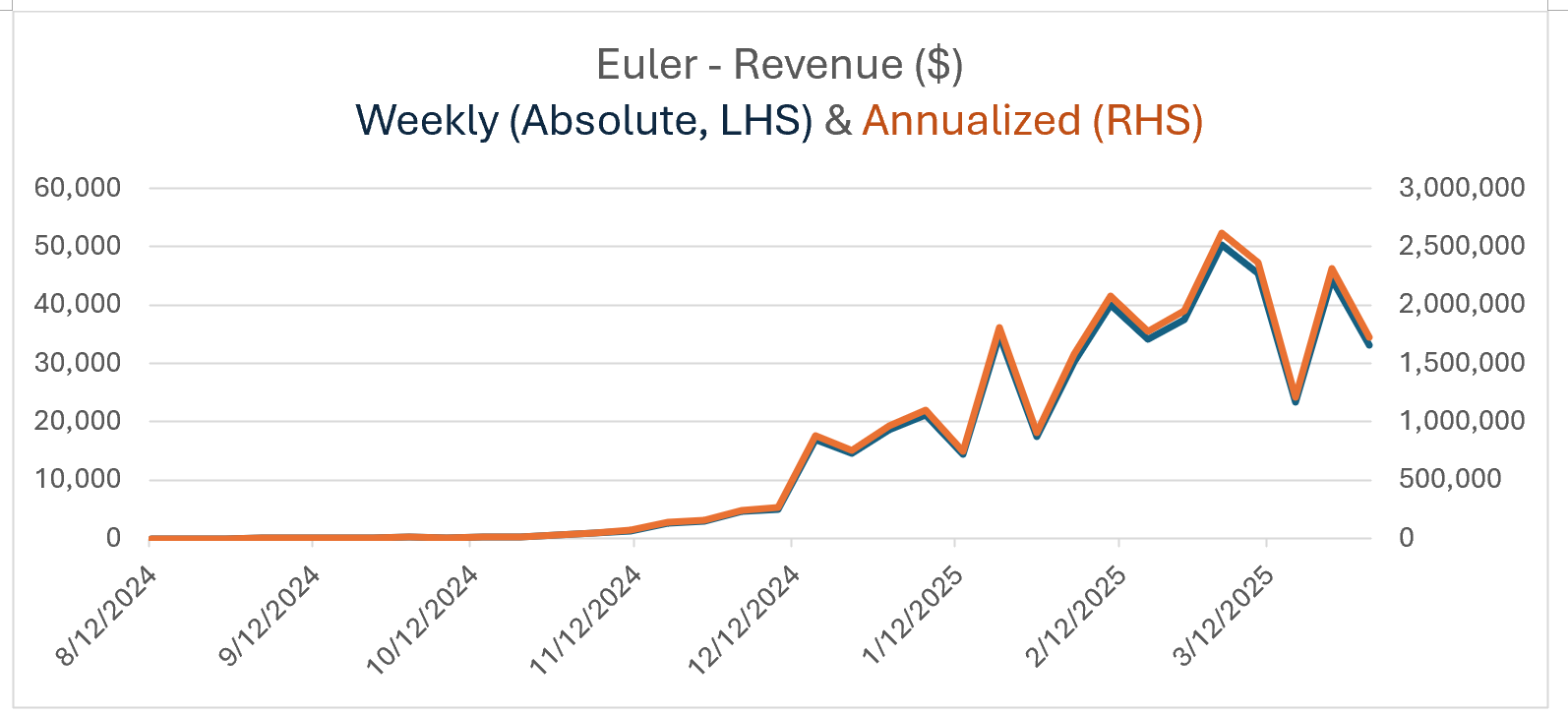

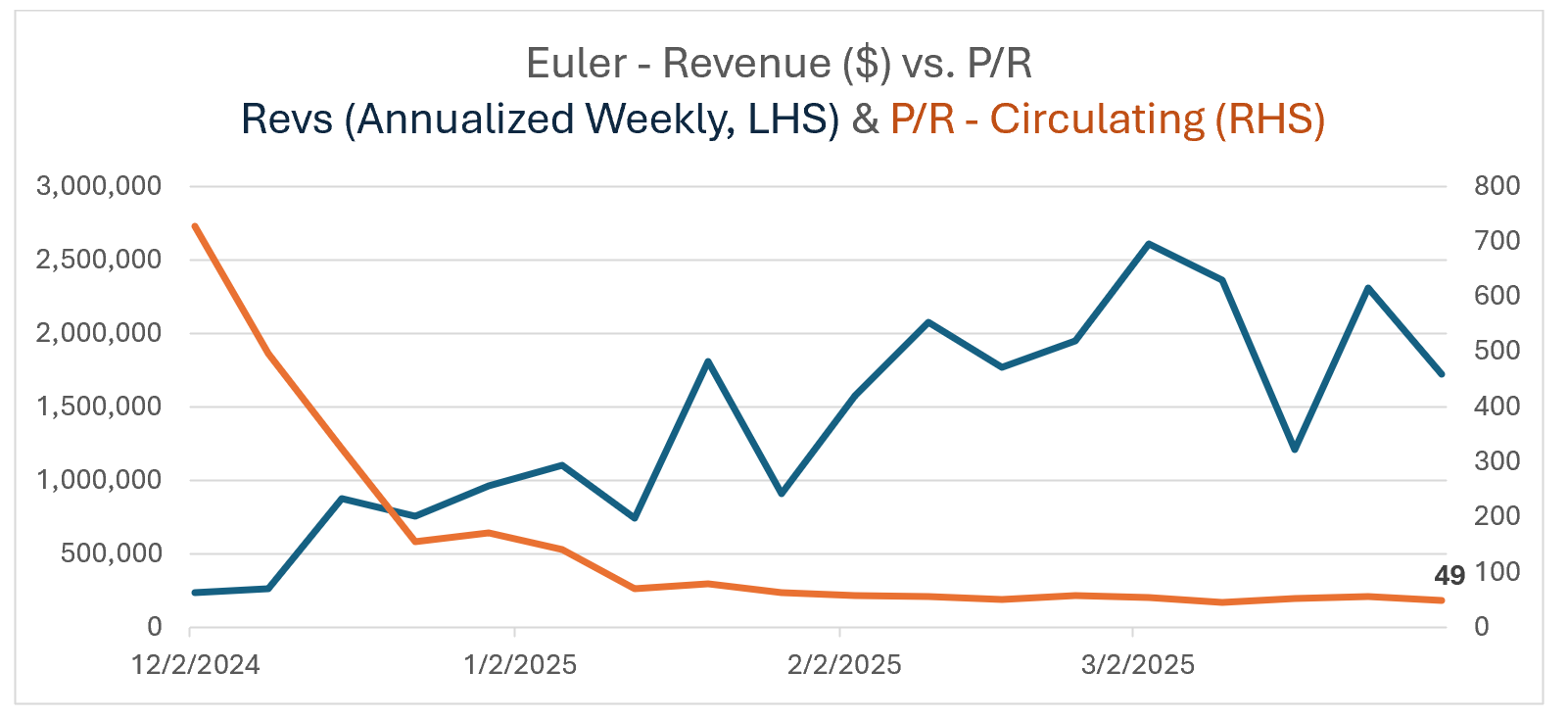

Euler uses a standard lending model where fees are generated on loans and liquidations. Fees are technically denominated in vault shares, charged by creating the amount of shares necessary to dilute depositors by the equivalent interest fee, and these shares are ultimately redeemable for the underlying asset. Because they enable support for the longtail of alt assets, they naturally capture fees in a variety of tokens. These captured tokens are then monetized through an in-protocol reverse Dutch auction for the fee flow. At current, Euler captures 10% of fees as revenue, on base vaults (vault creators receive the remainder). For managed vaults, risk managers receive 100% of fees generated. Recent market weakness has naturally led to a slowdown in rev growth with rate compression.

How this works: periodically, auctions are run beginning with a high initial price for those captured fee tokens. The price decreases over time until a bidder accepts and purchases that basket of tokens, paid in EUL. These EUL tokens are then diverted into the protocol treasury, where EUL holders have governance rights over the assets. For the moment, they are held in treasury and used to fund development where necessary. Future value share (yield payouts, burning, etc.) is dependent on governance action.

It is trading at the cheapest it has ever traded despite incredible growth and highly derisking execution/PMF from 4 months ago.

