Shuffle

SHFL

Target Name

Shuffle

Ticker

SHFL

Strategy

long

Position Type

token

Current Price (USD)

0.19

Circulating Market Cap ($M)

53.8

Fully Diluted Market Cap ($M)

182.8

CoinGecko

Purple Coin Gud: A Quality Defensive Asset Amidst a World of Uncertainty

01 May 2025, 10:16am

Thanks to Lai Yuen for providing access to data, reviewing this report and providing valuable feedback. All information presented is accurate to the best of my knowledge and this report was written purely for educational purposes. As always, DYOR and ape responsibly!

This report was written on my own volition for bidclub.io and I was not compensated in any way by the Shuffle team or any related parties for writing this report. I am not an employee, consultant or advisor to Shuffle and have never received any form of compensation from Shuffle. As a disclosure, I hold investments in $SHFL, $BTC, $HYPE, $AAVE and other assets not mentioned in this report. I do not hold short positions in any assets mentioned. All data presented in this report is as of April 25th 2025, unless noted otherwise.

As someone who loves sports betting and is an active liquid token investor, the Shuffle platform and $SHFL token have been on my radar for over a year. Candidly, I am not a seed investor, missed both the first airdrop and LBP. I began building a liquid position approximately 1 year ago and have added to the investment several times since. As of April 25th 2025, $SHFL trades within ~10% of my cost basis.

This investment report outlines my personal liquid token investment framework, reviews key features of Shuffle’s platform and the $SHFL token, highlights several unique insights around $SHFL’s fundamentals, covers some potential events that would motivate me to divest and raises some potential catalysts that would strengthen my bullish outlook.

My Liquid Token Investment Framework

Like many on CT, my first introduction to trading perps was on BitMEX. After getting liquidated many times and subsequently becoming the Co-Head of Ecosystem at WOO, it became apparent that I’m not a great trader. Over time I have evolved by refining my investment framework to focus on liquid tokens at the application layer that I perceive to be undervalued and am comfortable holding for several months to years. Here are the key features I look for in a potential liquid token investment:

Clear PMF in a Vertical I’m Bullish On: Category leaders with demonstrated traction in verticals that generate meaningful revenue. Think $BNB for CEXes, $HYPE for Perp DEXes, Tether equity for Stablecoins and $AAVE for Lending markets. In contrast, I am not as excited about verticals like oracle providers and the 50th L2 where its likely a race to zero and limited revenue is generated

Value Accrual Directly to Tokenholders: If it doesn’t make any revenue, it's an auto pass. If it makes revenue but the cashflows entirely accrue to dApp users or equity holders, then it's an easy pass (sorry $UNI). If the cashflows accrue to a DAO treasury, I’m likely not interested unless there is a clear path to returning cashflow to tokenholders (i.e. $SKY & $AAVE buybacks). In my view, the holy grail here are tokens that directly return some (ideally all) cashflows to tokenholders (i.e. $HYPE & $RAY)

Token Utility & Demand Sinks: Ideally there is a strong reason for users of a platform with PMF to hold the native token indefinitely. I think $BNB is the clear leader here with utility across trading fee discounts and launchpools. After working at WOO, I don’t think many realize how impressive it is that CZ has convinced many trading firms to hold mid 7 figs of $BNB for VIP9 fees

Hungry Founders & Teams with Integrity: If the team is checked out, get your check out. You know the teams who launched at 9-11 figs FDV and likely sold secondaries OTC or enabled staking of vesting tokens. As for integrity, this one speaks for itself and the perception alone of questionable integrity is enough for me to stay away (sorry Rollbit). Your goal should be to identify and back the hungry teams eager to make it(1). I believe you should also look for teams that are able to attract and retain strong talent and two great examples here are Ethena and Jito.

Valuation: I’m less concerned about MC or FDV in isolation and require full context on things like token inflation, cost basis of major stakeholders & OTC activity. Perhaps most importantly, I care about Cashflows Returned to Tokenholders, relative to MC or FDV depending on context. For example, I love Ethena as an innovative project and it checks most boxes but $ENA has had too much inflation subsidizing sUSDe yield and the insiders are up significant multiples compared to its liquid valuation

Perhaps most importantly, is How the Asset Fits in my Overall Portfolio. Is it correlated with my other holdings? Is it a small or large cap? Token or equity? Within the same vertical as another holding? Is there vesting or lockups? Does it contribute to my portfolio’s overall yield? Ideally each investment is a differentiated bet and, all things equal, preferably with lower correlation to existing holdings and fits well within the context of other assets.