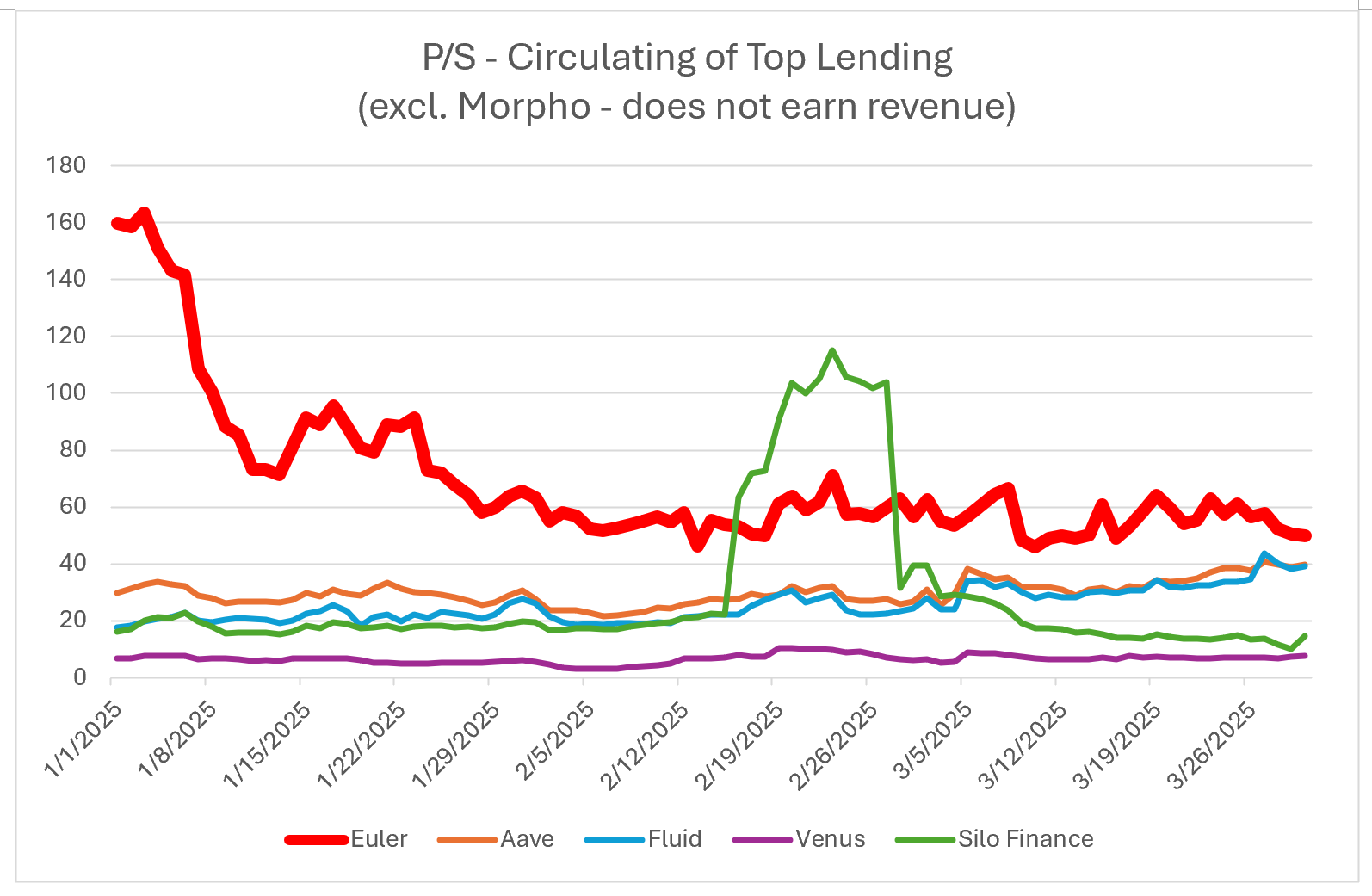

Relative to comps on the market, a lot of growth is still priced in, and admittedly the valuation remains rich at ~50x. But note that given revs are denominated in ETH and other tokens, these levels have largely been impacted by the softness in those prices.

Governance and Safety

Michael Bentley – Co-Founder and CEO. This guy is an animal, full stop.

- Before Euler:

o Postdoc researcher, Oxford (2019-2020) – dynamical systems (ODEs and PDEs) and evolutionary game theory

o Postdoc research, UCL (2017-2019) – evolutionary theory, bioinformatics and machine learning

o Postdoc research, University of Leeds (2016-2017), cancer evolution, bioinformatics and machine learning

o Analyst, Royal Bank of Scotland (2008-2009)

- Education:

o BS, Biology, Newcastle University (2005-2008)

o MSc, Computational Biology, University of Leeds (2009-2010)

o PhD, Mathematical Biology, Oxford, (2011-2016)

Bordering on religious zealotry, the focus on security is some of the highest in the industry. There is a live $7.5M bug bounty program via Cantina and more than 40 audits by the top firms in the space (full list here). This is important to highlight given their more hands-off approach to permissionless market creation and past issues with exploits.

The DAO oversees the direction of the protocol, but by all measures this is Euler Labs driven. The most recent proposal was in April 2025 to fund the Labs team $7.7M USDC for a 1-year contract. Notably, this is down from the previous contract value of $11.8M (of which Labs only billed $9.6M due to efficiencies and lower-than-expected bounty payouts and audit costs).

Currently have a ~$30M treasury – largely in own tokens; net treasury generally consists of ~$350K USDC and ETH. Treasury is viewable here: https://etherscan.io/address/0xcad001c30e96765ac90307669d578219d4fb1dce.

Based on most recent Labs contract value, the protocol has nearly 4 years of runway at current levels. Obviously would like to see more of this in stables or non-EUL, but still a strong amount relative to the size of the project.

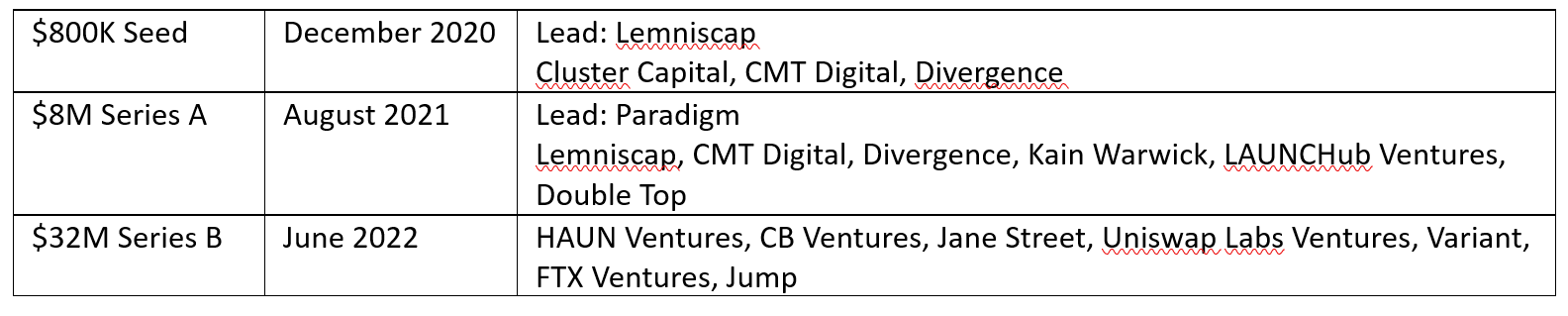

Private Investors

Performance

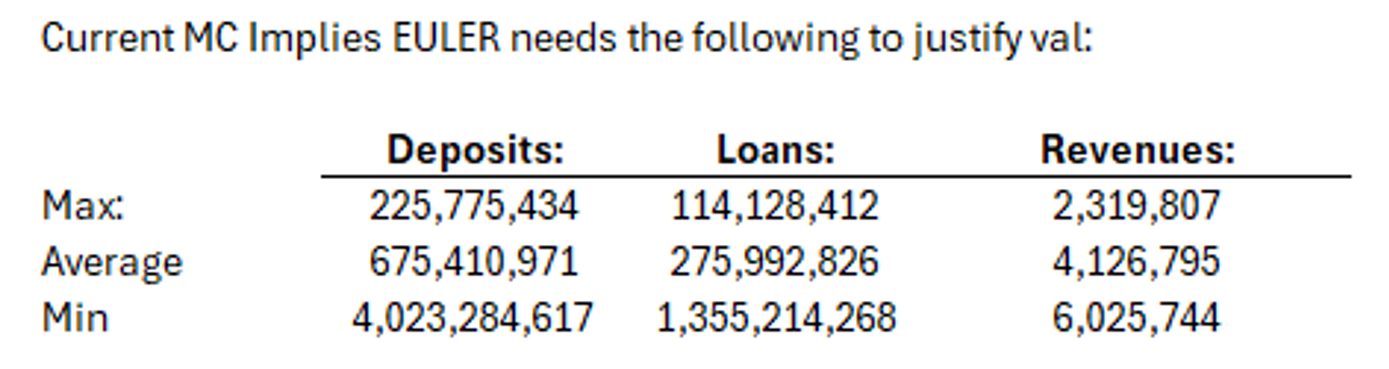

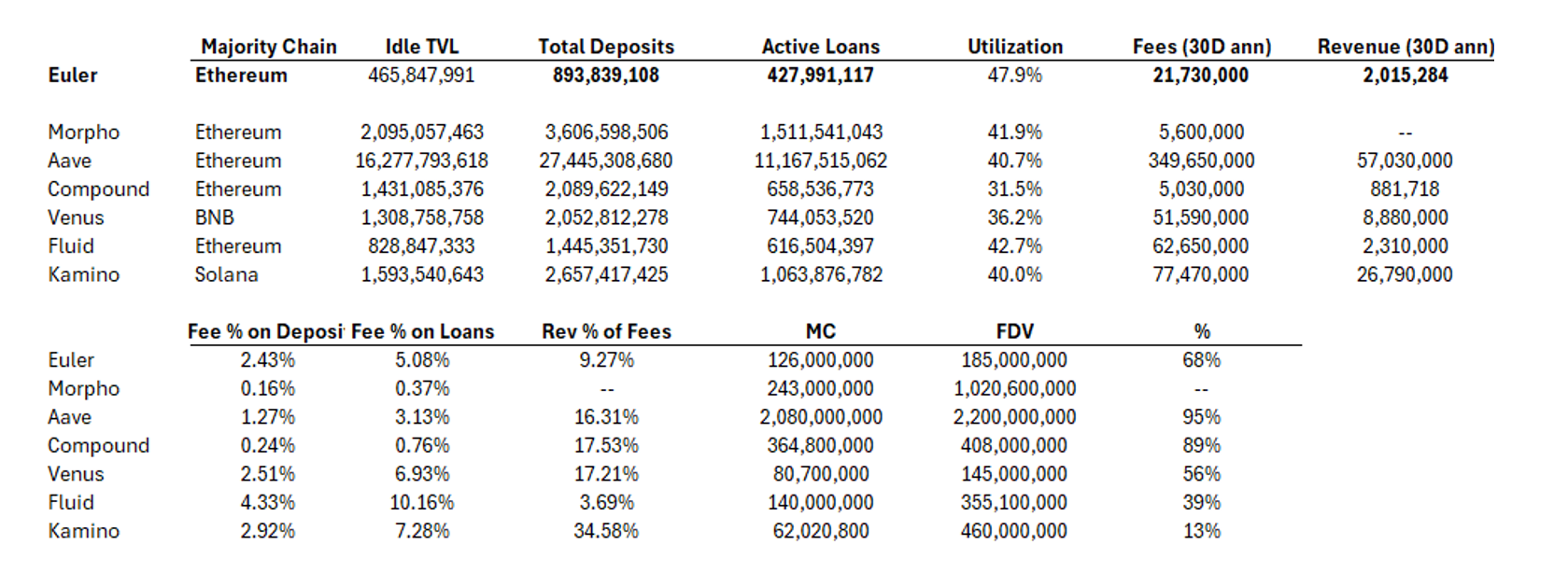

When we first underwrote Euler before v2 was even launched (July 2024), based on top competitors, these were the targets we laid out to justify the valuation at the time. We expected them to hit these within 6 months of launching but they have already blown through our baseline expectations for deposits and active loan origination. Revenue value capture (in terms of multiples) is still slightly lagging but still within the high-end of the range of how the market was pricing comps at the time. At their stage growth is key, not monetizing users, and we have full faith those levers will be pulled once appropriate scale has been reached – both on the core lending, and on value-add products such as Earn vaults and EulerSwap. Current annualized rev numbers come in at ~$2M; realized revs at $500K since December. Note this softness in revenue numbers comes at a time of severely depressed asset prices and onchain activity.