I will not invest in a coin that is missing more than two of these features and the closer to checking all of the boxes translates to a larger allocation within my portfolio. After reading this report, I believe you will conclude that $SHFL checks all of these boxes and can uniquely fit into many liquid token portfolios as a quality, defensive holding.

Shuffle Platform & $SHFL Token

$SHFL is probably the only token on page 7 of Coingecko to have multiple reputable funds & investment professionals publish an investment thesis. The most comprehensive report was published by Rich Gavin, CEO of DACM, and I highly recommend you read it for a full background and financial analysis.(2) Animoca Ventures, the major gaming investment firm, published a similar report(3) last fall and so did 0xKyle(4), who recently joined the sharpest liquid investment firm in the space called Defiance. Safe to say, there is smart money holding $SHFL.

For those too lazy to read the reports, the TLDR is that Shuffle is one of the leading global GambleFi platforms, offering many casino games and a comprehensive menu of sports betting markets. The closest comp would be Stake or Rollbit and the onshore equivalents are the likes of Draftkings and FanDuel.

Many on CT often state they love owning the casino, such as holding $HYPE and depositing into HLP, and with $SHFL you literally can. As standard with all casino games and sports betting markets, Shuffle, or the House, has an inherent edge against its users. This enables Shuffle to earn consistent and predictable revenue over time as nearly all users inevitably lose after gambling for a sufficiently long period of time.

When it comes to PMF, if there is one thing people in crypto love to do, it's gamble. Just look at perps trading, trenching with shitters on pump.fun or shotgunning angel checks. When it comes to casino games, if you have any doubt then you haven’t been to the Marina Bay Sands during Token2049. As for sports betting, look no further than Crypto Fight Nights to see Shuffle’s PMF.

Source: https://x.com/barneytheboi/status/1781278405406945348

Unlike many grifty shitcoins, Shuffle has a track record of consistently and transparently returning cashflows to $SHFL tokenholders for over a year. The initial value accrual mechanism was a buyback and burn, which has resulted in over 5% of the total supply being permanently destroyed. This was achieved by burning 30% of Net Gaming Revenue (NGR) for all wagers denominated in $SHFL and 15% of NGR denominated in all other tokens (BTC, ETH, SOL, stablecoins etc.). Shuffle has been more than six months ahead of the flight to fundamentals trend we’ve seen since late last year and none of its peers on page 7 of Coingecko have any comparable value accrual.