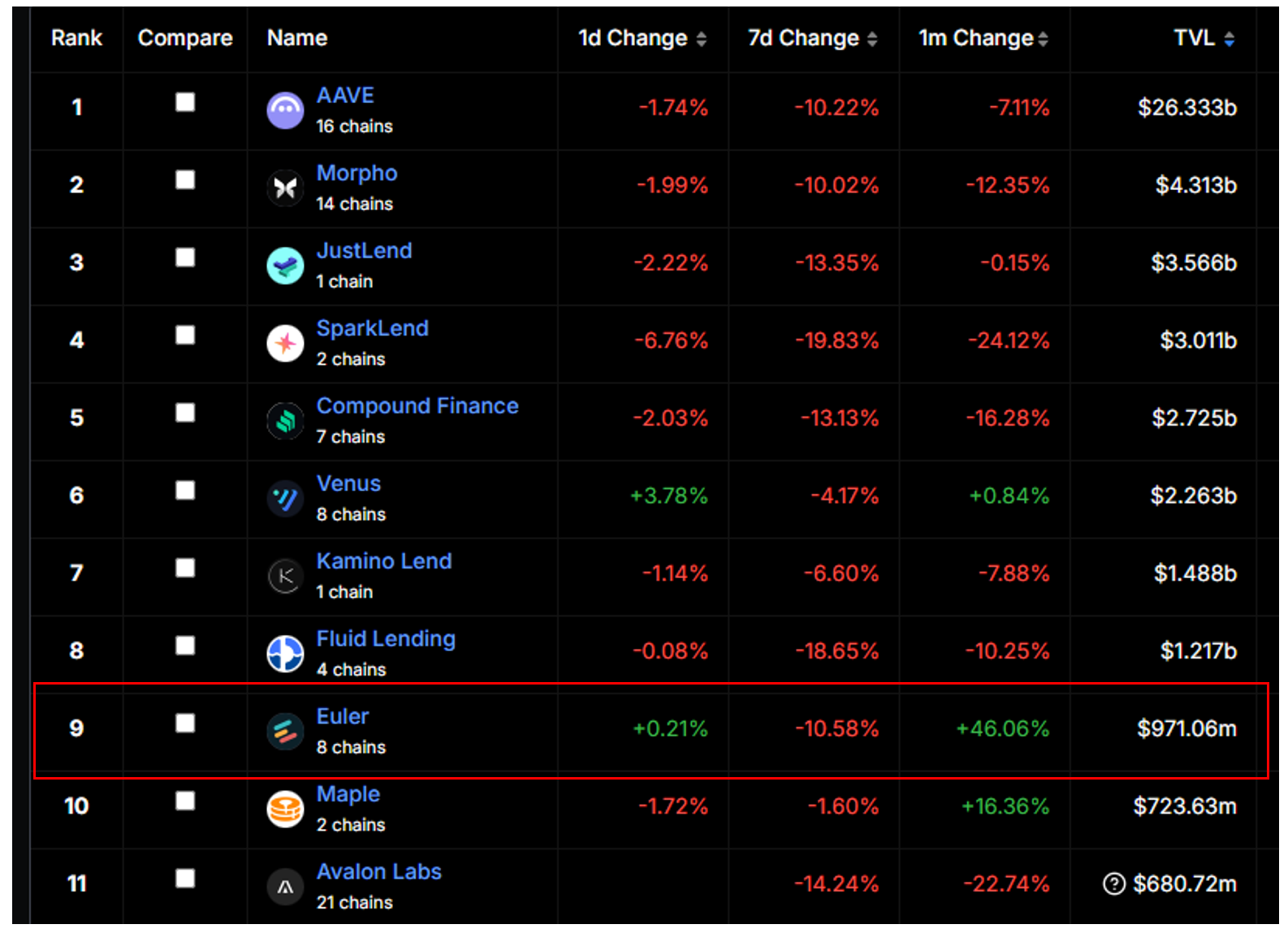

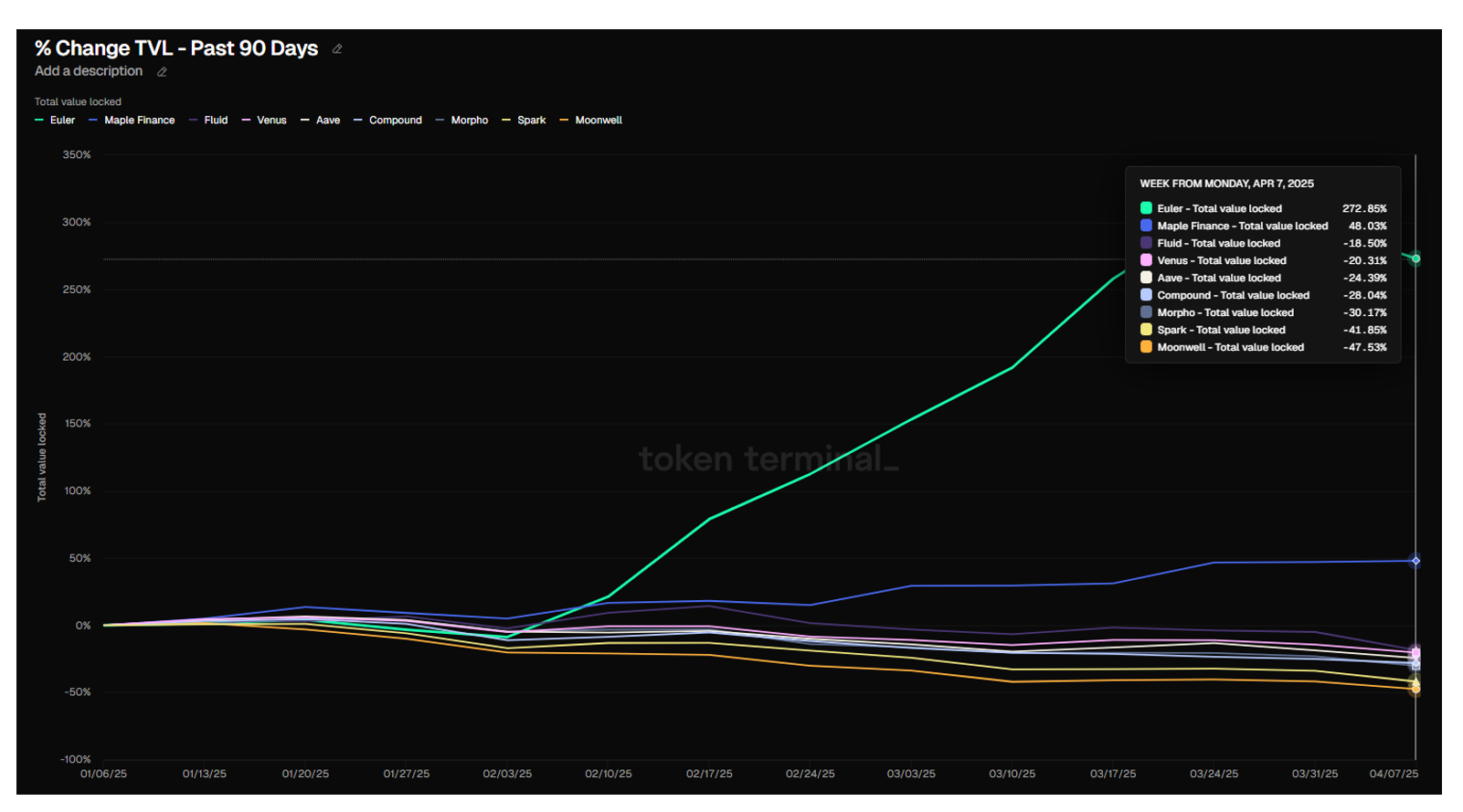

TVL growth in USD has been mind boggling – recently passing $1.2 billion. Normalized against ETH, it’s even stronger

Over the past month, they have grown TVL by 46% - where the rest of the market is down anywhere from 5-25%

Starting from near-0 in deposits (so mild discount required there), the TVL growth relative to the rest of the market is off the charts.