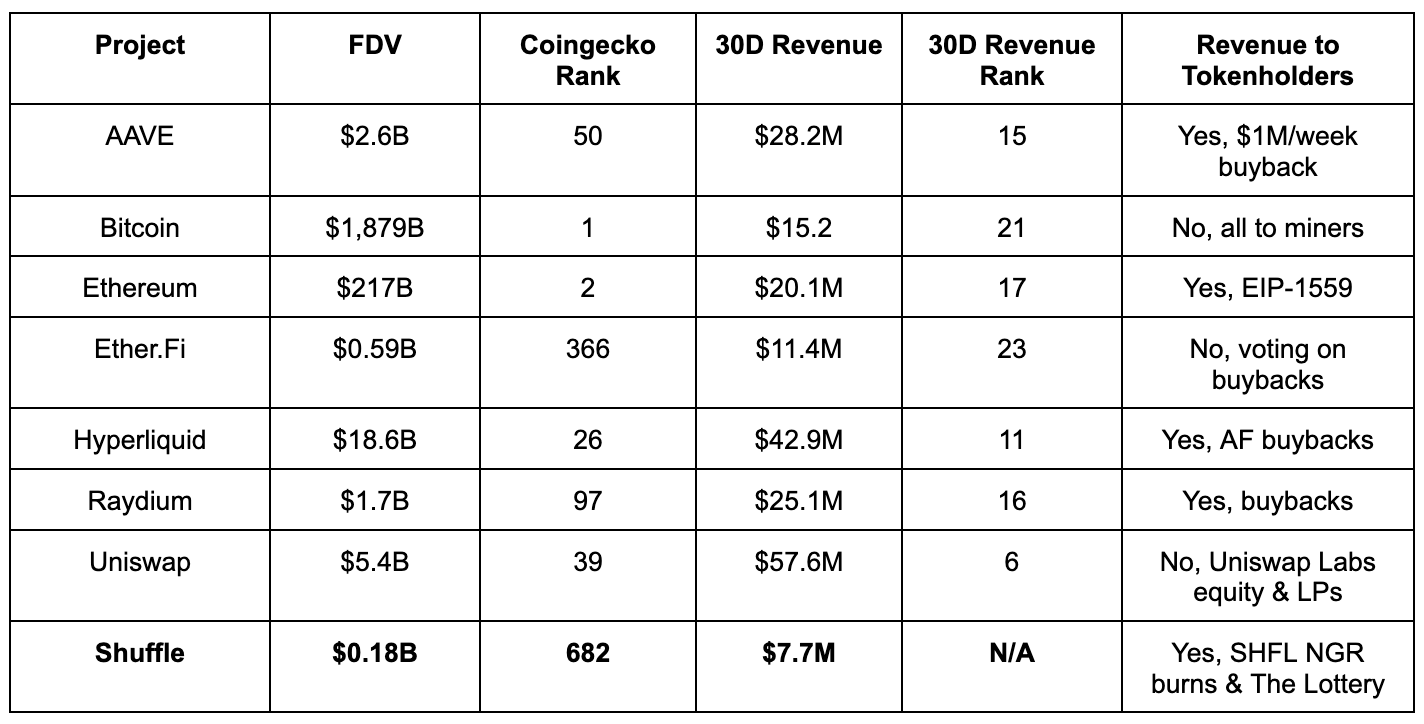

As of April 18th 2025 and on a four week rolling average, Shuffle had $14.7M in annualized cashflows returned to tokenholders. This equates to a multiple of 12.0 compared to $SHFL’s FDV and an impressive 3.6 multiple compared to current market capitalization. Using DeFiLlama’s revenue page and Coingecko, this table outlines several projects’ revenue & FDV:

Source: https://defillama.com/fees/simple, https://www.coingecko.com/ (Data as of April 29th, 2025)

As you can see, there is significant variation in the valuations versus revenue generated. For example, Bitcoin’s FDV is more than 10,000x larger than $SHFL’s and yet Shuffle’s platform revenue generated is roughly 50% of Bitcoin’s annualized transaction fees. Perhaps more nuanced is what happens with the revenue generated from the point of view of a tokenholder. Some projects pass most or all revenue along to their users, such as LP fees for Uniswap or transaction fees to Bitcoin miners.

Other projects have a dual equity and token structure where most of the revenue accrues to equity investors and the remainder goes to tokenholders. This has led many to criticize naive analysis of simply looking at protocol revenues, as what ultimately matters as a liquid token investor is cashflows returned to tokenholders.(5) In this regard, Shuffle stands out for having nearly $100M in annualized revenue and $15M in revenue returned to $SHFL tokenholders. At $50M market capitalization and $150M FDV, this amount of value accrual demonstrates $SHFL is objectively undervalued compared to many of its peers. The following diagrams help visualize how protocol revenue flows through to stakeholders:

Source: https://defillama.com/fees/simple, https://shfl.shuffle.com/shuffle-token-shfl/tokenomics/shfl-burn, https://shfl.shuffle.com/shuffle-token-shfl/tokenomics/lottery-history. Shuffle diagram’s data based on 4 week rolling average ending on April 25th, 2025 and Uniswap’s using 30 day historical data, both are annualized.

In corporate finance, there are two mechanisms to directly return cashflows back to equity shareholders: share repurchases and issuing dividend payments in dollars. Don’t tell the regulators but Shuffle’s buyback and burn program effectively emulates the former. In October 2024, Shuffle pivoted away from solely repurchasing tokens and began “paying a dividend” in the form of the Lottery. The Lottery is an engaging and fun way to have gamified, variable yield denominated in USDC earned on staked $SHFL.(6) There is nothing quite like checking the Lottery results every Friday morning EST, hoping for the chance to win $2M and at worst getting a 3-4 fig weekly stimmy while sipping morning coffee.

Source: Shout out to Lai Yuen for sharing the cleaned data and chart inspiration

The yield on staked $SHFL has varied between 30-70% annualized, paid entirely in USDC as opposed to industry standard of inflationary yield denominated in native tokens. This insanely thiccc dividend yield is a major component of what makes $SHFL a quality, defensive holding.

Looking beyond cashflows returned to tokenholders, $SHFL has two other characteristics that further increase its attractiveness within the context of a portfolio of liquid tokens. First, $SHFL has experienced significantly lower price volatility YTD than most other coins. Measuring YTD price volatility as the standard deviation of daily price returns, we observe the following data: $BTC 0.028, $SOL 0.057, $AAVE 0.059, $HYPE 0.066, $ENA 0.077 and $SHFL 0.048. This means that $SHFL has exhibited considerably less volatility than coins like $SOL that are more than 580x its FDV.

Perhaps more impressive is the lack of correlation to other liquid tokens that $SHFL has exhibited. The table below is a correlation matrix of daily price returns YTD and the colour scale has green representing low correlation and red indicating high correlation. Looking at $BTC and $SOL, there is over 80% correlation so a drawdown in $BTC is highly likely to be accompanied by one in $SOL. Conversely, $SHFL has exhibited effectively no correlation with any of the assets listed, as well as most liquid tokens more generally. Since the formula for Sharpe ratio (i.e. risk-adjusted returns) penalizes both high price volatility and high correlation with other portfolio holdings, these findings further reinforce that $SHFL is a quality, defensive asset that most liquid token portfolios would benefit from including.

Source: https://www.coingecko.com/ (Data as of April 28th, 2025)

Why Would I Dump my Purple Coins?

Reading up to this point, you may think I believe $SHFL can solve world hunger and cure Brian Armstrong’s baldness. So to provide a balanced perspective, here are some current issues with Shuffle’s platform and the $SHFL token that I’d like to see improved, as well as some future events that if materialized would likely cause me to divest.

The simplest criticism to make of Shuffle is that material decline in that wagering volume denominated in $SHFL. You can observe this trend in the chart below since Airdrop 2 and it's reflected in how low the $SHFL NGR is compared to non-$SHFL NGR in the revenue Sankey diagram above. It is also reflected in the low amounts of deposits and withdrawals for $SHFL into Shuffle’s EVM custody address.(7) The platform has clear PMF as a casino and sportsbook but there is also clear data showing that very few users prefer gambling in $SHFL relative to BTC, ETH, SOL, stablecoins and altcoins. In the next section, I share some ideas on how to improve $SHFL wagering volume, which translates to higher $SHFL NGR and most importantly burned $SHFL tokens each week.

Source: https://shuffle.com/token

Perhaps a more substantive issue, at least at first glance, is that the $SHFL team and early investors have begun vesting. One may speculate that the underperformance of $SHFL is linked to insiders selling their vesting tokens. Looking at the team vesting smart contract,(8) you can trace every distribution of $SHFL to a deposit on Shuffle. A skeptic would argue the recipients are depositing to sell off-chain discreetly or withdraw to a fresh address to break up ownership before selling. However, the Shuffle platform has a one-way conversion mechanism, which means users can only convert non-$SHFL assets into $SHFL but insiders depositing vested $SHFL cannot sell into other coins on Shuffle. Regarding withdrawing to fresh addresses, there have only been 3 withdrawals from Shuffle for more than 100K $SHFL since the last tranche of vested tokens were distributed on April 16th, 2025.(9) These tokens could even be withdrawals from normal users but taking the most conservative assumption that all withdrawals are from the team, that implies less than 15% of vested tokens have been sold.

Alternatively, the team could have gambled their vested tokens on Shuffle and that is a great outcome since it translates to users making -EV wagers against the House and contributing to $SHFL NGR. The last and clearly most likely outcome is that the team is staking their vested $SHFL into the Lottery. This is a great way for the team to receive USDC income on their tokens while not selling and the Lottery data supports this hypothesis. On the weeks that the team doesn’t receive vesting tokens, the Lottery grows by considerably smaller amounts than during weeks where vested tokens were distributed.(10)

So if the team is willing to stake their vested $SHFL into the Lottery instead of dumping, that is a strong signal to me that the team is bullish on $SHFL and so vesting should not be viewed as a negative event.(11) The remaining fair criticism is that the insiders staking their vested tokens will dilute the juicy staking yields but that is a solvable problem through growing the platform and its NGR. $SHFL’s vesting situation looks even better when you compare it to other tokens that have insiders hedge by shorting perps, dumping on unlocks or perhaps most egregious, staking vesting tokens - don’t take my word for it, ask liquid $TIA investors.(12)