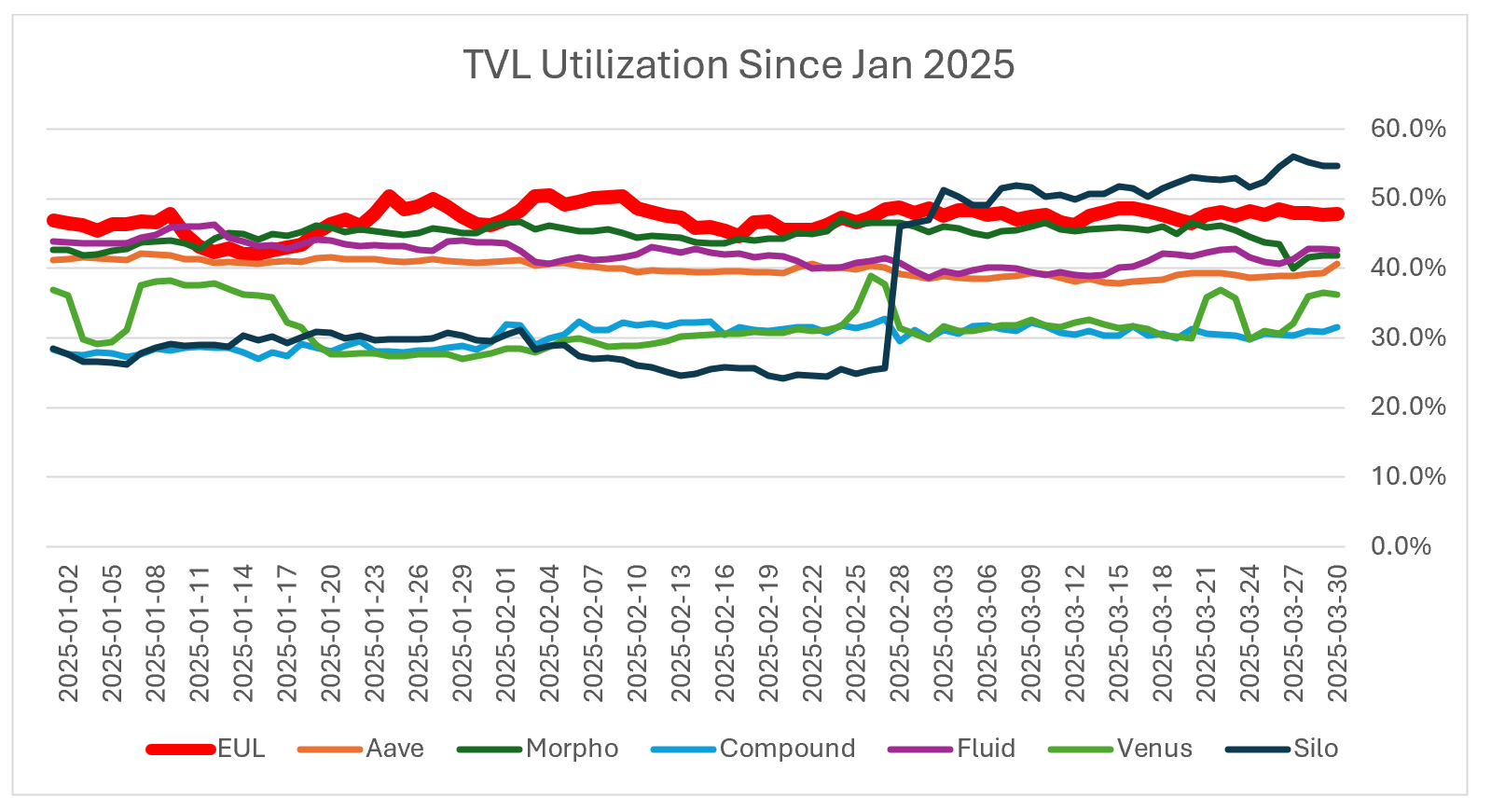

Utilization (Active Loans / TVL) is also the best among peer protocols. Note Silo utilization is currently highest in this set, but that is almost entirely incentive driven activity on Sonic right now – difficult to justify that as organic.

At just $185M FDV – Euler’s size and growth profile make it a highly attractive way to get quality exposure to onchain lending. The fee auction mechanism ensures there is a consistent market bid for the token.

Token Dynamics

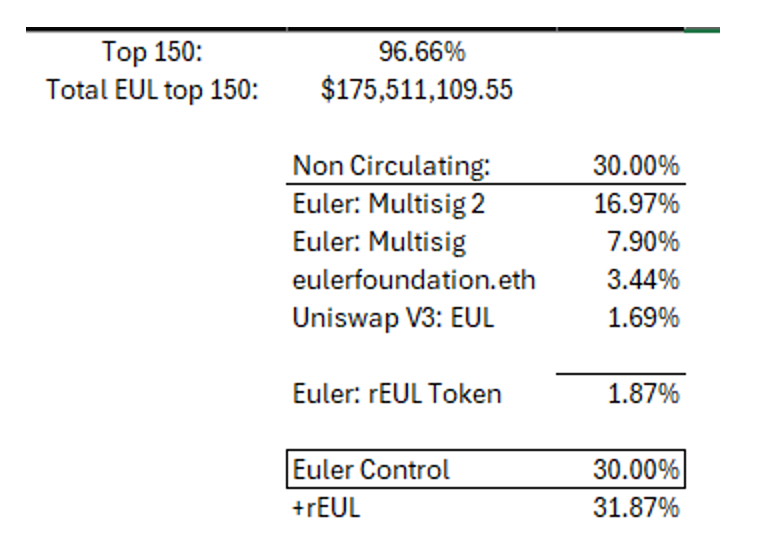

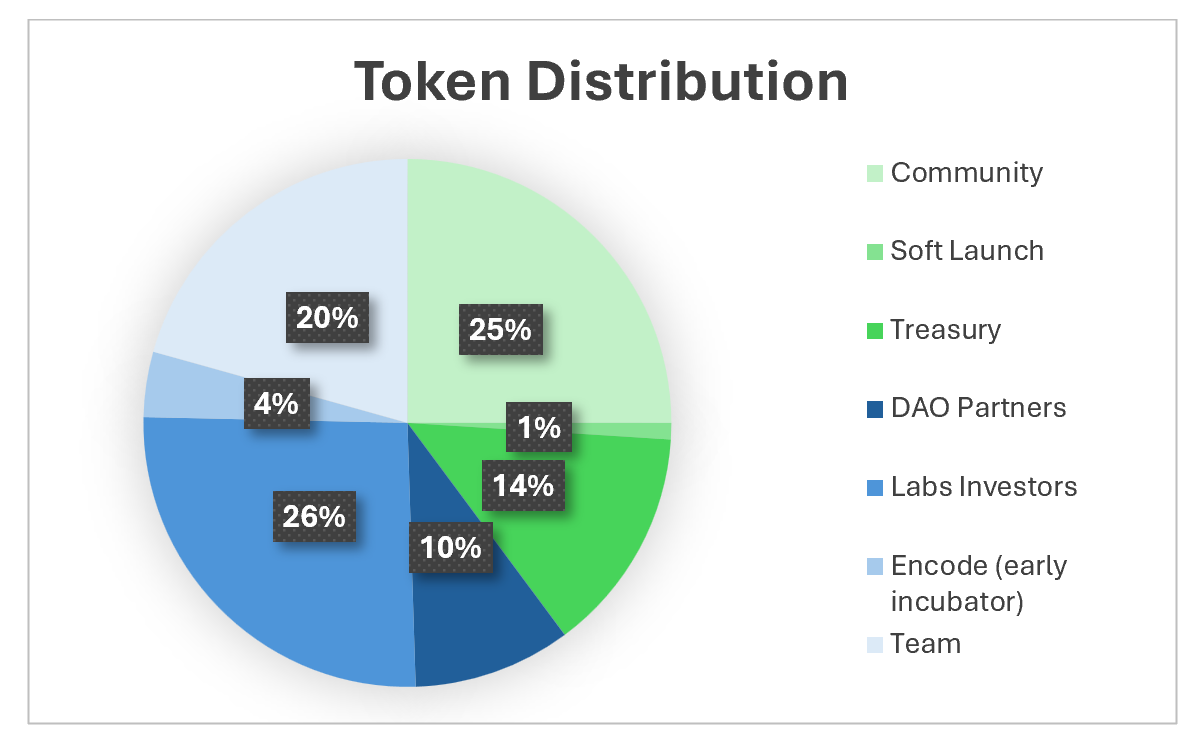

The total supply of EUL is 27,182,828 (in homage to Euler’s number). For the first 4 years, this supply is fixed. Token holders can vote to inflate the supply by a maximum of 2.718% per year. 70% of tokens are freely circulating. The non-circulating tokens are team controlled in the treasury, DAO, Foundation and liquidity.

The initial four-year breakdown of the EUL total supply is below. All investors/DAO partners are fully vested; co-founders will finish their 48-month linear vesting as of Jan 2026. 95% of tokens are fully unlocked.