Looking ahead, there are two main catalysts that could happen which would cause me to dump my purple coins. First would be an alternative GambleFi platform emerging that takes away substantial market share from Shuffle and has a liquid token that checks the boxes of my investment framework. Several analytics platforms proxy market share through verifiable metrics like onchain deposits across all networks and for the time being, Shuffle remains well positioned in the top 3 and ahead of Rollbit.(13) More substantially, if the value accrual mechanisms of the burn and the Lottery were removed then I would immediately consider divesting. I view this outcome as highly unlikely but wanted to flag it as these mechanisms are core to my thesis of $SHFL as a quality, defensive holding suitable for any liquid token portfolio.

What Would Make Me Ape More?

After spending the past week diving deeper into Shuffle, I’m already more bullish than when I began writing this investment report. That said, I’ve identified four initiatives that would cause me to consider sizing up my investment into $SHFL further. I’ve ordered them in my perceived level of increasing difficulty to implement and magnitude of impact.

The lowest hanging fruit is clearly getting $SHFL listed on more CEXes. It effectively has no CEX listings so unless investors proactively buy onchain, via the Shuffle platform or OTC from Wintermute, it's very difficult to obtain coins. $SHFL has a surprisingly large amount of onchain liquidity relative to its FDV, which makes sense given Shuffle takes wagers in $SHFL and needs price stability. However for $SHFL to reach mid 9 figures or 10 figures of FDV, it needs to open up more channels for buyers.

The crooked listing teams at these top CEXes are so hypocritical in my opinion as they list tons of shitcoins, outright scams and coins corresponding to platforms clearly doing unregulated activity. Shuffle’s platform requires KYC and it holds a gambling license in a reputable jurisdiction. In contrast, a token like $dYdX is universally listed while operating without KYC and clearly does not hold a license for offering perp trading to retail traders globally. There are even examples of other GambleFi coins listed on CEXes, such as FUNtoken on Binance with significantly less traction that $SHFL.(14) Perhaps a strong interim step is to circumvent CEX listings and buy a spot ticker on Hyperliquid, to capitalize on a flourishing ecosystem that is dying for quality spot assets.(15)

Given the low price volatility of $SHFL, deep onchain liquidity and embedded yield via the Lottery, I would love to see a liquid staking token (LST) be issued for $SHFL staked in the Lottery. There would be tons of new DeFi use cases enabled, such as depositing into lending markets and borrowing stablecoins against $SHFL_LST or looping yields, where the embedded yield may offset borrowing costs. You could deposit $SHFL_LST into Pendle and speculate on the growth of the yield in the Lottery via buying YTs or hedge the yield volatility by holding PTs. I could easily see more savvy DeFi users adding $SHFL_LST to their portfolios, which would help drastically improve onchain holder count, currently sitting at a measly 3,986 and likely contributing to no CEX listings. This could even benefit the Lottery yield for those choosing not to mint the LST, as there could be some forgone yield as a cost for minting the LST, which is reinvested back into the Lottery or distributing to other stakers.

Shuffle has a proven track record of going after VIPs - trust me I went to their private Axwell concert at Token2049 last year. One issue that constantly pains whale sportsbettors is being able to wager with large limits at reasonable betting lines (i.e. prices or odds). I would love to see Shuffle implement a VIP sports betting offering entirely denominated in $SHFL. This would require users to stake substantial amounts of $SHFL into the lottery to access these enhanced limits and prices. All wagering would be denominated in $SHFL to help improve the wagering volume in $SHFL and $SHFL NGR. I believe this is a much more effective way to spend $SHFL compared to the previous Airdrop campaigns in terms of achieving sustainable platform growth for the sportsbook.

The single most bullish catalyst for $SHFL would be an increased revenue share in the Lottery and token burns. Currently ~15% of total platform revenue is returned to tokenholders and this share increasing to 30% or higher would have a substantial impact on the fundamental outlook of $SHFL. After having worked at a CEX for years, I understand that costs are substantial but there are clear economies of scale so as Shuffle grows, it should be more feasible to spread its fixed costs and increase the revenue share to tokenholders. The total onchain gambling market is likely to continue growing and Shuffle’s market share is closer to 10% than 25%, so I believe this outcome has potential but I have no inside knowledge nor confidence it could happen in the immediate future. This is why my investment horizon is measured in months to years, as teams require time to achieve these home run outcomes.