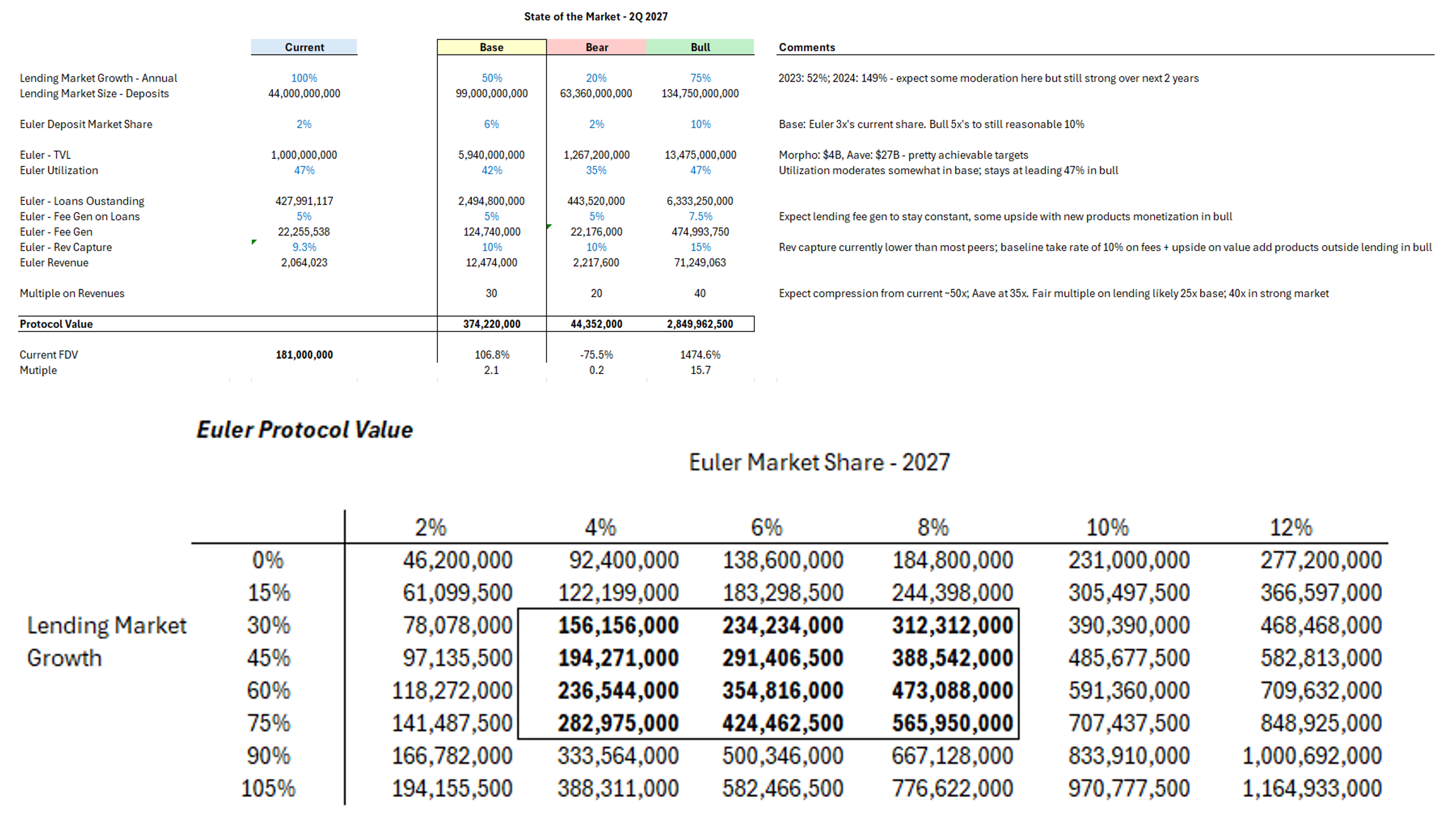

Valuation

Looking at only the lending aspect of Euler, it still presents an attractive opportunity at current levels and outlook. Note that this does not include any expansion in product lines such as EulerSwap and the marginal revenue they can generate there.

Risks

Reputation + previous hacks

- Euler v1 suffered one of the biggest exploits in DeFi in 2023 and the name has since been synonymous with that event. It remains on the top-15 list of largest crypto exploits in history.

- The team is strong, but with lending, trust and reputation is of paramount importance and this track record definitely presents a reputational headwind for them to overcome. Many still associate Euler with the exploit

Aave V4 will be modular

- Aave’s governance greenlit and funded (w/ $12M) Aave Labs to build out v4, with a focus on more modularity and a far more flexible framework

- While this is not yet live, looks like it will be a vault-based mechanism and include full cross-chain liquidity via Chainlink CCIP. Will allow for more flexible use of deposited assets in a controlled manner while maintaining strong risk management and isolation of funds. However, this is not the same as enabling rehypothecation per se, where collateral is re-used as security for additional borrowing without additional safeguards.

- Likely impacts Morpho more directly than Euler, but a competitive dynamic to keep in mind nonetheless

Morpho’s head start

- Beyond Aave’s new architecture, Morpho has gotten a headstart on the modular lending markets and has captured over $4B in TVL already. Its brand is strong and the parts of the market that aren’t served by Aave/Compound/Venus etc. are largely being served by Morpho already

- Morpho has a fresh token + airdrop campaigns at its disposal to compete against Euler

- Morpho has a pseudo-poison pill that transitions code to MIT from BUSL should they implement a fee switch and as such captures no revenue currently

- Euler’s growth to date has shown they can compete, especially given how quickly they deploy to new chains

Limited token dry powder

- Because Euler has been in the market for a few years, its token is largely issued. This hamstrings their incentive budget which serves as a headwind relative to other competitors

- Despite this, they have shown an incredible ability to grow TVL without direct inflationary incentive programs in place

Summary

Euler’s team is one of the best in the industry and has proven it can build a competitive product in the past (e.g. v1). V2 has already exceeded even the most optimistic projections going into 2025 and the team continues to grow their footprint through rapid deployment to the most active chains as they come to market. Before Euler, Morpho had captured much of the modular lending mindshare and presents a formidable direct competitor with a strongly entrenched position (largely concentrated on Ethereum and Base). However, Euler takes an even less opinionated and more permissionless approach to Morpho and as such is positioned to outcompete for long-tail markets while Aave continues to dominate the blue-chip pools. Though it has a relatively strong treasury ($30M), the fact that tokens are already widely distributed may be a headwind to attract the marginal depositor, all else equal.

•

•

•

Affiliate Disclosures

- The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- The author is not being compensated in any form by the target in relation to this research.

- To the best of the author’s knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

Neither BIDCLUB nor PHATPITCH LLC represents or endorses the accuracy or reliability of any advice, opinion, statement or other information displayed, uploaded, or distributed through BIDCLUB by any user, information provider, or other party. PHATPITCH LLC is not a broker, a dealer, or investment adviser. Nothing in BIDCLUB constitutes an offer or a solicitation to buy or sell any securities. BIDCLUB prohibits the sharing of material non-public information (MNPI), but assumes no responsibility for member conduct or associated risks. Nothing in BIDCLUB is intended as specific investment advice and no individual should make any investment decision based on any recommendation or analysis provided on BIDCLUB. You acknowledge that any reliance upon any such opinion, advice, statement, memorandum, or information shall be at your sole risk, and you bear sole responsibility for your own research and investment decisions. See full

Terms and Conditions.