Final Thoughts

Liquid token investing is really fucking hard. The professionals take massive drawdowns just like us retail investors. Correlations of assets are quite high and during periods of intense market stress, they head towards 1. Some teams abuse material non-public information and engage in other unethical activities. Other teams remain above board but their competitors chose not to. Sometimes the better teams and platforms don’t win despite having a stronger team, better UX or distribution partners.

But if you’ve read this far, you clearly love the game like I do. You have no choice but to deploy capital - someone must walk the point and take early stage venture risk. Despite being liquid, most liquid projects are Seed to Series B stage whereas companies IPO in TradFi after several more investment rounds and are significantly more mature businesses.

With all of these risks and pitfalls in mind, I believe $SHFL has many redeeming qualities. It has a relatively low valuation, its price correlation is extremely low compared to other tokens, it has multiple forms of value accrual with substantial amounts of revenue returned directly to tokenholders, it has strong PMF within an attractive vertical and it has several meaningful catalysts ahead. You’re unlikely to get a 5x in 2 weeks like possible via going lev longing $FARTCOIN or gambling on pump.fun shitters but you’re also unlikely to take a 75% drawdown. So given all of these characteristics, I am confident that $SHFL is a quality, defensive holding that compliments many liquid token portfolios.

Footnotes

(1) Read Jez’s article if you haven’t already: https://oldcoinbad.com/p/a-starter-guide-to-the-crypto-mmo

(2) https://x.com/richwgalvin/status/1844677870482055361

(3) https://x.com/jennyqcheng/status/1852006926172983738

(4) https://x.com/0xkyle__/status/1844454804128661669

(5) https://x.com/pythianism/status/1915427518838169759

(6) Read these docs for full details on the Lottery: https://shfl.shuffle.com/shuffle-token-shfl/tokenomics/shfl-lottery

(7) 0xDFaa75323fB721e5f29D43859390f62Cc4B600b8

(8) https://etherscan.io/address/0xcd543881d298bb4dd626b273200ed61867fb395d#tokentxns

(9) The potential weak-handed list for April 16th’s vesting distribution: 0xe7ed028b7bbf4f1a47756011975a869864c90a2812fc130834577fe0283379c1, 0x6f07122821bc0e0bf558aab97d70fc944a07541f5805566c1f793676adb6c276 and 0xc3d236bdca6fffb738ce3e6e0be140517a0cbdecf102cacc5d59380e4b0c82a0.

(10) The March 14th lottery had 103.5M $SHFL staked and then a vesting distribution happened and the subsequent March 21st lottery had 110.4M $SHFL staked. Then the following three lotteries (March 28th, April 4th and April 11th) had 112.8M, 114.7M and 117.5M $SHFL staked, respectively. Then after the April 16th unlock, the amount of staked $SHFL grew by nearly 7M $SHFL to 124.3M.

(11) If you don’t believe me that the team is bullish SHFL, hear it from the horse’s mouth: https://x.com/ishanhaq/status/1909003216991465634

(12) https://x.com/gtx360ti/status/1841786995741491299

(13) https://tanzanite.xyz/analytics

•

•

•

Affiliate Disclosures

- The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- The author is not being compensated in any form by the target in relation to this research.

- To the best of the author’s knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

Neither BIDCLUB nor PHATPITCH LLC represents or endorses the accuracy or reliability of any advice, opinion, statement or other information displayed, uploaded, or distributed through BIDCLUB by any user, information provider, or other party. PHATPITCH LLC is not a broker, a dealer, or investment adviser. Nothing in BIDCLUB constitutes an offer or a solicitation to buy or sell any securities. BIDCLUB prohibits the sharing of material non-public information (MNPI), but assumes no responsibility for member conduct or associated risks. Nothing in BIDCLUB is intended as specific investment advice and no individual should make any investment decision based on any recommendation or analysis provided on BIDCLUB. You acknowledge that any reliance upon any such opinion, advice, statement, memorandum, or information shall be at your sole risk, and you bear sole responsibility for your own research and investment decisions. See full

Terms and Conditions.

I'm a little concerned tbh about the shrinking volume on the platform. What's mgmt's comments on why it's declining and how'd it pump?

Also I don't think this will ever get listed on CEX's. What do u think can drive a rerating aside from liquidity + more volume?